Andy Rachleff: What "Disrupt" Really Means →

I found this discussion by Andy Rachleff of the Clay Christensen’s idea of a “disruptive” business model very interesting. Clay Christensen himself recommended this piece in a tweet.

A Partisan Nonpartisan Blog: Cutting Through Confusion Since 2012

I found this discussion by Andy Rachleff of the Clay Christensen’s idea of a “disruptive” business model very interesting. Clay Christensen himself recommended this piece in a tweet.

For the first time in six centuries, a Pope is resigning. I admire Pope Benedict’s willingness to face forthrightly the reality of how advancing age has affected his ability to perform his duties by handing off leadership to another Pope to be chosen soon by the College of Cardinals.

Although I have no special insight into the inner workings of the Catholic Church, I saw the last years of my grandfather, Spencer W. Kimball, who remained President and Prophet of the Mormon Church from 1974 until the day he died in 1985 at the age of 90. At the age of 83 (in 1978), he declared that he had received a revelation from God that the Mormon priesthood–and all of the ceremonies in Mormon temples–should be opened to those of African ancestry, who had previously been barred from ordination to the priesthood and full participation in Mormon temple ceremonies. But from at least age 86 on, my grandfather was seldom up to carrying on a normal conversation. His position as leader of the Mormon Church still mattered because other Mormon Church leaders tried to do what they thought he would have, but the decisions he himself made were at the level of nodding his head to something suggested by one of his lieutenants—especially the then relatively young Gordon B. Hinckley, who later went on to lead the Mormon Church in a very visible way because of his high level of comfort with the news media.

My grandfather believed it was his duty to serve as head of the Mormon Church until God released him from that position by death. Part of his reasoning was the tradition within the Mormon Church that upon the death of the Prophet, the longest-serving surviving Apostle becomes the new Prophet. Thus, he believed that the timing of his own death might be part of the way in which God chose who would become the next Prophet. For Pope Benedict, there is no such consideration, since the next Pope is chosen by the decision of the College of Cardinals rather than by life and death. But still, he had to buck six centuries worth of tradition that Popes serve until the day they die—a span of time more than three times as long as the Mormon Church has been in existence.

All of us face death, and many of us will face serious disability before death. Forthrightly admitting those possibilities to ourselves–and dealing with their actual arrival with grace, as Pope Benedict has–can both help us lead a good life and help ensure that those people and causes we love are taken care of when we are gone or fading, in body or mind.

Thanks to Yannis Varoufakis for pointing me to this interesting article. I think massive multiplayer online role-playing games have a lot of as-yet-only-partially-tapped potential both for experiments and for teaching.

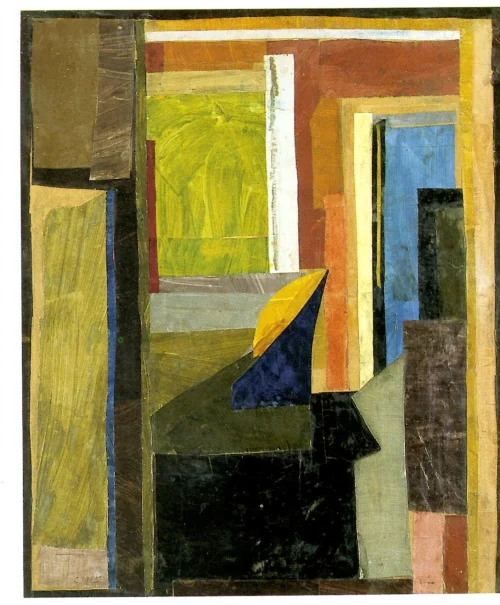

I posted this originally simply because it is beautiful, but Ian Preston pointed out that the interior depicted is 46 Gordon Square, where John Maynard Keynes lived! Along with my economist dinner companions, I made a pilgrimage to see the plaque on the outside of the building after giving a seminar on the Economics of Happiness at LSE in June 2011. Here are some walking tour directions that Ian Preston tweeted.

