Alexander Trentin Interviews Miles Kimball about Macroeconomic Stabilization: Negative Rates and Sovereign Wealth Funds

I am grateful for permission to reproduce the text of this interview here on my blog. I have been pleased with all of Alexander Trentin's interviews of me. The previous interviews are here:

Negative Interest Rates and Financial Stability: Alexander Trentin Interviews Miles Kimball

Alexander Trentin: Negative Interest Rates and the Swan Song of Cash

The International Trade System Should Be Designed to Foster More Balanced Trade

Alexander Trentin Interviews Miles Kimball on Next Generation Monetary Policy

Also, let me highlight this piece by Alexander:

What follows is Alexander’s newest interview of me:

Miles Kimball, economics professor at University of Colorado Boulder, argues for negative rates and sovereign wealth funds to stabilize the economy.

Miles Kimball: “Sovereign wealth funds could stabilize financial markets and would earn money by profiting from high risk premia.”

Professor Kimball, the Fed kept interest rates last week unchanged. What is your take on the current policy of central banks?

Central banks worry about the current environment. The tightening cycle seems to be coming to an end. It is about a balance of risks. From a political perspective, it might be easier now for the Fed and other central banks to keep rates unchanged or lowering them rather than increasing them. If a central bank raises rates in the current environment, people will blame it if the economy does badly. By contrast, it seems less risky to be lenient: if inflation heats up, inflation will just be moving in the direction of the inflation target. At this moment, politics and good policy are aligned. One positive factor is that long-term yields are much lower.

How is that positive?

During and after the financial crisis the expectations of interest rates were too high, the expectations turned out to be wrong as interest rates stayed low. Now the situation has changed: long-term yields and expectations for future interest rates are low. The reason is that markets know the playbook of central banks: how they would deal with an economic downturn with all the new policy tools. The last time the markets didn’t know that. This is positive for the economy, because long-term rates matter as well as short-term rates for the economy. And long-term rates depend on expectations of future central bank policy. However, given where it is now, the Eurozone could be in trouble if the ECB feels it can’t lower rates any further.

Do you mean you think the ECB should set negative rates further below zero?

Yes. Things are not going that well in the Eurozone. In comparison, Japan appears to have a much stronger recovery. The ECB should think of its next move, especially how to set lower rates. There is one easy thing they could implement that would open the way to set rates considerably lower.

What do you propose?

The immediate concern about negative rates is not yet that people would store paper currency, but a concern about bank profits and a concern that there would be bad headlines if savers faced negative interest rates on their accounts. Central banks should subsidize the provision of zero interest rates in checking and savings accounts, up to a limit. Then checking and savings accounts with balances under that limit would not be affected by negative policy rates. You could tell people: We are implementing negative rates in a way that shields regular people from negative rates in their checking and savings accounts.

But wouldn’t that dilute the effect of a negative interest rate policy?

It is totally misguided to think that negative rates on small checking and savings accounts are a crucial part of the transmission mechanism. A few thousand dollars per person could be exempted without any serious harm to the transmission mechanism. Those with large amounts in checking and savings accounts would still be subject to negative rates, and it is the interest rate on the last dollar or euro or franc in large accounts that matters for transmission.

How do you answer concerns that negative rates are a burden for bank profits?

Central banks do worry about the effect on bank profits when negative interest rates reduce net interest margins. But the main way in which negative rates reduce net interest margins is that banks are reluctant to reduce rates on checking and savings accounts below zero. If the central bank subsidizes zero rates for small checking and savings accounts, it deals with this in two ways: first, with the subsidy, bank profits do not suffer from providing zero rates to small accounts, and second, the limit on the quantity of checking and savings that can get the subsidy makes it easier for banks to explain why they need to have negative rates on large accounts beyond that level.

Are there other ways to help banks in a negative rate environment?

Even if a central bank doesn’t want to subsidize zero rates for small accounts, there are many ways in which central banks can effectively throw money at commercial banks to help their balance sheets. The question is more whether it is politically viable to throw money to commercial banks—and the answer is yes if it is done in the right way. In the Eurozone, the LTRO programs offers banks cheap liquidity to do more lending. And in Switzerland, you have tiered reserves, which excludes some bank reserves from negative rates. Nevertheless of concerns about net interest margins, which the subsidy for zero rates on small accounts takes care of, negative rates are helpful to bank balance sheets. First, banks profit from capital gains when interest rates decreases. Second, banks benefit from a more robust economy as fewer people and businesses default.

The Fed stopped its interest rate hikes not only due to macroeconomic news but also due to financial market turmoil. Should financial markets influence monetary policy?

I am not sympathetic to the idea that central banks should observe the stock market closely. There is too much noise trading. The conditions in the stock markets are not very important for the capital costs of companies; stock prices affect financing costs directly only when a firm does an IPO. What is more important is the risk premium observable in the market for commercial paper or junk bonds. There is research suggesting it would be better monetary policy if rates were routinely cut almost one-for-one if the spread between commercial paper rates and Treasury bill rates, or the spread between junk bond rates and Treasury bill rates increases beyond what can be justified by increased default risk. Though this policy can be justified without any reference to financial stability, it also helps improve financial stability.

What if a central bank is not ready to implement deep negative rates?

One solution would be to finance a sovereign wealth fund by issuing Treasury bills. This is much safer than borrowing to spend money with the idea of using fiscal policy to stimulate the economy. I think it is much better to add debt to buy assets than to add debt to increase government spending. Sovereign wealth funds could stabilize financial markets and would earn money by profiting from high risk premia. Organizationally, they should be independent of Central Banks as they require a different kind of expertise.

When advocating intervention in financial markets, you seem to mistrust markets.

I defer to the market microeconomically, but not macroeconomically. If the government wants to intervene in a microeconomic way, there should be a high burden of proof. However, markets by themselves do a bad job stabilizing the economy at a macroeconomic level. There are chronically high risk premia, fluctuations are too large, and sticky prices lead to regular business cycles. I also don’t agree with free bankers who say that a private market should be responsible for monetary policy. Governments have a large risk-bearing capacity, that political entrepreneurs will try to use in one way or another—typically by government guarantees that are off budget but often cost taxpayers dearly when something goes wrong and the government has to pay up on the guarantee. This applies also to the need for the government to do bailouts if the economy would otherwise fall apart. With a sovereign wealth fund, taxpayers would not only bear the risks but would also gain the profits from this risk-bearing capacity. And done right, a sovereign wealth fund would add to financial stability and so make it less likely that the government would need to do a bailout. However, higher capital requirements, beyond those currently mandated, are the real key to greater financial stability.

What do you think of Modern Monetary Theory, which advocates using debt-financed fiscal policy to have full employment?

I think in an extreme interpretation MMT is technically not correct. In a not so extreme interpretation, it is equivalent to standard economic theory—which means it would have none of the new implications MMT folks are claiming. But even if MMT is not correct, it might be politically helpful and I welcome a diverse field of opinions. Here is how it might be helpful: government spending is currently not responsive enough to the level of interest rates – if interest rates are low, spending—especially government spending on genuine investments that will raise government revenue later on—should be higher. However, I don’t think fiscal policy should do the job of monetary policy to stabilize the economy. Whenever I hear a central bank president saying they need more help from fiscal policy, I want to say: “Don’t wait for fiscal policy—do your job!” If their tools are not sufficient, they should innovate to add new tools to their toolkit.

Other posts on negative interest rate policy are organized in this bibliographic post:

Other posts related to sovereign wealth funds:

How a US Sovereign Wealth Fund Can Alleviate a Scarcity of Safe Assets

How to Stabilize the Financial System and Make Money for US Taxpayers

Four More Years! The US Economy Needs a Third Term of Ben Bernanke

After Crunching Reinhart and Rogoff’s Data, We Found No Evidence High Debt Slows Growth

Roger Farmer and Miles Kimball on the Value of Sovereign Wealth Funds for Economic Stabilization

Answering Adam Ozimek’s Skepticism about a US Sovereign Wealth Fund

Tristan Hanson and Eric Lonergan: What Would a UK Sovereign Wealth Fund Look Like?

In addition, I have three storified Twitter discussions about sovereign wealth funds:

some posts on closely related issues (two of which are guest posts):

and many posts (of which I will only list three right now) on a key scientific issue relevant for sovereign wealth funds–the level of efficacy of quantitative easing:

Trillions and Trillions: Getting Used to Balance Sheet Monetary Policy

Wallace Neutrality Roundup: QE May Work in Practice, But Can It Work in Theory?

