“Chris House is right, … having a medal from Sweden doesn’t mean that you’re wise, or even sensible. And it certainly doesn’t grant you the right to have your opinion treated as gospel. Maybe the prize entitles you to a hearing, but no more than that; from there on, it’s the quality of the argument that matters. And if an economist, no matter how credentialed, consistently makes low-quality arguments, he should be tuned out — whereas someone who consistently makes very good arguments deserves attention, even if he or she lacks impressive-sounding formal credentials.”

João Marcus Marinho Nunes on Japan's Monetary Policy Experiment

There have been many disputes about the effectiveness of the large scale purchases of long-term and risky assets by a central bank that we have all fallen into calling QE. In June 2012, I wrote in “Future Heroes of Humanity and Heroes of Japan”:

Noah [Smith] points out that macroeconomists have been arguing over the same things for a long time with no resolution; only decisive central bank actions have provided “experimental” evidence strong enough to convince most macroeconomists of something they didn’t already believe. Just so, massive balance sheet monetary policy on the part of the Bank of Japan could put to rest the idea that balance sheet monetary policy doesn’t work. The Bank of Japan has amazing legal authority to print money and buy a wide range of assets, and has the rest of the government actually pushing for easier monetary policy. So they could do it. They just need to buy assets chosen to have nominal interest rates as far as possible above zero in quantities something like 30% or more of annual Japanese GDP. Japan needs monetary expansion, particularly if it is going to raise its consumption tax, and would be doing the world a huge service by settling the scientific question of whether Wallace neutrality applies to the real world.

… the value of experimentation in economic policy is vastly underrated: trying a policy of “print money and buy assets” on a massive scale such as 30% or more of the value of annual GDP is the way to find out. And there is no country in the world for which the possible side effect of permanently higher inflation would be more harmless. The Bank of Japan has officially set an inflation target at 1%, which is 1% higher than where Japan is at, and there would be nothing terrible about having a 2% inflation target, like the inflation targets for the Fed and the European Central Bank. So the Bank of Japan should do it. If the Bank of Japan shifts to such a decisive policy, those pushing for this approach on its monetary policy committee will ultimately go down in history as heroes of humanity as well as heroes of Japan.

After having seen decades of feckless Japanese monetary policy, I was as surprised as anyone when now Prime Minister Shinzo Abe ran an election campaign centering on monetary policy, and with his election victory in December 2012 and the appointment of Haruhiko Kuroda to the Bank of Japan turned Japanese monetary policy around.

João Marcus Marinho Nunes provides an early read on the results of the Japanese monetary policy experiment in his post “‘Abenomics’ one year on.” What Marcus finds is impressive. I am grateful to him for permission to mirror his blog post in full here.

Shinzo Abe was elected in December 2012 on a promise to revive growth and put an end to deflation. How have his promises ‘performed’ one year after taking power?

The ‘performance’ will be illustrated by a set of charts.

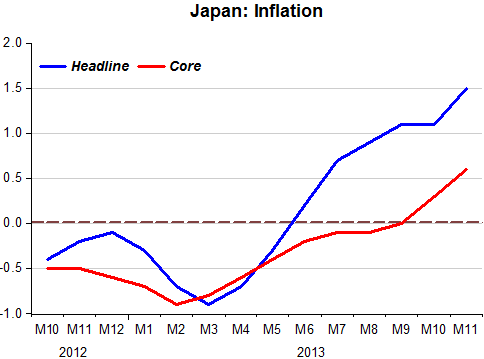

The first chart shows the behavior of inflation, both headline and core.

It appears to be gaining ‘positive traction’ after years of languishing in deflationary territory.

The next chart shows the bounce in aggregate demand (NGDP) and real output (RGDP).

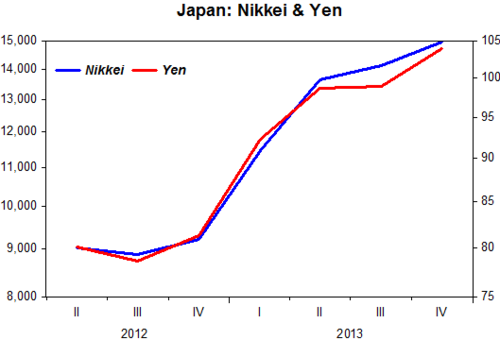

The next chart depicts what happened with the Nikkei stock index and the exchange rate (yen/USD).