Isomorphismes is one of my favorite Tumblogs. Here is a math post I liked.

Going the long way: What does it mean when mathematicians talk about a bijection or homomorphism?

Imagine you want to get from X to X′ but you don’t know how. Then you find a “different way of looking at the same thing” using ƒ. (Map the stuff with ƒ to another space Y, then do something else over in image ƒ, then take a journey over there, and then return back with ƒ ⁻¹.)

The fact that a bijection can show you something in a new way that suddenly makes the answer to the question so obvious, is the basis of the jokes on www.theproofistrivial.com.

In a given category the homomorphisms Hom ∋ ƒ preserve all the interesting properties. Linear maps, for example (except when det=0) barely change anything—like if your government suddenly added another zero to the end of all currency denominations, just a rescaling—so they preserve most interesting properties and therefore any linear mapping to another domain could be inverted back so anything you discover over in the new domain (image of ƒ) can be used on the original problem.

All of these fancy-sounding maps are linear:

Fourier transform

Laplace transform

taking the derivative

Box-Müller

They sound fancy because whilst they leave things technically equivalent in an objective sense, the result looks very different to people. So then we get to use intuition or insight that only works in say the spectral domain, and still technically be working on the same original problem.

Pipe the problem somewhere else, look at it from another angle, solve it there, unpipe your answer back to the original viewpoint/space.

“Going the long way” can be easier than trying to solve a problem directly.

The top 25 posts on supplysideliberal.com listed below are based on Google Analytics pageviews from June 3, 2012 through February 11, 2013. The number of pageviews is shown by each post. (There were 195,923 pageviews during this period, but, for example, 66,802 homepage views could not be categorized by post.) I have to handle my Quartz columns separately because that pageview data is proprietary. So there I am giving only the order in the Top 10 list immediately below. The list of top posts would be quite misleading without the inclusion of the Quartz columns. You might also find other posts you like in this earlier list of top posts, at this link.

For those who want to find this post again, the “Top 25 posts in order of popularity” button at my sidebar will link to it until I make another post like this.

As economists, it is important for us to pay attention to the unintended side effects of our usual initial working assumption that people are fully optimizing–doing the best they can given the situations they are in. To the extent we treat this not just as an initial working assumption, but as if it were the God’s truth, we are in danger of missing opportunities for helping people make better decisions.

Fortunately, economists don’t routinely assume that those in government are always optimizing. Instead, a routine starting point for policy analysis is to act as if those in government want to improve the general welfare (along with some more self-interested motives), but don’t always know how. In an excellent Project Syndicate essay, “The Tyranny of Political Economy,” Dani Rodrik writes about the learned helplessness that can result if one follows to a logical conclusion the assumption that those in government are already fully optimizing–often in a self-serving way–subject to their constraints. He argues that new ideas and advice can make a difference.

Dani Rodrik worries that the logic of optimization is leading economists to doubt, on principle, whether policy advice can make any difference. I worry that the logic of optimization is leading economists to doubt, on principle, whether advice to households or firms can make any difference. If we assume people are already optimizing, where in fact they are not, then we will be blind to opportunities to help. If individuals are optimizing 95% of the way, the approximation that they are optimizing 100% of the way could well be an appropriate simplification in building a larger model, but when focusing attention on that decision, it still leaves a 5% leeway for improvement. That 5% improvement in decision-making could correspond to a large increase in welfare–an especially important opportunity because the increase in welfare from better decision-making would require no coercive action, but only persuasion based on the hearer’s appropriate self-interest.