Freakonomics: The Story of Bananas

The story of bananas told by Freakonomics podcast #375: “The Most Interest Fruit in the World,” is fascinating. According to the podcast, one reason that bananas are as inexpensive as they are is that almost all the bananas we see are clones: the Cavendish variety. As a result, techniques for dealing with those bananas can be standardized.

Unfortunately, the fungus that knocked the Gros Michel or “Big Mike” clones from their top banana spot is coming for the Cavendish clones. It looks like the fungus can be defeated by adding or editing genes to match key genes of another variety of bananas that doesn’t have all the desirable properties of the Cavendish variety, but can defeat the fungus. That may save the day. But many people are leery of adding or editing genes. The most likely outcome is that in the future, the typical grocery store will have more varieties of bananas: a tweak on the Cavendish for those who are OK with genetic modification or editing and other varieties for those who aren’t.

I love bananas. Unfortunately, they are a somewhat high on the insulin index: 59 or so. (See “Forget Calorie Counting; It's the Insulin Index, Stupid.” In the belief that green bananas have a lower insulin index than that, I buy the greenest bananas I can find in the grocery store, and then put them in the refrigerator as soon as I get home. This isn’t what most people do: after shipping, bananas are put into ripening rooms for 4-7 days, because most people want yellow bananas.

A common treat for me is to cut up a green banana and poor over it half a can of coconut milk from Costco (actually coconut cream—not the watery stuff):

I sprinkle on some Ceylon cinnamon from Whole Foods:

I also often add a bit of Swerve.

In addition to bananas, I often get Plantains. I often don’t know how ripe a plantain will be. Even if it looks somewhat green, a Plantain is often ripe enough that I can eat it exactly as I would a banana. If it is less ripe than that, I slice it up, fry it in avocado oil and eat it with goat butter. The experience is somewhere in between that of eating a baked potato and eating the french fries—both of which I now carefully avoid.

Don’t miss my other posts on diet and health:

I. The Basics

Jason Fung's Single Best Weight Loss Tip: Don't Eat All the Time

What Steven Gundry's Book 'The Plant Paradox' Adds to the Principles of a Low-Insulin-Index Diet

II. Sugar as a Slow Poison

Best Health Guide: 10 Surprising Changes When You Quit Sugar

Heidi Turner, Michael Schwartz and Kristen Domonell on How Bad Sugar Is

Michael Lowe and Heidi Mitchell: Is Getting ‘Hangry’ Actually a Thing?

III. Anti-Cancer Eating

How Fasting Can Starve Cancer Cells, While Leaving Normal Cells Unharmed

Meat Is Amazingly Nutritious—But Is It Amazingly Nutritious for Cancer Cells, Too?

IV. Eating Tips

Using the Glycemic Index as a Supplement to the Insulin Index

Putting the Perspective from Jason Fung's "The Obesity Code" into Practice

Which Nonsugar Sweeteners are OK? An Insulin-Index Perspective

V. Calories In/Calories Out

VI. Other Health Issues

VII. Wonkish

Framingham State Food Study: Lowcarb Diets Make Us Burn More Calories

Anthony Komaroff: The Microbiome and Risk for Obesity and Diabetes

Don't Tar Fasting by those of Normal or High Weight with the Brush of Anorexia

Carola Binder: The Obesity Code and Economists as General Practitioners

After Gastric Bypass Surgery, Insulin Goes Down Before Weight Loss has Time to Happen

A Low-Glycemic-Index Vegan Diet as a Moderately-Low-Insulin-Index Diet

Analogies Between Economic Models and the Biology of Obesity

Layne Norton Discusses the Stephan Guyenet vs. Gary Taubes Debate (a Debate on Joe Rogan’s Podcast)

VIII. Debates about Particular Foods and about Exercise

Jason Fung: Dietary Fat is Innocent of the Charges Leveled Against It

Faye Flam: The Taboo on Dietary Fat is Grounded More in Puritanism than Science

Confirmation Bias in the Interpretation of New Evidence on Salt

Eggs May Be a Type of Food You Should Eat Sparingly, But Don't Blame Cholesterol Yet

Julia Belluz and Javier Zarracina: Why You'll Be Disappointed If You Are Exercising to Lose Weight, Explained with 60+ Studies (my retitling of the article this links to)

IX. Gary Taubes

X. Twitter Discussions

Putting the Perspective from Jason Fung's "The Obesity Code" into Practice

'Forget Calorie Counting. It's the Insulin Index, Stupid' in a Few Tweets

Debating 'Forget Calorie Counting; It's the Insulin Index, Stupid'

Analogies Between Economic Models and the Biology of Obesity

XI. On My Interest in Diet and Health

See the last section of "Five Books That Have Changed My Life" and the podcast "Miles Kimball Explains to Tracy Alloway and Joe Weisenthal Why Losing Weight Is Like Defeating Inflation." If you want to know how I got interested in diet and health and fighting obesity and a little more about my own experience with weight gain and weight loss, see “Diana Kimball: Listening Creates Possibilities” and my post "A Barycentric Autobiography.

John Locke: Usurpation is a Kind of Domestic Conquest, with this Difference, that an Usurper Can Never Have Right on His Side

Chapter XVII of John Locke’s 2d Treatise on Government: Of Civil Government, “Of Usurpation,” has a very simply point, expressed in the title above. By simple usurpation, John Locke means taking a role in a government one is not entitled to, without otherwise changing the form of the government. Increasing the power of that role beyond what that role is entitled to would be tyranny added to usurpation:

§. 197. AS conquest may be called a foreign usurpation, so usurpation is a kind of domestic conquest, with this difference, that an usurper can never have right on his side, it being no usurpation, but where one is got into the possession of what another has a right to. This, so far as it is usurpation, is a change only of persons, but not of the forms and rules of the government: for if the usurper extend his power beyond what of right belonged to the lawful princes, or governors of the commonwealth, it is tyranny added to usurpation.

Even simple usurpation is a serious violation of the principle of consent. Indeed, John Locke repeatedly compares a violation of the method a state has for choosing its leaders as being akin to anarchy:

§. 198. In all lawful governments, the designation of the persons, who are to bear rule, is as natural and necessary a part as the form of the government itself, and is that which had its establishment originally from the people; the anarchy being much alike, to have no form of government at all; or to agree, that it shall be monarchical, but to appoint no way to design the person that shall have the power, and be the monarch. Hence all commonwealths, with the form of government established, have rules also of appointing those who are to have any share in the public authority, and settled methods of conveying the right to them: for the anarchy is much alike, to have no form of government at all: or to agree that it shall be monarchical, but to appoint no way to know or design the person that shall have the power, and be the monarch. Whoever gets into the exercise of any part of the power, by other ways than what the laws of the community have prescribed, hath no right to be obeyed, though the form of the commonwealth be still preserved; since he is not the person the laws have appointed, and consequently not the person the people have consented to. Nor can such an usurper, or any deriving from him, ever have a title, till the people are both at liberty to consent, and have actually consented to allow, and confirm in him the power he hath till then usurped.

I find John Locke’s comparison of usurpation to anarchy puzzling. Even in the Roman Empire, where usurpation occurred with stunning frequency, the situation was much better than anarchy. And if usurpation occurred only occasionally, the improvement over anarchy might be quite substantial, assuming those usurpations were not combined with tyranny. (It is possible that the word anarchy did not have quite the same connotations in John Locke’s day as it does now.)

For links to other John Locke posts, see these John Locke aggregator posts:

Neil Lewis Jr.: Has Gender Stereotype Threat Declined? →

The title is a link to an interesting Twitter thread about stereotype threat.

Deeper Negative Rates Can Ward Off Secular Stagnation

I have often avoided the term “secular stagnation” on this blog because its meaning is ambiguous. Is “secular stagnation” just another term for a liquidity trap, does it mean forces that lower the steady state real interest rate, or does it mean a slowdown in productivity growth?

Negative interest rate policy that paper currency policies that can reduce the rate of return on paper currency below zero are the straightforward solution to a liquidity trap: the liquidity trap is simply gone once one changes paper currency policy, and interest rate policy by the central bank can then proceed without constraint. (On how to change the rate of return on paper currency, or otherwise allow room for deep negative rates despite the existence of paper currency, see my bibliographic post “How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide.” I also have another paper coauthored with Ruchir Agarwal on the way.)

Long-run real interest rates and long-run productivity growth are beyond the power of monetary policy to change directly. (See my exposition of this standard view in “What Monetary Policy Can and Can't Do.”) But enabling deep negative rates allows monetary policy to do its job of stabilizing the economy, removing a large distraction that takes many economists and policymakers away from discussing ways to raise long-run productivity growth. Raising long-run productivity growth would also tend to raise the long-run real interest rate.