The strong rise in the stock market is indicative of positive expectations about the effects of the plan. The depreciation of the yen is an important transmission mechanism of the expansionary monetary policy. In this case, the initial negative reaction of competitors, who accused Japan of engaging in ‘beggar-thy-neighbor’ policies, was misplaced. As the next chart shows, imports rose by more than exports, with Japan incurring a trade balance deficit.

This is indicative that the income effect of the expansionary policy was stronger than the terms of trade effect of the exchange devaluation. In other words, it reflects an increase in domestic demand.

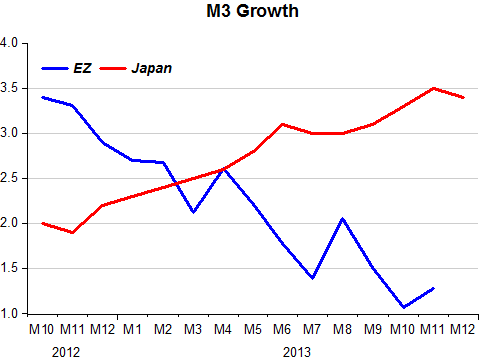

It is also interesting to compare Japan since ‘Abenomics’ with what´s happening in the Eurozone.

The chart shows the growth of broad money (M3). While in Japan, according to the plan, monetary policy is expansionary; in the Eurozone the BCE is tightening monetary policy.

It is, therefore, not surprising to observe the contrasting behavior of inflation in the two cases. While in Japan inflation is climbing towards the 2% target, in the EZ it is way below target and falling, with several countries in the group experiencing deflation.

The difference in the behavior of the BoJ and BCE is summarized in the chart below which shows the growth of real output in the two ‘countries’.

So it seems that ‘Abenomics’ is delivering on its promise. Hopefully it will continue to do so. We may also conclude that the EZ is travelling to “where Japan is coming from”!

Actually, There Was Some Real Policy in Obama’s Speech

I briefly considered titling this post “The 2014 State of the Union Hints at Shifts in the Overton Window.” I say a bit about the “Overton window" in my post "The Overton Window.” In brief, the “Overton window” is the set of “respectable" policies that are discussed by actual politicians and those closely associated with them.

Quartz #43—>That Baby Born in Bethlehem Should Inspire Society to Keep Redeeming Itself

Here is the full text of my 43d Quartz column, “That baby born in Bethlehem should inspire society to keep redeeming itself,” now brought home to supplysideliberal.com. It was first published on December 8, 2013. Links to all my other columns can be found here.

I followed up the main theme of this column with my post “The Importance of the Next Generation: Thomas Jefferson Grokked It.” I followed up the gay marriage theme with my column “The Case for Gay Marriage is Made in the Freedom of Religion.” I also have a draft column on abortion policy that is waiting for a news hook as an occasion to publish it.

If you want to mirror the content of this post on another site, that is possible for a limited time if you read the legal notice at this link and include both a link to the original Quartz column and the following copyright notice:

© December 8, 2013: Miles Kimball, as first published on Quartz. Used by permission according to a temporary nonexclusive license expiring June 30, 2015. All rights reserved.

Among its many other meanings, Christmas points to a central truth of human life: a baby can grow up to change the world. But it is not just that a baby can grow up to change the world; in the human sense, babies are the world: a hundred-odd years from now, all of humanity will be made up of current and future babies.

Babies begin life with the genetic heritage of humankind, then very soon take hold of, reconfigure, and carry on the cultural heritage of humanity. The significance of young human beings as a group is obscured in daily life by the evident power of old human beings. But for anyone who cares about the long run, it is a big mistake to forget that the young are the ultimate judges for the fate of any aspect of culture.