From John Stuart Mill's On Liberty, Chapter 2–“Of the Liberty of Thought and Discussion”:

Our merely social intolerance kills no one, roots out no opinions, but induces men to disguise them, or to abstain from any active effort for their diffusion. With us, heretical opinions do not perceptibly gain, or even lose, ground in each decade or generation; they never blaze out far and wide, but continue to smoulder in the narrow circles of thinking and studious persons among whom they originate, without ever lighting up the general affairs of mankind with either a true or a deceptive light. And thus is kept up a state of things very satisfactory to some minds, because, without the unpleasant process of fining or imprisoning anybody, it maintains all prevailing opinions outwardly undisturbed, while it does not absolutely interdict the exercise of reason by dissentients afflicted with the malady of thought. A convenient plan for having peace in the intellectual world, and keeping all things going on therein very much as they do already. But the price paid for this sort of intellectual pacification, is the sacrifice of the entire moral courage of the human mind. A state of things in which a large portion of the most active and inquiring intellects find it advisable to keep the general principles and grounds of their convictions within their own breasts, and attempt, in what they address to the public, to fit as much as they can of their own conclusions to premises which they have internally renounced, cannot send forth the open, fearless characters, and logical, consistent intellects who once adorned the thinking world. The sort of men who can be looked for under it, are either mere conformers to commonplace, or time-servers for truth, whose arguments on all great subjects are meant for their hearers, and are not those which have convinced themselves. Those who avoid this alternative, do so by narrowing their thoughts and interest to things which can be spoken of without venturing within the region of principles, that is, to small practical matters, which would come right of themselves, if but the minds of mankind were strengthened and enlarged, and which will never be made effectually right until then: while that which would strengthen and enlarge men’s minds, free and daring speculation on the highest subjects, is abandoned.

Those in whose eyes this reticence on the part of heretics is no evil, should consider in the first place, that in consequence of it there is never any fair and thorough discussion of heretical opinions; and that such of them as could not stand such a discussion, though they may be prevented from spreading, do not disappear. But it is not the minds of heretics that are deteriorated most, by the ban placed on all inquiry which does not end in the orthodox conclusions. The greatest harm done is to those who are not heretics, and whose whole mental development is cramped, and their reason cowed, by the fear of heresy. Who can compute what the world loses in the multitude of promising intellects combined with timid characters, who dare not follow out any bold, vigorous, independent train of thought, lest it should land them in something which would admit of being considered irreligious or immoral? Among them we may occasionally see some man of deep conscientiousness, and subtle and refined understanding, who spends a life in sophisticating with an intellect which he cannot silence, and exhausts the resources of ingenuity in attempting to reconcile the promptings of his conscience and reason with orthodoxy, which yet he does not, perhaps, to the end succeed in doing. No one can be a great thinker who does not recognise, that as a thinker it is his first duty to follow his intellect to whatever conclusions it may lead. Truth gains more even by the errors of one who, with due study and preparation, thinks for himself, than by the true opinions of those who only hold them because they do not suffer themselves to think. Not that it is solely, or chiefly, to form great thinkers, that freedom of thinking is required. On the contrary, it is as much and even more indispensable, to enable average human beings to attain the mental stature which they are capable of. There have been, and may again be, great individual thinkers, in a general atmosphere of mental slavery. But there never has been, nor ever will be, in that atmosphere, an intellectually active people. When any people has made a temporary approach to such a character, it has been because the dread of heterodox speculation was for a time suspended. Where there is a tacit convention that principles are not to be disputed; where the discussion of the greatest questions which can occupy humanity is considered to be closed, we cannot hope to find that generally high scale of mental activity which has made some periods of history so remarkable. Never when controversy avoided the subjects which are large and important enough to kindle enthusiasm, was the mind of a people stirred up from its foundations, and the impulse given which raised even persons of the most ordinary intellect to something of the dignity of thinking beings.

It was a very interesting seminar when Gita came to Michigan to present the paper described in this excellent Bloomberg article.

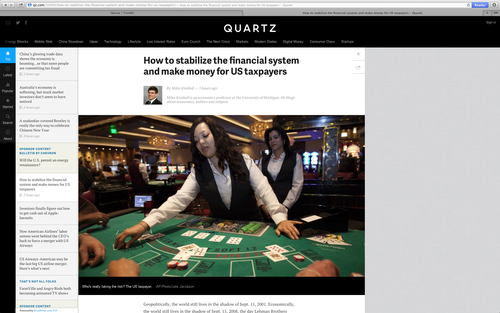

Here is a link to my 15th column on Quartz: “How to stabilize the financial system and make money for US Taxpayers.” My proposal for A US Sovereign Wealth Fund is about more than monetary policy.