While arguing the opposite, Martin Wolf makes the case for adding deep negative interest rates to the monetary policy toolkit in his Financial Times op-ed “Monetary policy has run its course” in his summary of a paper by Lukasz Rachel and Lawrence Summers:

A recent paper by Lukasz Rachel and Lawrence Summers shines light on these questions. Its thrust is to support and elaborate the hypothesis of “secular stagnation”, revived by Prof Summers as relevant to our era in 2015. This paper’s principal innovation is to treat the big advanced economies as a single bloc. Here are four conclusions.

First, a dramatic and progressive decline in real interest rates on safe assets has occurred, from over 4 per cent in the 1980s to around zero now. Furthermore, shifts in risk preferences do not explain this decline, since spreads in yields of riskier over safe assets have changed little. (See charts.)

Second, this secular fall in real interest rates implies a roughly equivalent fall in the (unobservable) “neutral” or “equilibrium” rate — the rate at which demand matches potential supply.

Third, governments are not generating this structural weakness in demand. On the contrary, by expanding social spending, deficits and debt, governments have raised equilibrium long-term real interest rates, other things being equal.

Finally, changes in the private sector would, on their own, have generated a fall of more than seven percentage points in the equilibrium real rate of interest. Among the many factors driving this sharp decline must have been ageing; declining productivity growth; rising inequality; declining competition; and falling prices of investment goods.

A key point here is that fiscal policy has already been working hard. Trying to keep aggregate demand up without using lower interest rates requires quite extreme fiscal policy.

Martin Wolf dismisses negative interest rate policy in one paragraph:

Suppose, then, that our economies were to fall into a deep recession, yet still have near zero real interest rates and very low nominal rates, too. Suppose, too, that, inflation were somewhere between zero and two per cent. Then the response to a recession would require strongly negative short-term nominal interest rates, possibly as low as minus 5 per cent. That would, to put it mildly, create a wasps’ nest of technical, financial and political problems.

There are two answers to Martin: First, there has been progress in thinking through how to address the technical, financial and political problems that Martin is not fully aware of. Second, any solution to secular stagnation involves a wasp’s nest of technical, financial and political problems. There are no easy outs. In particular, fiscal policy is not the easy out that people think. As I point out in “Monetary vs. Fiscal Policy: Expansionary Monetary Policy Does Not Raise the Budget Deficit,” fiscal policy not only adds to the national debt, but is almost unavoidably tangled up in political struggles.

By contrast, in many countries governments have given central banks broad enough authority that negative interest rate policy beyond what has been done so far can be executed by an independent central bank without additional legislation. Politicians can then distance themselves from the negative interest rate policy. A central bank that does so will, of course, get some blowback, but central bankers pride themselves on being willing to raise interest rates when appropriate even when such a move meets with criticism. They should take a similar pride in being willing to lower interest rates deeper below zero when appropriate even when that move meets with criticism.

Also, there is a set of arguments that work equally well against both fiscal policy and quantitative easing as alternatives to negative interest rate policy. A large enough dosage of either fiscal policy or quantitative easing is likely to have important side effects. Fear of these side effects is likely to keep the dosage of fiscal policy and quantitative easing below the dosage that would be necessary to get quick recovery during a serious recession in which interest rates were not cut very much. And waiting to see if a dosage of quantitative easing within historical experience or a dosage of fiscal policy within the most likely range can deliver enough stimulus is likely to lead to a delay in recovery costing trillions of dollars worth of social welfare relative to going to deep negative interest rates immediately.

Another way of putting the argument that delay is very costly, in relation to quantitative easing, is that the “buying time” that Mohamed El-Erian talks about in “How Western Economies Can Avoid the Japan Trap” is a bad thing, not a good thing:

Large-scale balance sheet operations like quantitative easing (QE) can buy time by seeking to inject more liquidity directly into the system. But they don’t address the underlying issues, and they come with their own set of costs, forms of collateral damage, and unintended consequences.

The sentence right before this passage is just plain wrong:

Monetary policy, after all, is less effective near the “zero bound” and in scenarios where other “liquidity trap” factors are in play.

On the contrary, to a good approximation, if all interest rates are lowered, including the paper currency interest rate (as is easily possible) monetary policy is just as effective per basis point in the negative region, and there is no limit to how far interest rates can be cut other than the danger of overstimulating the economy.

Altering paper currency policy also alleviates other worries Mohamed El-Erian has. He writes:

… persistently low – and in some cases negative – interest rates tend to eat away at the institutional integrity and operational effectiveness of the financial system, thereby reducing bank lending and limiting the range of long-term products that insurance/retirement firms can offer to households. Another indirect effect stems from expectations about the future. The longer growth and inflation remain low, the more tempted households and companies will be to postpone consumption and investment decisions, thus prolonging low growth and inflation.

With paper currency interest rates going down along with other interest rates, there is no reason for the spreads that financial firms live off to be dramatically different. As one salient example, relying on negative interest rate policy instead of quantitative easing allows for a more historically typical yield curve. As another example, for large accounts that go beyond the quantity for which the central bank provides a subsidy for along the lines I discuss in “How to Handle Worries about the Effect of Negative Interest Rates on Bank Profits with Two-Tiered Interest-on-Reserves Policies,” deposit rates can go down enough that the interest rate margin between interest rates on loans banks make and the deposit rates they pay can be substantial.

As for people postponing investment and consumption, low enough interest rates can counteract any such tendency: a negative interest creates a penalty for postponing investment or consumption.

In my view, the future will be on a safer track if the prominent economists and journalists who are now advocating preparations for dramatic fiscal expansion began advocating more vigorous innovation in in negative interest rate policy—either instead of, or in addition to a dramatic fiscal expansion. A great deal may rest on whether they do so.

Kevin D. Hall and Juen Guo: Why it is So Hard to Lose Weight and So Hard to Keep it Off

As an economist, I love Kevin Hall’s and Juen Guo’s approach to energy balance and weight loss. In their paper “Obesity Energetics: Body Weight Regulation and the Effects of Diet Composition,” they emphasize right away that calories in and calories out are endogenous:

Weight changes are accompanied by imbalances between calorie intake and expenditure. This fact is often misinterpreted to suggest that obesity is caused by gluttony and sloth and can be treated by simply advising people to eat less and move more. …

Obesity is often described as a disorder of energy balance arising from consuming calories in excess to the energy expended to maintain life and perform physical work. While this energy balance concept is a useful framework for investigating obesity, it does not provide a causal explanation for why some people have obesity or what to do about it.

In particular, obesity prevention is often erroneously portrayed as a simple matter of bookkeeping whereby calorie intake must be balanced by calorie expenditure.1 Under this “calories in, calories out” model, treating obesity amounts to advising people to simply eat less and move more, thereby tipping the scales of calorie balance and resulting in steady weight loss that accumulates according to the widely known, but erroneous, 3500 kcal per pound rule.2,3 Therefore, failure to experience substantial weight loss implies that an individual lacks the willpower to adhere to a modest lifestyle intervention over a sufficient period of time.

Then they detail evidence on different mechanisms by which calories in and calories out might depend on weight so that while improving one’s dietary habits can change the level of one’s weight, there is a new equilibrium at a lower weight that can only be maintained by continuing those better dietary habits: permanent weight loss requires permanent changes in behavior.

How Calories Out Depend on Weight. There are three components of calories out. First is inefficiency in converting all the calories in food into generally usable energy for the body. This is called the thermic effect of food because heat is the form in which energy that is not generally usable shows up. (Obviously, there are situations in which body heat is itself useful.) In addition to the thermic effect of food, there is resting energy expenditure and physical activity energy expenditure. Physical activity expenditure can, in turn, be divided into exercise calories and spontaneous physical activity calories.

The Thermic Effect of Food. One of the big points Kevin and Juen make is that a highfat lowcarb diet does not increase the thermic effect: in their meta-analysis, there is a tiny difference in the opposite direction. In other words, the evidence I discussed in “Framingham State Food Study: Lowcarb Diets Make Us Burn More Calories” is outweighed by the evidence in other studies.

One confounding factor is that the thermic effect of protein is greater than the thermic effect of either fat or carbs. However, this doesn’t mean you should ramp up your protein consumption. Protein—particularly animal protein—has other issues for health:

(Also, there are reasons to worry about soy.)

The thermic effect of food is not that large: Kevin and Juen write “For typical diet compositions, the thermic effect of food is approximated to be about 10% of energy intake.” As a percentage of energy intake, this dimension of calories out is likely to go down when one eats less. Some other metabolic components of energy expenditure might get counted as part of resting energy expenditure. These metabolic components should follow a similar pattern to the thermic effect of food.