Since those who are now young are the ultimate judges for our culture, it won’t do to neglect instilling in them the kind of morality and ethics that can make them good judges. I have been grateful for the lessons in morality and ethics that I had as a child in a religious context, and with my own children, I saw many of these lessons instilled effectively in short moral lessons at the end of Tae Kwon Do martial arts classes. I don’t see any reason why that kind of secularized moral lessons can’t be taught in our schools, along with practical skills and a deep understanding of academic subjects, especially if we do right by kids by giving them time to learn by lengthening the school day and year.

In at least two controversies, the collective judgments of the young seem on target to me. Robert Putnam of Bowling Alone fame came to the University of Michigan a few years ago to talk about the research behind his more recent book with David Campbell, American Grace: How Religion Divides and Unites Us. He expressed surprise that many young people are becoming alienated from traditional religion when attitudes toward abortion among the young are similar to attitudes among those who are older. But the alienation from traditional religion did not surprise me at all given another fact he reported: the young are dramatically more accepting and supportive of gay marriage than those who are older. I am glad that the young are troubled by the conflict between reproductive freedom and reverence for the beginnings of human life presented by abortion on the one hand and abortion restrictions on the other. But there is no such conflict in the case of gay marriage, which pits the rights of gay couples to make socially sanctioned commitments to one another and enjoy the dignity and practical benefits of a hallowed institution against ancient custom, theocratic impulses, and misfiring disgust instincts that most of the young rightly reject. In this, the young are (perhaps without knowing it) following the example of that baby born in Bethlehem, who always gave honor to those who had been pushed to the edges of the society in which he became a man.

The hot-button controversy of gay marriage is not the only area of our culture due for full-scale revision. Our nation and the world will soon become immensely richer, stronger, and wiser if young people around the world reject the idea I grew up with that intelligence is a fixed, inborn quantity. The truth that hard work adds enormously to intelligence can set them free. What will make an even bigger difference is if they also enshrine their youthful idealism in a vision of a better world that can not only motivate them when young, but also withstand the cares of middle-age to guide their efforts throughout their lives.

Knowing that those who are now young, or are as yet unborn, will soon hold the future of humanity in their hands should make us alarmed at the number of children who don’t have even the basics of life. By far, the worst cases are abroad. The simplest way to help is to stop exerting such great efforts to put obstacles in the way of a better life for them. But whether or not we are willing to do that, it is a good thing to donate to charities that help those in greatest need. Also, I give great honor to those economists working hard trying to figure out how to make poor countries rich.

For those of us already in the second halves of our lives, the fact that the young will soon replace us gives rise to an important strategic principle: however hard it may seem to change misguided institutions and policies, all it takes to succeed in such an effort is to durably convince the young that there is a better way. Max Planck, the father of quantum mechanics, said “Science progresses funeral by funeral.” In a direction not quite as likely to be positive, society evolves from funeral to funeral as well—the funerals of those whose viewpoints do not persuade the young.

It is a very common foolishness to look down on children as unimportant. The deep end of common sense is to respect children and to bring to bear our best efforts, both intellectually and materially, to help them become the best representatives of our species that the universe has ever seen.

David Beckworth: "Miles and Scott's Excellent Adventure"

Link to the post on David Beckworth’s blog

David Beckworth was kind enough to give me permission to mirror this post as a guest post on this blog. Here it is:

A journalist recently reminded me of how important the blogosphere has become for shaping conversations on macroeconomic policy. Everything from TARP to shadow banking to quantitative easing have been vetted in the blogosphere over the past few years. Often these conversations have influenced policymaking. Paul Krugman recently commented on this development:

[T]here has been a major erosion of the old norms. It used to be the case that to have a role in the economics discourse you had to have formal credentials and a position of authority; you had to be a tenured professor at a top school publishing in top journals, or a senior government official. Today the ongoing discourse, especially in macroeconomics, is much more free-form…at this point the real discussion in macro, and to a lesser extent in other fields, is taking place in the econoblogosphere…

Alex Tabarrok made a similar point at an AEA meeting when he said the blogosphere has become the “first place for policy debate and policy development.” There are many examples of this, but here I want to recognize two potential solutions to the zero lower bound (ZLB) problem that got a wide hearing because of the blogosphere. These solutions were not new, but because of blogging and the personalities behind them, they became more widely understood and influenced policy.