Since I am teaching in the second-year macroeconomic field sequence this year, I have been thinking about the objectives for my teaching. I see three goals for a Ph.D. course:

a. For straight theory, the development of mathematical intuition is the key for predicting what a project might lead to.

b. For empirical work, key skills for predicting what a project might lead to are

- understanding identification,

- understanding the sources and characteristics of measurement errors,

- understanding at least rudimentary power analysis in the sense of knowing something about what goes into the standard errors one is likely to get, and

- understanding that the data are endogenous in two very different senses: (i) data from naturally occurring situations come from a complex web of causal relationships and forces and (ii) economists can cause data to come into existence through surveys, field experiments and lab experiments to help fulfill their research objectives.

c. For computational work, such as a project using a Dynamic Stochastic General Equilibrium model, or a project simulating life-cycle consumption, labor supply and portfolio behavior, some key skills for predicting the likely behavior of a model are

- understanding general comparative statics and comparative dynamics results;

- understanding general principles about how models behave, such as key neutrality results that cut across large classes of models and often require intentional modeling devices in order to break (monetary neutrality, Ricardian neutrality, Modigliani-Miller, Wallace neutrality, etc.)

- knowing how to design a set of graphs to get to the heart of what is going on in a model: graphs that serve the purpose for that advanced model that supply and demand serve for Economics 101 (see for example the graphs in my paper “Q-Theory and Real Business Cycle Analytics”); and

- knowing how to compute quantitative results for a few simple models by hand in order to get a sense of the likely size of various effects. (You can see an example of what I mean in some of the chapters of my draft textbook “Business Cycle Analytics.”)

Of course, in all of these areas, research experience and seeing what other people have done–both in published articles and in work presented in seminars–will also help one predict what a project will lead to. Unfortunately, seeing what other people have done is most helpful in understanding paths that are already well-trodden. But sound criticism of what other people have done is immensely helpful in teaching what to avoid. (Helpful hint: when reading papers, be very suspicious of what is claimed in abstracts. At least half the time, abstracts misrepresent what a paper has really accomplished.) Whether one’s own research experience ultimately leads to unique insight into the likely outcomes of various potential projects depends on the directions one strikes out in during the early days of one’s research career.

Yesterday I was on HuffPost Live for the first time. I had a chance to make the case for electronic money and for Adam Ozimek’s idea of region-based visas. Here is the link again: “The Wrong Debate."

There were a couple of things I wanted to make sure to get in, so I wrote a couple of notes beforehand. Here are those two notes:

Of course, these lines mutated when I was actually on the spot, but I did get a chance to say them in my first two at-bats.

I knew the question about immigration policy (my third bit) was coming, so I didn’t need to mention it in the first instance. And I was confident I could say what I wanted to about that more extemporaneously, since I was just coming off of Immigration Tweet Day.

Here are the tweets I was able to storify for Immigration Tweet Day. I tried to storify just the original tweet, rather than all the retweets, but I suspect that in various ways there is some duplication.

Immigration Tweet Day was everything I could hope for. I was especially pleased to see the strong moral dimension to many of the arguments. Like Abraham Lincoln, who was very careful in how he handled the Emancipation Proclamation, I hope we will have a clear moral compass about immigration, working to change hearts and minds, but also be smart about political strategy.

I appreciate the contribution the minority who were against open immigration made to the discussion. It really sharpened the arguments.

Think of a Neoclassical model with inelastic labor supply (including inelastic retirement timing). I am going to focus on the effects that occur in the period of time before capital has had much chance to adjust. To keep the numbers simple, let’s imagine there are 100 million workers in the economy. Production is Cobb-Douglas (see my post “The Shape of Production: Charles Cobb’s and Paul Douglas’s Boon to Economics”), with the following shares:

What are the economic effects of allowing 1 million new workers: enough additional immigration to increase the population by 1%?