One of the things I am confused about is where the energy burned by gut bacteria that doesn’t make it to the human host figures into this typology of calories out. Also, on the other side, what about certain types of gut bacteria taking calories that were indigestible by humans (and so usually not included in the usual calorie counts) and turn them into humanly usable calories?

Resting Energy Expenditure. Other thing equal, the more you weigh, the higher the resting energy expenditure. So when you get to a lower weight, this dimension of calories out is likely to go down.

Physical Activity Energy Expenditure. It takes a lot of energy to move a heavy body. Conversely, the lighter you are, the fewer calories any given amount of activity uses. Kevin and Juen write: “physical activity energy expenditure declines with weight loss unless its quantity or intensity increases to compensate.”

Exercise. While exercise increases energy expenditure during exercise, it may lead to less energy expenditure the rest of the day. Here is how Kevin and Juen put it:

While often considered a first-line treatment option for obesity, large amounts of exercise are required to result in a modest degree of average weight loss.15 However, exercise results in preferential loss of body fat and maintenance of fat-free mass compared with diet-induced weight loss.16,17 but exercise does not appear to prevent the slowing of metabolic rate during weight loss.18 Exercise interventions typically result in less average weight loss than expected, based on the exercise calories expended, and individual weight changes are highly variable even when exercise is supervised to ensure adherence.19 A likely explanation for these observations is that the energy expended during exercise is variably compensated by changes in food intake and non-exercise physical activity behaviors.19

The recently proposed “constrained energy expenditure model” provides an alternative explanation for why exercise interventions often result in minimal weight loss.20 According to this model, daily energy expenditure is regulated and increments in physical activity expenditure are predicted to be offset by decreases in non-physical activity expenditure (ie, the thermic effect of food or REE) resulting in minimal energy imbalance. The experimental basis of the constrained energy expenditure model in humans includes cross-sectional data demonstrating that free-living daily energy expenditure adjusted for body composition is relatively constant for a wide range of physical activity levels measured using accelerometry.21,22 Furthermore, longitudinal data have found that progressive increases in the quantity and intensity of aerobic exercise training do not lead to corresponding increases in total daily energy expenditure in ad libitum-fed men and women.23

Effects of Calories In on Calories Out. Even apart from weighing less, the less you eat, the fewer calories you burn. The body could conserve energy by either reducing resting energy expenditure or reducing physical activity energy expenditure (perhaps mostly spontaneous physical activity, which is harder to notice than exercise). Kevin and Juen write: “Reductions in energy intake lead to decreased energy expenditure to a degree that is often greater than expected based on changes in body composition or the thermic effect of food.25,26”

Effects of Weight Loss on Appetite. A lower weight can result in a higher appetite that can easily lead to more food intake. The article below, “How strongly does appetite counter weight loss? Quantification of the feedback control of human energy intake” by David Poldori, Arjun Sanghvi, Randy Seeley and Kevin R. Hall showed this in an ingenious way. A drug that was being tested in a placebo-controlled clinical trial lead to quite a bit of blood sugar being excreted in the urine. So those who got the real drug had a reduction in calories in net of that excretion of blood sugar. Those who lost blood sugar lost more weight than those on the placebo, and ate more the more weight they lost. One caveat is that the amount of food intake was imputed from a model rather than directly measured.

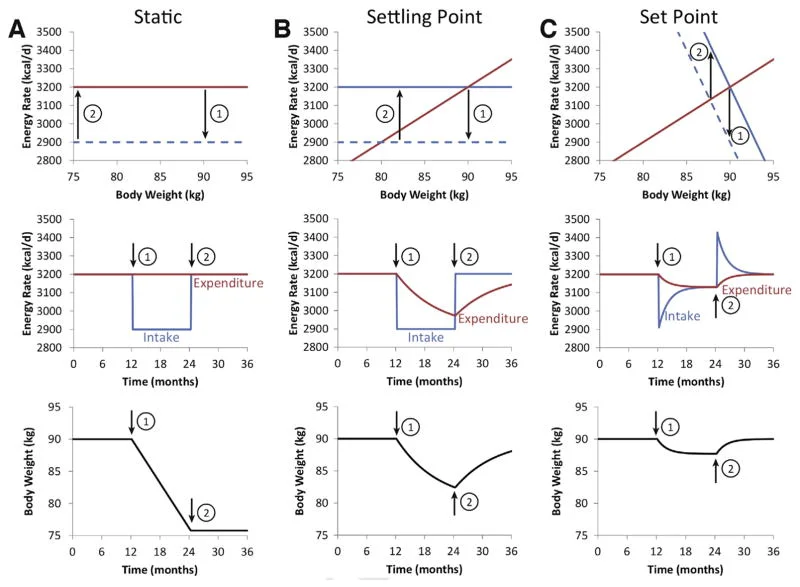

The Determination of Equilibrium Weight. All of these effects go in the same direction in terms of the qualitative behavior of body weight. They mean that a particular set of overall eating habits (aside from things governed by appetite in ways people don’t realize) and exercise habits corresponds to an equilibrium weight. Changing one’s eating and exercise habits changes that equilibrium weight. But if one goes back to the old habits, the original equilibrium weight will again apply. (In an economic analogy, weight is like the capital stock in a Solow growth model, not like the capital stock in the AK model.) In the graphs below, taken from Kevin and Juen’s paper, economists will find the top row the most familiar way to think about equilibrium. The column on the left shows what would happen if lower weight had no effect on either calories in or calories out. The middle column shows what happens if calories out go down as weight goes down. The column on the right shows what happens if calories out go down as weight goes down and calories in go up as weight goes down. In both the middle and right columns, there is an equilibrium weight for any set of eating and exercise habits. Going back to the old habits leads back to the old weight. Maintaining a new lower weight requires permanently different habits.

Hope for Dramatic, Permanent Weight Loss. One intervention that Kevin and Juen do not talk about in their paper is a change in the timing of eating as an intervention, whether that means a short eating window within each day or some use of longer fasts (periods of time without eating but still drinking water). What they do is provide ample reason why interventions short of changing the time pattern of one’s eating have such a tough time delivering permanent weight loss. Here is their conclusion:

In addition to the long-term feedback control of energy intake mediated by homeostatic signals related to body weight and composition, eating behavior is also strongly influenced by social and environmental influences in conjunction with learned eating habits.73,74 While previous conceptions of the set point model were thought to be incompatible with non-homeostatic influences on food intake and body weight,72 such effects can be naturally incorporated by altering the position or slope of the energy intake line depicted in Figure 3A and the defended body weight will be adjusted accordingly.

Unfortunately, we do not yet know the quantitative effects of non-homeostatic influences on the set point model, but there is likely to be a wide degree of individual variation. Some people may experience substantial changes in the energy intake, along with correspondingly large weight changes, whereas others will be more resistant. Re-engineering the social and food environments may facilitate shifts in the energy intake line, but losing weight and keeping it off using willpower alone to reduce energy intake is difficult because considerable effort is required to persistently resist the physiological adaptations that act to increase appetite and suppress energy expenditure.

I want to focus attention on the hypothesis that one of the most important aspects of the “social and food environment” is our customs about the timing of eating: the idea that it is normal to have three meals a day, every day, with snacking being OK. Question that social norm, and there is hope for dramatic, permanent weight loss.

Don’t miss my other posts on diet and health:

I. The Basics

Jason Fung's Single Best Weight Loss Tip: Don't Eat All the Time

What Steven Gundry's Book 'The Plant Paradox' Adds to the Principles of a Low-Insulin-Index Diet

II. Sugar as a Slow Poison

Best Health Guide: 10 Surprising Changes When You Quit Sugar

Heidi Turner, Michael Schwartz and Kristen Domonell on How Bad Sugar Is

Michael Lowe and Heidi Mitchell: Is Getting ‘Hangry’ Actually a Thing?

III. Anti-Cancer Eating

How Fasting Can Starve Cancer Cells, While Leaving Normal Cells Unharmed

Meat Is Amazingly Nutritious—But Is It Amazingly Nutritious for Cancer Cells, Too?