The two solutions are implementing negative policy interest rates via electronic money and nominal GDP level targeting (NGDPLT). Miles Kimball pushed the former while Scott Sumner was behind the latter. Both individuals first pushed these ideas in the blogosphere. Miles Kimball’s idea spread rapidly from his blog to other media outlets to central banks where he made multiple presentations to monetary authorities. Arguably, the Fed and ECB officials began talking more seriously about negative interest rates because of his efforts. Scott Sumner’s relentless efforts for NGDPLT also began on his blog and are considered by many to be the reason the Fed finally did QE3, a large scale-asset purchasing program tied to the state of the economy. Miles and Scott’s success is a testament to their hard work, but also to disruptive technology that is the blogosphere.

I bring up their contributions, because they provide a nice conclusion to my previous two posts that looked at the ZLB. In those posts I looked at the claim that slump has persisted for so long because the nominal short-term natural interest rate has been negative while the actual short-term interest rate has been stuck near zero. It is stuck near zero because individuals would rather hold paper currency at zero percent than to invest their money at a negative interest rate. The ZLB is preventing short-term interest rates from reaching their output-market clearing level. The long slump is the result. Miles and Scott both have a solution for this problem. Unsurprisingly, both view the ZLB as a self-imposed constraint that can be easily fixed.

There are two key parts to Miles Kimball’s solution. The first part is to make electronic money or deposits the sole unit of account. Everything else would be priced in terms of electronic dollars, including paper dollars. The second part is that the fixed exchange rate that now exists between deposits and paper dollars would become variable. This crawling peg between deposits and paper currency would be based on the state of the economy. When the economy was in a slump and the central bank needed to set negative interest rates to restore full employment, the peg would adjust so that paper currency would lose value relative to electronic money. This would prevent folks from rushing to paper currency as interest rates turned negative. Once the economy started improving, the crawling peg would start adjusting toward parity. More details on his proposal can be found here.

There is much to like about his proposal. It is effectively how a free-banking, profit maximizing system would solve the ZLB, as shown by JP Koning. Holding risk constant, it would move all interest rates down and maintain spreads so that financial intermediation would not be disrupted. It would also eliminate the illusion that liquid short-term debt contracts are risk-free. Most importantly, it would allow short-tern nominal interest rates to better track their natural interest rate level. (1)

The figure below shows how how Miles Kimball’s solution would provide an escape route from the ZLB problem. It shows a situation where there is a negative output gap and anegative short-turn nominal natural interest rate. Miles would have the Fed would lower its policy interest rate down to the natural interest level at time t. The output gap would start to close and consequently, the natural interest rate would start to rise. The Fed would follow suit and start raising its policy interest rate in line with the natural rate. Eventually, the economy would return to full employment and the nominal interest rates would settle at their long-run values (which typically are positive). The escape from the ZLB would be complete. (2)

Scott Sumner’s solution to the ZLB provides another escape route from the ZLB. His approach is to “shock and awe” the economy with a regime change to monetary policy that would catalyze a sharp recovery. This recovery would pull the natural interest rate back into positive territory and eliminate the ZLB problem. Scott would implement his “shock and awe” program by having the Fed announce a NGDPLT (or total dollar spending target) and credibly committing to do whatever it takes to make it happen.

This amounts to the Fed committing to a permanent expansion of the monetary base, if needed. That is, a NGDPLT creates the expectation that if the market itself does not self correct through a higher velocity of base money, then the Fed will raise theamount of monetary base as needed to hit higher level of NGDP. If credible, this becomes a self-fulfilling expectation with the market itself doing most of the heavy lifting. In other words, the regime changewould spark a major portfolio rebalancing away away from highly liquid, low-yielding assets towards less liquid, higher yielding assets. The portfolio rebalancing would raise asset prices, lower risk premiums, increase financial intermediation, spur more investment spending, and ultimately catalyze a robust recovery in aggregate demand. It would be similar in spirit to what monetary policy portion of Abenomics is now doing in Japan.

