Alexander Trentin: "Japan, It's Time to Finally Overthrow Cash!"

Link to the article on the Finanz und Wirtschaft website

Some of the best reporting ever on my proposal to eliminate the zero lower bound is in German. I am delighted by Alexander Trentin’s article “Japaner, shafft endlich das Bargeld ab” on the Finanz und Wirtschaft site. (“Finanz und Wirtschaft” means “Finance and Economics.”) And I am very grateful for his permission to publish an English translation here.

This article is closely related to my column “Righting Rogoff on Japan’s Monetary Policy,” but I recommend reading this one first. Also, I can’t fail to mention the news this week that the Swiss National Bank has gone to negative interest rates. I wrote about that in my latest Quartz column: “The Swiss are now at a negative interest rate due to the Russian ruble collapse.”

Below the row of stars is my translation of Alexander Trentin’s words, with the help of my college German, Google translate, and my knowledge of the substance. Based on substance, I translated “abschaffen” as “overthrow” instead of “abolish” because I don’t advocate abolishing cash, only demoting it. Similarly, I translated “solange es den Yen noch als Bargeld gibt” to “as long as cash still rules in Japan” instead of “as long as there is yen as cash” for the same reason. The Tokugawa Shogunate was overthrown with the slogan “Honor the Emperor and expel the barbarians!" The right slogan for Japan now is "Honor the electronic yen and end the lost decades!”

Has the Bank of Japan really done everything possible to create inflation? No, says a US economist, as long as cash still rules in Japan.

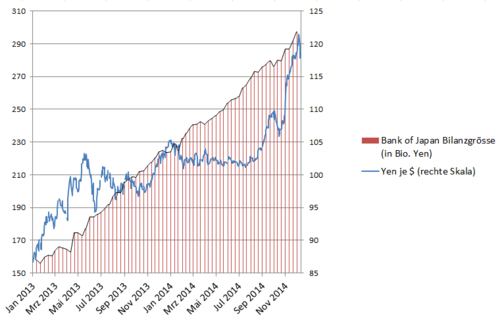

The Bank of Japan wants inflation. To that end, it expanded its bond purchase program (QE) in late October. The currency markets are impressed. The central bank balance grows with those purchases, while the yen’s exchange rate vis a vis the dollar weakens:

Source: Bloomberg. Red stripes, left scale: BOJ balances in trillions of yen. Jagged blue line, right scale: Yen per US dollar.

But stimulating growth by stimulating inflation is much more difficult than devaluing the currency. In the last two quarters, the economy contracted. And in October, prices fell again. The temporarily high inflation of 2% in April was achieved by increasing the consumption tax. Now, the decline in oil prices has lowered inflation expectations in Japan.

Source: Bloomberg. Red bars, left scale: quarterly growth in GDP. Blue line, right scale: inflation in the previous month.

The consensus among market analysts is that the Bank of Japan has fulfilled its task. And it has been expanding its QE program. Harvard economist Kenneth Rogoff argued recently that structural reform is the only hope for Japan’s economy, because the Bank of Japan has done all it can: that is the only way Japan can get out of deflation and low growth.

But is this really true? For Miles Kimball, a professor at the University of Michigan, it isn’t true that the Bank of Japan has really tried everything. Because the Japanese could cut interest rates. They are already at zero, but Kimball is one of the economists who advocate electronic money instead of paper money to make it possible to charge negative interest rates. If there were no more cash, you couldn’t use paper money to save yourself from negative interest rates in your bank account–negative interest rates that have already been introduced in certain German banks for business customers. On Twitter, Miles Kimball writes:

The Japanese are interested

He presented his view last year at the Bank of Japan and Japan’s Ministry of Finance. And according to Kimball’s website, the Central Bank and the Ministry of Finance were “interested” in his proposal.

In Kimball’s proposal, paper currency would continue to exist, but prices would be expressed in units of electronic money. There would be a time-varying exchange rate between electronic money and paper money. “We wouldn’t have to worry about [central banks] ever again seeming relatively powerless in the face of a long slump" Kimball writes in a column.

Absolute price stability is possible

But Kimball is no fan of inflation who wants to make the money in our pockets or in our bank accounts worth continually less and less. On the contrary, he argues that the possibility of negative interest rates makes the generally accepted inflation target of 2% unnecessary. An inflation target of 0%–that is, absolute price stability–would then be possible.

His reasoning: Central banks want an inflation rate of 2% so they have room to push the real interest rate low enough. The real interest rate is the nominal interest rate minus the inflation rate. For investment decisions, the real interest rate is crucial. If the nominal interest rate can’t go below 0%, an inflation rate of 2% is needed to make a real interest rate of -2% possible. However, if the nominal interest rate can be negative, then a central bank no longer needs to get the leeway for negative real interest rates from a positive rate of inflation.

"The benefits of true price stability alone would easily make up for any inconvenience of [electronic money,]” believes Kimball. If the Bank of Japan cannot generate persistent inflation even after continued huge bond purchases, maybe Japan will be the first nation to overthrow paper money.