IV. Eating Tips

Using the Glycemic Index as a Supplement to the Insulin Index

Putting the Perspective from Jason Fung's "The Obesity Code" into Practice

Which Nonsugar Sweeteners are OK? An Insulin-Index Perspective

V. Calories In/Calories Out

VI. Other Health Issues

VII. Wonkish

Framingham State Food Study: Lowcarb Diets Make Us Burn More Calories

Anthony Komaroff: The Microbiome and Risk for Obesity and Diabetes

Don't Tar Fasting by those of Normal or High Weight with the Brush of Anorexia

Carola Binder: The Obesity Code and Economists as General Practitioners

After Gastric Bypass Surgery, Insulin Goes Down Before Weight Loss has Time to Happen

A Low-Glycemic-Index Vegan Diet as a Moderately-Low-Insulin-Index Diet

Analogies Between Economic Models and the Biology of Obesity

Layne Norton Discusses the Stephan Guyenet vs. Gary Taubes Debate (a Debate on Joe Rogan’s Podcast)

VIII. Debates about Particular Foods and about Exercise

Jason Fung: Dietary Fat is Innocent of the Charges Leveled Against It

Faye Flam: The Taboo on Dietary Fat is Grounded More in Puritanism than Science

Confirmation Bias in the Interpretation of New Evidence on Salt

Eggs May Be a Type of Food You Should Eat Sparingly, But Don't Blame Cholesterol Yet

Julia Belluz and Javier Zarracina: Why You'll Be Disappointed If You Are Exercising to Lose Weight, Explained with 60+ Studies (my retitling of the article this links to)

IX. Gary Taubes

X. Twitter Discussions

Putting the Perspective from Jason Fung's "The Obesity Code" into Practice

'Forget Calorie Counting. It's the Insulin Index, Stupid' in a Few Tweets

Debating 'Forget Calorie Counting; It's the Insulin Index, Stupid'

Analogies Between Economic Models and the Biology of Obesity

XI. On My Interest in Diet and Health

See the last section of "Five Books That Have Changed My Life" and the podcast "Miles Kimball Explains to Tracy Alloway and Joe Weisenthal Why Losing Weight Is Like Defeating Inflation." If you want to know how I got interested in diet and health and fighting obesity and a little more about my own experience with weight gain and weight loss, see “Diana Kimball: Listening Creates Possibilities” and my post "A Barycentric Autobiography.

A Liberal Turn in the Mormon Church

The dictum “Everything is relative” can sometimes steer people wrong, but seeing things in relative terms is one important perspective. Using “liberal” and “conservative” to mean socially liberal and socially conservative in the usual political sense, the Mormon Church remains quite socially conservative, but it has recently taken a liberal turn.

One of the most important recent changes is one that is not easily visible to non-Mormons and has probably been in the works for some time: a change in the language of the Mormon temple ceremonies to be more nearly gender-neutral.

Highly gender-asymmetric language had been a stone in the shoe of many Mormon women for a long time. Things are now improved. in order to appreciate the magnitude of this change, I highly recommend reading Peggy Fletcher Stack and David Noyce’s Salt Lake Tribune article “LDS Church changes temple ceremony; faithful feminists will see revisions and additions as a ‘leap forward’”:

Another recent change is a continuing widening of the racial and ethnic diversity of Mormon Church leaders. Ideologically, Mormonism is universalistic, so this is an easy evolution, but it is one that could have positive effects over time. (Gender balance is another matter entirely. See “Will Women Ever Get the Mormon Priesthood?” There are a few women in relatively high leadership positions in the Mormon Church, but beyond being few in number, in all practical terms there is no question that every one of them ranks behind at least 15 male Mormon leaders—the 3 men in the First Presidency and the 12 men in the Quorum of the 12 Apostles—in power and influence.)

But perhaps the most remarkable recent change in the Mormon Church has been the downgrading of gay marriage what I described in a November, 2015 post as “The Mormon Church Decides to Treat Gay Marriage as Rebellion on a Par with Polygamy” to gay marriage being officially on a par with heterosexual premarital sex (which is a serious sin in Mormonism). From the article flagged below:

Previously, our Handbook characterized same-gender marriage by a member as apostasy. While we still consider such a marriage to be a serious transgression, it will not be treated as apostasy for purposes of Church discipline," leaders wrote. "Instead, the immoral conduct in heterosexual or homosexual relationships will be treated in the same way."

Many of the headlines emphasize the repeal of a particular unjust part of the policy that existed for three and a half years: when gay marriage was treated as rebellion on a par with polygamy, the children of a gay marriage were treated as inherently suspect. That is now gone.

But there are many other consequences of downgrading gay marriage from high rebellion to a serious sin. In particular, it gives local Church leaders a lot of leeway (if they choose) to make married gay couples feel more welcome in a Mormon congregation.

One of the reasons this is a remarkable change is that it repeals a policy that is not even 4 years old. My brother Chris emphasizes this in his guest post “The No-Longer Policy: Where Do We Go From Here?” on By Common Consent shown below:

… the Policy’s reversal has challenged our collective ideas of “revelation” alongside the near infallibility halo our culture casts over our religious leaders.

Chris elaborates on this view in the comments section, referencing my post “Flexible Dogmatism: The Mormon Position on Infallibility”:

With respect to revelation and correctness, I am bemused by arguments that speak of “flexible dogmatism” (a coinage I attribute to my brother and he attributes to a friend). Flexible dogmatism is the idea that the Church can renounce past policies and practices, even past doctrines and theologies, but it cannot renounce the rightness of past policies at the time they were in effect. Flexible dogmatism is a common practice in rationalizing the Church. I think it is sorely tested (I believe to the point of breaking) by 180-degree turns in just a few years.

How did the Mormon Church end up with a policy it wanted to back away from after just a few years? My post “The Mormon Church Decides to Treat Gay Marriage as Rebellion on a Par with Polygamy” gives one perspective. Here is Chris’s description of the dynamic in “The No-Longer Policy: Where Do We Go From Here?”:

The Exclusion Policy seemed like a response to the landmark U.S. Supreme Court decision in Obergefell v. Hodges (decided June 26, 2015) which guaranteed the fundamental right to marry to same-sex couples. The Obergefell decision could have been predicted 10 years earlier. Not the date or the case, but the ultimate outcome. The trend line was clear in a series of cases in the federal courts, and a series of decisions by state legislatures in the United States, and by changes to laws in other countries. Same-sex marriage was coming.

Notwithstanding the writing on the wall, the Church seemed ill-prepared for it. It seemed to me (and this was a source of overwhelming frustration and anger to me personally) the Exclusion Policy as implemented was the worst choice, the most damaging, the least Christian, of all the Church’s reasonably conceivable options.

Then how and why did the policy of treating gay marriage as high rebellion that tainted even the children of a gay marriate get reversed? Here is Chris’s description of the how:

I believe if the Church had internalized the virtual certainty of public disclosure, there would have been recognition that the Policy was a mistake before it was promulgated. As November 2015 happened, I believe there was almost immediate widespread recognition that the Policy was a mistake. I believe the recognition was early enough that we have just lived through 39 months of puzzlement about how to fix it. I view now—President Nelson’s foray into assigning the “revelation” label was a trial balloon for the “shore it up” method of fixing a problem. Once that failed, pragmatic reality required the Church to immerse itself in nuanced and involved dialogue in order to seek consensus at the highest levels as well as some amount of membership support.

Let me give three possible reasons why. The first is a change in personnel. The previous President, Thomas S. Monson, died on January 2, 2018. Russell Nelson has made major changes since then, see “New Mormon Prophet Russell Nelson Shakes Things Up” and “Less is More in Mormon Church Meetings.” The degree of deference to the President of the Mormon Church is so great that it is often difficult for those outside the inner circles to know what the views of another apostle are until they ascend to the Presidency. This is actually true not just for Russell Nelson, whose views are finally being revealed, but especially true for the other 2 in the top 3 leaders in the organizational chart: Dallin Oaks (a former colleague of my Dad’s in the Brigham Young University Law School) who is currently both the #2 in the organization chart and the designated successor if Russell Nelson should die and the #3 in the organization chart, my Dad’s first cousin Henry B. Eyring. Both Dallin Oaks and Henry B. Eyring are very much good soldiers, who will fall in line with whatever policy has been decided on by those more senior then he is. In other words, the views of the entire First Presidency—the troika at the top of the Mormon Church—have been to an important extent hidden by their high levels of loyalty. There is some reason to hope that their views are reasonably liberal when those views are not trumped by loyalty, despite the fact that they have on many occasions publicly espoused extremely conservative views in lockstep with policy. I had not thought of Russell Nelson himself as particularly liberal, but I do think of Russell Nelson as being non-monarchical. Deliberating as a group of three, the combination of Russell Nelson, Dallin Oaks and Henry B. Eyring is plausibly quite a bit more liberal than Thomas S. Monson.

Further down in the line of succession, I don’t have a good sense of the views of 90-year-old M. Russell Ballard. But 78-year-old Jeffrey R. Holland (who attended the same congregation as my family when I was a teenager and he was the President of Brigham Young University) and 78-year-old Dieter F. Uchtdorf are likely to be relatively liberal. (Both of these apostles are higher in the line of succession than Henry B. Eyring.) I emphasize the ages not only as a predictor of vigor but also because other than being appointed an apostle at a young age, long life is the key to become President of the Mormon Church.