Case 1: All of the New Immigration is Unskilled. If all of the new immigration is unskilled, the amount of unskilled labor increases by 2% (from 50 million to 51 million). This increases output by .25 * 2% = .5 %. Unskilled labor gets ¼ of this bigger pie. With a .5% bigger pie and 2% more people to share it among, unskilled workers get a 1.5% reduction in their wage. The skilled workers get the same share of a bigger pie, with no dilution, so they each get a .5 % increase in their wage. Capital also gets .5% more. This helps people in saving for retirement.

Case 2: All of the New Immigration is Skilled. Now the pie is .5 * 2% = 1% bigger (from 50 million to 51 million). With a 1% bigger pie and 2% more people to share it among, each skilled worker now gets 1% less. Unskilled workers get the same share of a bigger pie, with no dilution, so they each get a 1% increase in their wage. Capital also gets 1% more, which helps people in saving for retirement.

Case 3: 60% of the New Immigration is Skilled, 40% Unskilled. In this case, the amount of skilled labor increases by 1.2% (from 50,000,000 to 50,600,000), while the amount of unskilled labor increases by .8% (from 50,000,000 to 50,400,000). This increases output by (.5 * 1.2%) + (.25 * .8%) = .6% + .2% = .8%. Capital gets .8% more, which helps people in saving for retirement. Since there are .8% more unskilled workers to divide their share of the pie among, the unskilled wage is unaffected. The effect on the skilled wage is .8% - 1.2% = -.4% in this simple model.

Everything left out of this bare bones model suggests that in a richer model, output will ultimately grow more. If the skilled workers are willing to bet that the combination of higher returns to capital and the effects of capital accumulation, extra technological progress, the benefits of increasing returns to scale and diversity, and the share of the national debt and of unfunded government liabilities that immigrants will shoulder would make up for the -.4% reduction in wages they see in the bare bones model, the unskilled workers have no reason to object (except perhaps for cultural reasons), since even in the bare bones model, their wage is unaffected, and all other factors then push in the direction of doing better economically.

I suspect that something like the bare bones model of immigration lurks in the back of many brains, and is encoded as saying that immigration is good for capitalists, but not for workers. Therefore, to successfully argue their case, advocates of immigration must confront this bare bones model head on, explain what is missing, and convincingly argue what the quantitative effects of those missing pieces are.

Tweets here and below:

liucid is a tumblog I follow on Tumblr. This reblog from derelictmetropolis struck me as so beautiful I couldn’t help wanting to post it.

Entspannung vor’m Kamin (by tonal decay ⇋ realname)

This column gives a better overall picture of my economic policy stance than any other single post so far. From the conclusion:

Franklin Roosevelt famously said:

The country needs and, unless I mistake its temper, the country demands bold, persistent experimentation. It is common sense to take a method and try it: If it fails, admit it frankly and try another. But above all, try something.

We at such a moment again. The usual remedies have failed. It is time to try something new. Any one of these proposals could make a major difference. In combination, they would transform the world.

Evidence that the publisher Hay House thought that in 2006 people would be interested in “reaching for yield.” (No recommendation intended.)

Many readers have misunderstood the following passage in my recent post “Contra John Taylor” about the effects of interest rates on risk-taking. I was responding to John Taylor’s following argument:

The Fed’s current zero interest-rate policy also creates incentives for otherwise risk-averse investors—retirees, pension funds—to take on questionable investments as they search for higher yields in an attempt to bolster their minuscule interest income.

What I wrote in response was this:

I can’t make sense of this statement without interpreting it as a behavioral economics statement about some combination of investor ignorance and irrationality and fraudulent schemes that prey on that ignorance and irrationality. The often-repeated claim that low interest rates lead to speculation cries out for formal modeling. I don’t see how such a model can work without some combination of investor ignorance and irrationality and fraudulent schemes preying on that ignorance and irrationality.