The figure below shows how Scott’s solution would provide an escape route from the ZLB. Like before, the figure shows a negative output gap and short-run nominal natural interest rate that is negative. At time t, Scott would have the Fed introduce NGDPLT. The output gap would begin shrinking and put upward pressure on the natural interest rate. Eventually the natural interest rate would broach zero and the Fed would have to start raising its policy rate in line with it. Finally the economy would return to full employment and the natural interest rate to its long-run positive value. The escape from the ZLB would be complete.

So these are the two solutions to the ZLB problem. They have received a wide hearing and to some extent influenced policymaking because of Miles and Scott’s efforts in the blogosphere. Thanks to this disruptive technology and the conversations it started the world is a better place.

1. Bill Woolsey has a similar proposal. He wouldtransfer paper currency production to private banks and allow them to determine whether they want to produce paper money. Private banks would then determine the exchange rate between deposits and paper currency.

2. To be clear, Scott Sumner would do away with interest rate targeting altogether and his push for NGDPLT is more than about escaping the ZLB. It is about setting up a credible and effective target for monetary policy. I too am a big proponent of NGDPLT for this reason.

Quartz #42—>Make No Mistake about the Taper—The Fed Wishes It Could Stimulate the Economy More

Here is the full text of my 40th Quartz column, “Make no mistake about the taper—the Fed wishes it could stimulate the economy more,” now brought home to supplysideliberal.com. It was first published on December 19, 2013. Links to all my other columns can be found here.

If you want to mirror the content of this post on another site, that is possible for a limited time if you read the legal notice at this link and include both a link to the original Quartz column and the following copyright notice:

© December 19, 2013: Miles Kimball, as first published on Quartz. Used by permission according to a temporary nonexclusive license expiring June 30, 2015. All rights reserved.

The US Federal Reserve announced yesterday that it would reduce the rate at which it would buy long-term government bonds and mortgage bonds—the long-awaited taper of quantitative easing. But the financial markets have the last word on which way monetary policy has shifted. And as Tyler Durden complained at zerohedge.com, the rise in stock prices and gold prices, and fall in long-term interest rates and the dollar, indicated that the Fed had moved in the direction of monetary stimulus. The reason is that in the financial markets, the reaction to Fed action is always an expectations game. The Fed announced a smaller cut in bond-buying than the financial markets expected, so the markets treated the Fed decision as a move in the direction of stimulus.

Yet the Fed, while tapering more gradually than expected, indicated that it wished it could stimulate the economy more. The majority decision said that as far as the labor market (and the closely related level of economic activity) is concerned, risks had “become more nearly balanced” but that “inflation persistently below its 2 percent objective could pose risks to economic performance.” Since the Fed cares about both the labor market and inflation, the means that overall the Fed thinks there is too little monetary stimulus. And the one dissenter, Boston Fed president Eric Rosengren, said that “with the unemployment rate still elevated and the inflation rate well below the target, changes in the purchase program are premature until incoming data more clearly indicate that economic growth is likely to be sustained above its potential rate.”

What is going on? Though the official statement doesn’t say so explicitly, the discussion of the Fed’s interest rate target makes it clear that if the current labor market and inflation situation were coupled with a federal funds rate of, say 2%, then the Fed would cut interest rates, which would provide a substantially bigger monetary stimulus than moderating the expected taper a bit. So the reason the Fed isn’t stimulating the economy more is not that it thinks the economy is in danger of overheating, but because it doesn’t like the tools it has to use when interest rates are already basically zero. Ben Bernanke said as much when he came to the University of Michigan back in January. Even the Fed doesn’t like QE or making the quasi-promises about future interest rates that go under the name of ‘forward guidance.” So it doesn’t stimulate the economy as much as it thinks the economy needs to be stimulated.

The solution to the dilemma of a Fed doing less than it thinks should be done because it is afraid of the tools it has left when short-term interest rates are zero? Give the Fed more tools. Unfortunately, it takes time to craft new tools for the Fed, but that is all the more reason to get started. (Sadly, even if all goes well in the next few years, this isn’t the last economic crisis we will ever have.) As I have written about here, here, and here, three careful and deliberate steps by the US government would make it possible for the Fed to cut interest rates as far below zero as necessary to keep the economy on course:

- facilitate the development of new and better means of electronic payment and enhance the legal status of electronic money,

- trim back the legal status of paper currency, and

- give the Federal Reserve the authority to charge banks for storing money at the Fed and for depositing paper currency with the Fed.