The second possible reason for the reversal is that many local leaders may have complained about having to implement the initial harsh policy. In the comments section of Chris’s post, you can find these reports:

cat: I concur. I know of more than a few Bishops and Stake Presidents who publicly announced that the Policy of Exclusion would not be enforced under their stewardship.

Christian Kimball: I too have heard of Bishops and Stake Presidents who worked to minimize the effects of the Exclusion Policy within their scope of influence.

My sense is that, in general, high Mormon Church leaders have a great deal of respect for the local Church leaders, whom they themselves have often personally chosen and appointed out of the set of almost all the adult male members of the Church in a given area.

The third possible reason for the reversal is that the Church has become worried about the slowdown in its growth rate. The article flagged at the top of this post reports that, in the US, the worldwide growth rate of the Mormon Church has slowed from 3 to 8 % per year from 1960 to 2000 to about 1.5% per year now, with the growth rate in the US only 3/4 of a percent per year now. Mormon Church leaders care deeply about the growth rate of the Church. They wouldn’t sacrifice key doctrinal tenets for the sake of growth, but they might be willing to soften their approach toward gay married couples.

Mormon Church leaders care deeply about the growth rate of the Church for many reasons. First, they see it as their job, given them by Jesus, who said to his disciples before ascending to heaven:

Go ye therefore, and teach all nations, baptizing them in the name of the Father, and of the Son, and of the Holy Ghost: Teaching them to observe all things whatsoever I have commanded you …

Notice that this doesn’t just say “teach all nations” but baptize them. Mormon baptism makes one a member of the Mormon Church. So under a Mormon interpretation, this amounts to a command to convert people and bring them into the Mormon Church. In addition to a keen awareness of Jesus’ Great Commission, in its “the-Mormon-Church-is-the-only-true-church” interpretation, many Mormon Church leaders have a business background, in which growth is often a key goal. Finally, at a gut level, most Mormon leaders care about growth as do rank-and-file Mormons because for a long time the fast growth rate of the Mormon Church was seen by those in the Church as a validation of the Church’s claims to have been established by God. The article flagged just below gives a nice description of this mindset, which resonates with my own 40 years as a Mormon during those high-growth years, before I left Mormonism in 2000.

Without any doctrinal change, there is much further that the Mormon Church could go to liberalize. The Mormon Church’s has historically been hard on gays, feminists and free-thinking intellectuals. In relation to gay marriage, Chris suggests that the Mormon Church could continue to consider gay marriages religiously invalid (as, indeed, it considers all marriages not done by the Mormon church in any case), but to be civilly valid, and sufficient to make sex within that marriage something other than a serious sin:

If two men marry, before God and country and friends and family, are they married in the Church’s eyes? Not the question “Will the Church perform the marriages?” Not the question “Will the Church encourage or recommend or celebrate the marriages?” But the very basic question “Does the Church respect the marriages?” In essence, is same-sex marriage a real marriage?

In relation to feminism, without any change in doctrine, and without given women the Mormon priesthood the Mormon Church’s leaders could direct that women be in all the key meetings for the governance of each individual congregation.

For free-thinking intellectuals, it would be a big step forward if Mormon Church leaders simply left them alone to say their piece. No doctrine requires that a particular person be excommunicated for what they have written or said. There is enormous discretion in decisions of whether or not to excommunicate a particular intellectual.

Don't miss these posts on Mormonism:

The Message of Mormonism for Atheists Who Want to Stay Atheists

How Conservative Mormon America Avoided the Fate of Conservative White America

The Mormon Church Decides to Treat Gay Marriage as Rebellion on a Par with Polygamy

David Holland on the Mormon Church During the February 3, 2008–January 2, 2018 Monson Administration

Also see the links in "Hal Boyd: The Ignorance of Mocking Mormonism."

Don’t miss these Unitarian-Universalist sermons by Miles:

By self-identification, I left Mormonism for Unitarian Universalism in 2000, at the age of 40. I have had the good fortune to be a lay preacher in Unitarian Universalism. I have posted many of my Unitarian-Universalist sermons on this blog.

Alexander Bogomolny: Interactive Mathematics Miscellany and Puzzles →

Hat tip to Daniel Arovas. The link above leads to an array of links categorized by math topic and this explanation:

Back in 1996, Alexander Bogomolny started making the internet math-friendly by creating thousands of images, pages, and programs for this website, right up to his last update on July 6, 2018. Hours later on July 7th he passed away.

What Monetary Policy Can and Can't Do

Sluggish, Sticky, Inertial Inflation. There are two big problems with many academic models used to think about monetary policy. First, optimal monetary policy papers often do not include investment in the model. (See “Next Generation Monetary Policy.”) Second, a large share of all sticky price models lack any inflation inertia: if a substantial shock hit the model economy, inflation would instantly jump to a new and quite different value.

One model that does have inflation inertia in it is the model in Greg Mankiw and Ricardo Reis’s paper “Sticky Information Versus Sticky Prices: A Proposal to Replace the New Keynesian Phillips Curve.” The one big difference I have with Greg and Ricardo is that what they speak of as “sticky information” in their title, I think is not imperfect information, but imperfect information processing—something they should have emphasized. People can know things in some sense, but ignore them because the cost of meaningfully and appropriately using that information in decisions is high. (On the difference between imperfect information and imperfect information processing, see “Cognitive Economics.”)

In relation to the majority of macroeconomic models, one of the big mysteries of the Great Recession was why inflation didn’t fall more. In the last few years, one of the big mysteries for the majority of macroeconomic models has been why inflation didn’t rise more. Imperfect information processing is a likely part of the explanation for both: firms that believe that the Fed is trying hard to keep inflation at 2% might feel they don’t have to pay much attention to inflation. It is unlikely that they don’t know when inflation differs from 2% per year; they don’t do much with that information. Then what they do with their own prices tends to reproduce something much closer to 2% inflation than if they were paying attention to the level of inflation.

Let me summarize what I have said so far in this way: in the short-run, central banks cannot control inflation. In recent news, Jerome Powell confirmed this with his own frustration. In Nick Timiraos’s March 20, 2019 Wall Street Journal article “Fed Keeps Interest Rates Unchanged; Signals No More Increases Likely This Year,” Nick reports:

In a particularly revealing admission, Mr. Powell said he was discouraged that inflation hadn’t risen in a more sustainable fashion.

“I don’t feel we have convincingly achieved our 2% mandate in a symmetrical way,” he said. “It’s one of the major challenges of our time, to have downward pressure on inflation” globally.

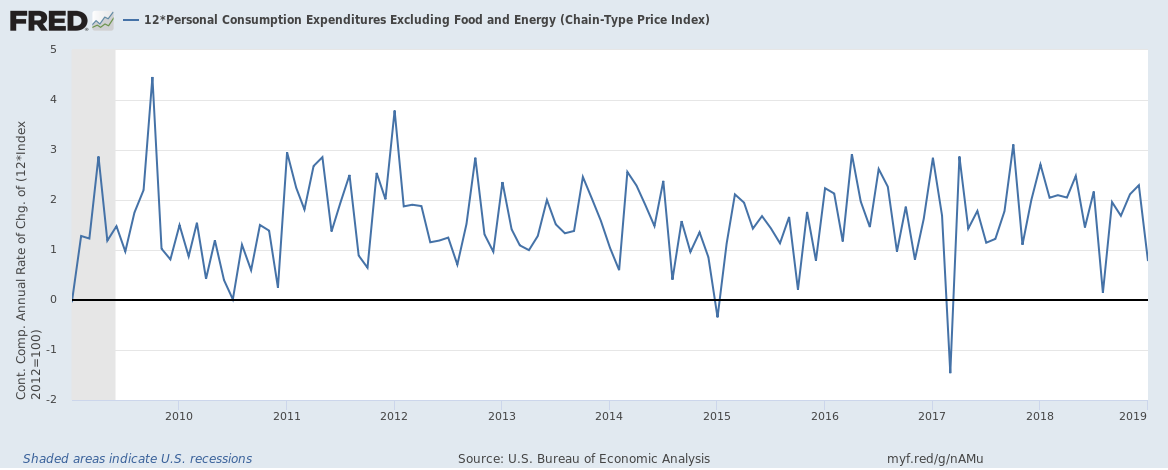

In other words, Jerome Powell, as Chair of the Federal Reserve Board and Chair of its interest-rate-setting Federal Open Market Committee, feels that inflation is changing much more slowly than he would like in response to Fed policy. The Fed has allowed the unemployment to fall below 4% for over a year now, and inflation according to the Fed’s favorite measure (the change in the deflator for personal consumption expenditures excluding food and energy) is lately still bouncing around between 1% and 2%, with an average of about 1.5%, instead of bouncing around between 1.5% and 2.5%, with an average of 2% as the Fed would like.