What I did not say clearly enough is that I have no problem believing that, indeed, investor ignorance and irrationality and schemes that prey on that ignorance and irrationality do indeed cause people to take on more risk as a result of low interest rates than they otherwise would. This is a genuine cost to the Fed stimulating the economy with low interest rates. But– especially once we figure out the details–it has much bigger implications for financial regulation than for monetary policy. I wanted to object to John Taylor’s using “reaching for yield” to criticize current monetary policy without discussing the implications “reaching for yield” has for financial regulation. Regulation has serious costs, but so does tight monetary policy in the current environment. So either we need to live with the costs of “reaching for yield” or we need to consider the costs and benefits of various remedies. Let me add more investor education to the list of potential remedies. So as alternatives to living with the costs of “reaching for yield” we need to consider

To me, it seems clear that tighter monetary policy is the worst of these three options–not only because that would have a high change of causing another recession, but also because the effectiveness of tighter monetary policy in helping investors make better decisions is likely to be quite small. I would love to go with the third option of more investor education, but the costs of that option will only be manageable if effective educational interventions short of having everyone get a degree in finance can be found. That is not easy. (I am making no claim that a degree in finance would do the trick as an educational intervention, only that we would need something that is effective and costs less than having all investors get a degree in finance.)

I am serious in thinking it is important to develop formal models of “reaching for yield.” Let me give that explicitly as advice to Ph.D. students looking for dissertation topics. Here is tgmoe:

A while back I replied to a blog on dissertation topics suggesting I was interested in topics in finance, but I never got around to providing detail. I will do so now. I am interested in the mutual fund industry and how individual households make investment decisions. The evolution of planned sponsors and other institutional investors in this environment is also intriguing and has significantly altered the manner in which households invest. Any thoughts would be greatly appreciated. Thanks, Todd

Answer: To me, modeling “reaching for yield” and testing your model and other models against data on individual investor decisions seems like a great topic for your research. I just storified a Twitter conversation that might be helpful. Here is the link:

In addition, let me suggest the following idea. Suppose someone wants to commit financial fraud–think Bernie Madoff. In a way that might itself be irrational, in the real world, low interest rates seem to be associated with investors expecting a low percentage of the value of an investment being paid back each year. If expectations for the percentage of the value of an investment that is paid back each year are low, it is much easier to hide financial fraud. By contrast, if after a few years start-up period, if people expect substantial dividends or other payments paid out, then it is harder to hide financial fraud. Another to put it is that in a Ponzi scheme, the rate at which one must find additional investors to defraud is lower when people don’t expect fast payback. In some models, the rate of expected payback is the real interest rate, but it is possible that in the world, it is closer to the nominal interest rate. In any case, the details of the path over time at which investors expect to be paid back matters a lot for how long a fraudulent scheme can last. And the level of interest rates is likely to affect the payback path required by investors.

A couple of final thoughts.

Update: Karl Smith just wrote a very interesting post asking the question, as I did in some of my tweets in Reaching for Yield:

By ‘Reaching for Yield,’ Do You Mean 'Demand Curves Slope Downwards’?“

This is an important challenge to those arguing that low interest rates cause people to make mistakes in their decisions about which assets to invest in. Much of the evidence people point to when they talk about "reaching for yield” could be about perfectly rational responses to an increase in the risk premium. This rational response needs to be carefully distinguished from any claim that people are doing too much reaching for yield when interest rates fall–my point 2 just above. I may be more sympathetic than Karl to the idea that at least some people respond in maladaptive ways to low interest rates–enough to worry about. But the evidence is too thin to know how much of an issue this is once the rational response to higher risk premia is separated out.

Let me explain a bit better what a fall in the safe interest rate does. Suppose there is some benchmark level of risk for which the expected average rate of return is unaffected. Then a reduction in the safe interest rate

The second consequence should be no surprise: in general, reductions in interest rates are a relief for borrowers but painful for savers. The pain for savers of lower interest rates is a topic for other posts. The issue for this post is only if that pain drives some savers to make serious mistakes in their asset choices.