If the Fed could cut interest rates below zero, it wouldn’t need QE, it wouldn’t need forward guidance, and it wouldn’t wind up begging Congress and the president to run budget deficits to stimulate the economy. And because the Fed understands interest rates—whether positive or negative—much, much better than it understands either QE or forward guidance, the Fed would finally know what it was doing again.

Christian Kimball on the Fallibility of Mormon Leaders and on Gay Marriage

My big brother Chris gave me permission to post a (lightly edited) email discussion giving his reaction to my post “Flexible Dogmatism: The Mormon Position on Infallibility” that he sent in an email. You will have to read that post first to understand what he is talking about on that. What is of equal interest is what Chris had to say about gay marriage, later on in our exchange.

Chris: I think you are hypercritical in your post “Flexible Dogmatism: The Mormon Position on Infallibility." Understandable (a common reaction of one who has felt oppressed by the "follow the prophet” meme) but unnecessary.

First, the strong form of “infallibility” (not counting backroom conversations in Seminary and Sunday School) is not “we are right” but “we will not lead you astray”. Logically quite different and the difference matters–one is a truth statement, the other a safety or comfort statement.

Second, your statement that “According to these principles, the Mormon Church can renounce past policies and can renounce past theologies, but it cannot renounce the rightness of past policies at the time they were in effect. “ may be literally correct as qualified by “According to these principles” but I think it is simply wrong as a statement of theology, doctrine, or Church practice. To give credit, the “at the time” theory is frequently used in regard to 19th century polygamy, but I view that as a special (and specially troubled) case from which I would be slow to generalize. (Not that I agree with the theory even in that application.)

Third, the “Race and the Priesthood” statement does say to me “Brigham Young was wrong”. (Notably, it is not a first for Brother Brigham, who said a number of things that have been disavowed.) Extracting from the statement:

In 1852, President Brigham Young publicly announced that men of black African descent … Over time, Church leaders and members advanced many theories to explain … None of these explanations is accepted today …”

Recognizing that for all of the rationalization and reasons-behind-the-reason theories, the preeminent explanation was always “so says the prophet”, this adds up to Brigham was wrong. That doesn’t mean that people who want to rationalize around to a flexible dogmatism can’t find a way to do it. But such rationalizations will always be with us, and nothing anybody can say will end it.

Fourth, your closing reference to the Hopak/Cossack dance/Ukrainian dance doesn’t work literally (the LDS primary music is more like the Hava Nagila if I were looking for a non-Mormon reference, and the music I associate with the Cossack dance is various but more reminds me of what I’d hear in square dance or folk dance, or a circus) and therefore the reference comes across as an expression of your own feeling of oppression that you make vivid by associating it with the old Soviet state (my reaction) or marionettes (perhaps your first meaning).

Miles: By the way, did you see my column on gay marriage, “The case for gay marriage is made in the freedom of religion”?

Chris: I did. I’m not persuaded that SSM is a matter of religious freedom. The Rawlsian move might be effective in a due process or equal treatment argument but doesn’t get me to religious freedom.

Now if you reversed grounds and argued that a man-woman-only rule is an establishment of religion, one that violates the 1st Amendment … I’d have more to think about. I don’t know the Establishment jurisprudence so I can’t judge the strength of the argument, but it sounds good, especially in Utah where the case can be made that the anti-SSM position is state religion.

BTW, opinion polls in Utah are showing a shift, where an anti-SSM amendment would very possibly fail a popular vote today–a reversal of the actual voting in 2004.

Miles: Very interesting. On my “Flexible Dogmatism” post, I added this note:

I am not making a narrowly legal argument in “The case for gay marriage is made in the freedom of religion.” It as addressed at least as much to current and future voters and legislators as to lawyers crafting arguments for judges.