Personally, I have no doubt that low enough unemployment for long enough would cause inflation to begin increasing. But that is the long run. Leaving aside hyperinflationary situations that change at hyperspeed, in the short-run, central banks cannot control inflation.

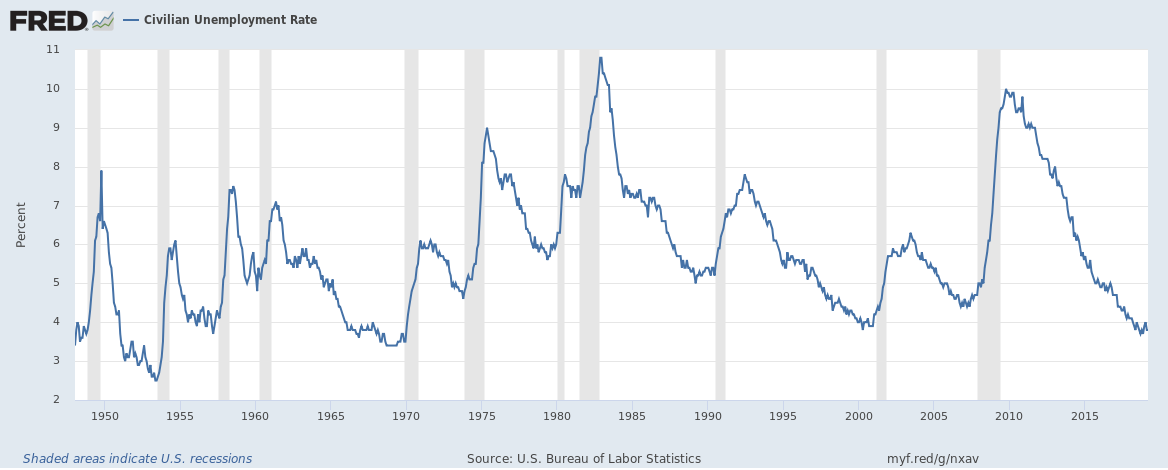

(To emphasize how dramatic the decline in unemployment has been since the depths of the Great Recession, take a look also at this graph of unemployment over a longer period of time:

)

The Classical Dichotomy. Let me now combine the idea that central banks cannot control inflation in the short run with the familiar idea that, simplifying only a little, in the long run central banks can only control inflation. Here, the “only” has a lot of poetic license to it: there are many other things that are closely related to inflation: the rate of increase in any nominal quantity, nominal interest rates, and real money balances. But by and large, all the important real quantities people care deeply about are unaffected by monetary policy in the long run. This is the “Classical Dichotomy” (which I consider to hold in the long-run, but not the short-run). In particular, monetary policy cannot affect the real interest rate in the long run. It is possible that claim is false, but it comes from absolutely standard economic theory—theory that makes sense to me.

How Inertial Inflation Simplifies the Fisher Equation Over Short Horizons. One consequence of how much inertia there is to inflation (in non-hyperinflationary situations), is that over a horizon of a year or two, there isn’t much difference between actual and expected inflation in the Fisher equation. So we can think of the ex ante real interest rate E r as being close to the ex post real interest rate and approximate by writing

r = i - pi

as the definition of the real interest rate, where

r = real interest rate

i = nominal interest rate

pi = inflation

(Ex ante is Latin for “before the fact,” and means the value expected in advance. Ex post is Latin for “after the fact,” and means what actually happens in the end—what one knows with hindsight.)

Eqivalently,

i = r + pi.

The Bottom Line. Putting everything together, let me summarize what central banks can and can’t do in the short run and in the long run:

In the short run, central banks can control the nominal interest rate i, and through it the real interest rate r, but can’t control inflation pi.

Through their control of the real interest rate in the short run, central banks can affect a large number of real variables in the short run.

In the long run, central banks can control inflation pi, and through it the nominal interest rate i, but can’t control the real interest rate r.

Because central banks can’t control the real interest rate in the long run, they can’t control any crucial real variable in the long run. (The biggest exception to the rule that central banks cannot affect real variables in the long run is that inflation and nominal interest rates influence real money balances.)

Update April 11, 2018: Lewis Lehe asks on Twitter:

Lewis: If they don’t affect inflation in the short run, couldn’t a central bank buy up, say, trillions worth of stocks and hold them for a year or so with no adverse consequence? Then the government could get all the dividends and not cause any inflation.

Miles: But while it can affect inflation only slowly, the effect on inflation that it does have is permanent.

This is part of a series of posts I am writing for my Intermediate Macroeconomics class this semester, including some that I wrote in advance. The others so far are:

John Cassidy: The High-Stakes Battle Between Donald Trump and the Federal Reserve →

The link above is to a New Yorker article that is a bit on the hyperventilating side. I think Donald Trump will lose this battle; so at this point there is no need for alarm. But the fact that Donald wants to weaken the independence of the Fed is to his discredit. If Donald Trump thinks the Fed makes too many mistakes in the direction of tightness, a good appointment now would be a Market Monetarist. By contrast, appointing—or trying to appoint—political hacks is destructive of the institution of the Fed.

Layne Norton Discusses the Stephan Guyenet vs. Gary Taubes Debate (a Debate on Joe Rogan’s Podcast)

157 minutes to listen the Stephan Guyenet vs. Gary Taubes debate on Joe Rogan’s podcast is a bit much for me right now. If you want to see the video of the whole podcast yourself, here it is:

However, I did read Layne Norton’s review of the debate, shown at the top. Let me engage with the scientific issues Layne raises. I want to be clear that I am not in this post defending or attacking anything that Stephan Guyenet or Gary Taubes said or didn’t say in the podcast itself. I’ll only be talking about my own views and Layne’s views as he expressed them in his review.

Evidence on the Effect of Insulin on Calories Out. The biggest criticism I have of what Layne says is that he repeatedly acts as if the energy balance or “calories in/calories out” identity were a theory. It only becomes a theory once you specify what determines calories in and calories out. On what determines calories in “in the wild” of people’s actual lives, the metabolic ward studies that Layne refers to repeatedly are uninformative, because they carefully control the amount of calories people consume. On what determines calories out, metabolic ward studies can provide some evidence on purely metabolic effects, Layne doesn’t address the study I discuss in “Framingham State Food Study: Lowcarb Diets Make Us Burn More Calories.” The other effect on calories out is how energetic one feels and therefore how much activity one does. Metabolic ward studies are also not great at showing these effects to the extent that not many activities are available while confined in the metabolic ward. And these studies might often try to standardize the activities of subjects in the studies.

One clue to a problem with the studies that Layne cites is this passage:

He would also likely point out that there was a small increase in energy expenditure on the ketogenic diet (that was near the detection limits of the equipment analyzing it). This difference in energy expenditure was transient during the first week of the ketogenic diet and didn’t last past that and didn’t produce meaningful differences in fat loss. This small increase in initial energy expenditure may likely be from the adaptation period of moving to use ketones & fats for fuels vs. carbohydrate. After that initial adaptation to ketones & fats, the small difference in energy expenditure disappears. In fact, it appears that when calories are equated, fat restriction may produce greater loss of body fat than carb restriction by a small amount.

Since any signal from each subject combined with a large enough sample can overcome any amount of uncorrelated noise, “near the detection limit” is a hint that a study is underpowered statistically. Nothing should be called “small” simply on the basis of having a low level of statistical significance in a small sample. And nothing should be called “small” if it could possibly cause, say, the pound a year weight gain of many American adults that is a description of much of the rise in obesity.

The fact that obesity comes on as slowly as it does for many people means that metaphors about fat being locked in cells (which I have used myself—see “How Low Insulin Opens a Way to Escape Dieting Hell”) when insulin levels are high must be taken as an indicator of direction, not as absolute statements. Layne makes the point I am making nicely in the following passage:

Now we have 2 central themes of the CIM with extremely strong evidence to the contrary. Let’s examine this notion that insulin is a magical fat storing hormone. Gary focuses on short term effects of insulin after a meal on fat storage (particularly around 2:09:35). Yes, insulin drives free fatty acids into cells, but assuming this is the cause of obesity takes a very simplistic view of adipose cell metabolism. Fat is constantly being stored into adipose and released from adipose. It is the net synthesis of fat minus the breakdown of fat in adipose that will determine fat balance and net fat loss or gain (I’m simplifying the model here but it’s accurate for our purposes).

Insulin doesn’t have to inhibit the release of fat from fat cells completely to be an important enough obstacle to fat burning to have a long-run effect. And if insulin levels, while not completely stopping fat burning, inhibit fat burning enough to lead in the long-run to weight gain, it could usefully be called a magical fat storing hormone.

How the Carbohydrate-Insulin Model Works. Let me now turn to what I find Layne’s most interesting paragraph. It’s first sentence is:

Hopefully, you’re convinced that part of the CIM [Carbohydrate-Insulin Model] is not plausible (calories don’t matter only carbs), but we can also rebuke other aspects of it.

There are two ideas here. It would be silly if the Carbohydrate-Insulin Model said that “calories don’t matter.” Calories are part of the causal pathway, the point of the Carbohydrate-Insulin model is that—even focusing on biology apart from psychology—calories are not the beginning of the causal pathway. As I interpret it, the Carbohydrate-Insulin Model emphasizes that—especially for those of us who aren’t in metabolic wards—calories are endogenous; therefore one should focus on the hormonal forces that drive calories in and calories out, rather than immediately jumping to trying to directly control calories in and calories out, as many people attempt to do.

Calories do matter, but the weight-loss strategy most people in our culture follow when they fixate on calories is usually a failure. Focus on eating low on the insulin index and on when you eat and calories in/calories out is likely to move in a direction that leads to weight loss without your directly thinking about calories. (See “Forget Calorie Counting; It's the Insulin Index, Stupid” and “Stop Counting Calories; It's the Clock that Counts.”) Once you have moved to low-insulin-index eating and a short eating window each day, you might want to experiment with thinking about the number of calories you are eating, but thinking about how much you eat should definitely come only third after thinking about what you eat and when you eat.

The reason to focus first on what you eat and when you eat and only then on how much you eat is that your body has decent mechanisms for controlling how much you eat at a sitting when you are eating healthy things, and how much you eat at a sitting puts a reasonable limit on how much you eat overall if you aren’t eating all the time.

Does Insulin Lock Fat in Fat Cells? The remainder of Layne’s most interesting paragraph is:

The idea that insulin traps free fatty acids in cells making the other tissues feel like they are “starving” has also been demonstrated to be incorrect. If this was correct, we would expect to see depleted levels of free fatty acids in blood during fasting in insulin resistant people. But we don’t. Obese people release MORE fatty acids from adipose, not less.

This is not a good argument on Layne’s part. As soon as one recognizes that even fairly high insulin levels do not completely lock fat in fat cells (even though insulin has an effect in that direction), it becomes obvious that number and size of fat cells is a factor in how much fat gets out into the bloodstream as well as insulin levels. So one should compare blood levels of fatty acids during fasting of people who have the same weight and amount of body fat but different levels of insulin to see the extent to which insulin goes in the direction of locking fat in fat cells.

Does Locking Fat in Fat Cells Leave the Rest of the Body Feeling Starved? But wait, Layne has an argument that even if fat is locked in fat cells, that doesn’t lead to hunger that causes one to eat more:

Hold on though, I’m not done crushing the CIM. Remember that one of the core themes of the CIM is that insulin causes fat to be trapped in fat cells and thus we can’t burn it and it’s not accessible to the other tissues of the body so we end up overeating because the rest of our tissues are “starving.” This aspect of the CIM has also been tested (indirectly) using a drug called acipimox which inhibits release of fats from adipose tissue. Not only did the subjects taking the drug not get fatter but they also did not increase their caloric consumption relative to the placebo group. [8: Makimura, H., Stanley, T. L, et. al. (2016, March). Metabolic Effects of Long-Term Reduction in Free Fatty Acids With Acipimox in Obesity: A Randomized Trial. Retrieved from https://www.ncbi.nlm.nih.gov/pubmed/26691888]

The problem with this argument is that the people in this this Acipimox trial were eating freely, which for most Americans means eating almost all the time. If you are getting plenty of sugar and fats in your bloodstream from food you have just eaten, you don’t need fat from your fat cells in order to keep hunger at bay. It is when trying to lose weight that having plenty of fatty acids in the bloodstream from your fat stores is crucial for not feeling hungry. My prediction is that taking Acipimox would make it more painful to fast and more painful to try to lose weight when using the common strategy of reducing calories while keeping one’s schedule of eating unchanged. It is a very different experiment to see if Acipimox gets in the way of attempts at weight loss than whether it causes weight gain.

The study claimed benefits of Acipimox. Such benefits are reasonably plausible: if one is eating enough that the fatty acids in the bloodstream from one’s own fat cells wouldn’t (on net) get used, those extra fatty acids are not really helpful and might have some undesirable side effects.

One of my most important contentions is that insulin above a certain level makes it painful to cut back on calories. So it is better to both stick to low-insulin-index foods and to go to the extreme for certain periods of cutting calories back to zero so that insulin levels go low enough that the gates are wide open for fat to come out of the fat cells. When you cut back on calories, you need energy resources from your fat cells to take up the slack, and high insulin levels interfere with that. A few calories of high-insulin-index foods could easily make you quite miserable on a low-calorie diet—much more miserable than you would be eating nothing at all. And far from being miserable, you might not suffer much at all eating nothing if the last things you ate before fasting was food that is low on the insulin index. (Fasting here means drinking water—and maybe unsweetened tea or coffee—but not eating food.)

Exercise. One place where both Layne and I disagree with Gary Taubes is this:

Gary also states in the debate that exercise doesn’t really matter (see 1:42:10). If that was the case, where are all the fat marathon runners who eat high carb diets? Where are all the pro athletes gaining massive amounts of weight on high carb diets?

I said my piece on exercise in last Tuesday’s post: “On Exercise and Weight Loss.” The most relevant point there is that exercise is very valuable for avoiding gaining weight, but much less helpful for losing weight.

Gary Taubes. When I listen to most people, including Gary Taubes, I habitually try to turn what they are saying into the strongest version of the argument that I can come up with. Then I focus on my version of the argument. That makes me value people who have a take on things that provokes useful thoughts. Gary Taubes is one of those people. I can see that he might be frustrating to people who, instead of taking his arguments and improving on them, can only see his arguments as stated. I have yet to meet anyone who is right all the time or anyone who is wrong all the time. But I feel that Gary’s ideas are in a very useful direction—a direction that can be converted into testable science by those whose business it is to turn rough ideas into testable science.

Update, April 9, 2019: Layne Norton and other respond on this Twitter thread.

Layne Norton: good attempt at a rebuttal I guess. But your point about low carb causing greater energy expenditure and that @KevinH_PhD 's may have been underpowered (not based on previous data) ignores the other 30 studies looking at the same thing and actually slightly favoring low fat on EE

Kevin Hall: Our ketogenic diet study was powered to detect a 150 kcal/d effect size for the primary outcome. This was pre-specified in the protocol to be the minimum physiologically important effect on 24hr EE & signed-off by @NuSIorg. The null result led to shifting goalposts by @garytaubes

Sarong Joshi: If the bmj study is correct and LC increases metabolic rate And majority of hunter gatherers for majority of the part were low carbers And if optimum foraging strategy is correct That would just mean LC has least return on investment, evolution would've wiped out low carbers

I should say that, whatever Gary Taubes said, something less than 150 “calories” (technically, the usual calorie is a “kilocalorie”) a day, say 100 calories a day, is still an important effect. (Sarong’s argument is robust to that point.)

Don’t miss my other posts on diet and health:

I. The Basics

Jason Fung's Single Best Weight Loss Tip: Don't Eat All the Time

What Steven Gundry's Book 'The Plant Paradox' Adds to the Principles of a Low-Insulin-Index Diet

David Ludwig: It Takes Time to Adapt to a Lowcarb, Highfat Diet

II. Sugar as a Slow Poison

Best Health Guide: 10 Surprising Changes When You Quit Sugar

Heidi Turner, Michael Schwartz and Kristen Domonell on How Bad Sugar Is

Michael Lowe and Heidi Mitchell: Is Getting ‘Hangry’ Actually a Thing?

III. Anti-Cancer Eating

How Fasting Can Starve Cancer Cells, While Leaving Normal Cells Unharmed

Meat Is Amazingly Nutritious—But Is It Amazingly Nutritious for Cancer Cells, Too?

IV. Eating Tips

Using the Glycemic Index as a Supplement to the Insulin Index

Putting the Perspective from Jason Fung's "The Obesity Code" into Practice

Which Nonsugar Sweeteners are OK? An Insulin-Index Perspective

V. Calories In/Calories Out

VI. Other Health Issues

VII. Wonkish

Framingham State Food Study: Lowcarb Diets Make Us Burn More Calories

Anthony Komaroff: The Microbiome and Risk for Obesity and Diabetes