Chris: It’s probably worth mentioning that my 1998 speech advocated marriage. I refer to it as the speech that made nobody happy: to the one-man-one-woman traditionalist I said “they should get married” and to the gay couple looking for permission but not necessarily obligation I said “you should get married”. There are plenty of churches and religious leaders (now there are, anyway) who are willing and happy to celebrate a same-sex marriage. But I haven’t yet seen a church or religious leader take the completely logical and in my mind necessary step of layering a moral imperative on same-sex marriage. Until that happens, it will be hard to see an affirmative freedom of religion argument for SSM.

I also made a set of questions as if for a law school class on the Mormon Church’s “Proclamation on the Family,” which sets out the Church’s position on gay marriage.

Paul Krugman: Microfoundations and the Parting of the Waters

I find myself mostly in agreement with Paul Krugman’s post “Microfoundations and the Parting of the Waters.” I recommend it.

Izabella Kaminska: The Time for Official E-Money is NOW!

Link to the post on FT Alphaville

A few months ago, Izabella Kaminska and I arranged to talk to each other on Skype and had a very interesting discussion. Izabella has written a wonderful column on the Financial Times’s blog Alphaville based on that discussion: “The time for official e-money is NOW!” I was delighted when Izabella told me it was fine to mirror that column in full here. In relation to what follows, let me say that my two-year timeline for a government to get all the legal wrinkles figured out for electronic money is for a government that is making a concerted bureaucratic effort. But I think it will not be too many years before some government does exactly that.

Now, more than ever, is the time for central banks to launch their own official e-money. We’ve campaigned for this before. But in light of further Bitcoin and altcoin developments, as well as secular stagnation observations by Larry Summers, it’s worth reiterating the argument for an unconventional policy of this sort.

First, it’s important to stress why this wouldn’t in any way be a panicked response to the supposedly destabilising “threat” of Bitcoin.

Central bankers, after all, have had an explicit interest in introducing e-money from the moment the global financial crisis began.

What’s more, the Bitcoin asset bubble is much more likely to be doing the stagnating dollar economy a favour at the moment than a disservice.

For one thing, it’s directing what would otherwise be de-stabilising flows into an entirely synthetic market rather than into real world goods and resources, like houses, art or commodities — in so doing stopping at least some actual consumable goods and resources from being bid up to prohibitively high levels for regular folk. Second, it’s expanding the overall money supply — useful in a disinflationary world which lacks compensatory bank lending. Third, it’s potentially improving the velocity of money. And fourth, it’s created a parallel currency that looks hugely overvalued relative to the dollar, by definition causing Gresham’s law type effects that end up rewarding the dollar with greater use, velocity and competitive advantage.

Most important of all, however, Bitcoin has helped to de-stigmatise the concept of a cashless society by generating the perception that digital cash can be as private and anonymous as good old fashioned banknotes. It’s also provided a useful test-run of a digital system that can now be adopted universally by almost any pre-existing value system.

This is important because, in the current economic climate, the introduction of a cashless society empowers central banks greatly. A cashless society, after all, not only makes things like negative interest rates possible, it transfers absolute control of the money supply to the central bank, mostly by turning it into a universal banker that competes directly with private banks for public deposits. All digital deposits become base money.

Consequently, anyone who believes Bitcoin is a threat to fiat currency misunderstands the economic context. Above all, they fail to understand that had central banks had the means to deploy e-money earlier on, the crisis could have been much more successfully dealt with.

Among the key factors that prevented them from doing so were very probable public hostility to any attempt to ban outright cash, the difficulty of implementing and explaining such a transition to the public, the inability to test-run the system before it was deployed.

Last and not least, they would have been concerned about displacing conventional banks from their traditional deposit-taking role, and in so doing inadvertently worsening the liquidity crisis and financial panic before improving it.

Given the disruptive consequences of such an irreversible move for the banking sector — effectively transforming banking into fund management — the central bank would not have been keen to deploy the strategy until it was sure that secular stagnation was really the result of the crisis and that the conventional banking model was beyond saving.

Almost of all of these prohibitive factors have, however, by now been overcome:

1) Digital currency now follows in the footsteps of a “disruptive” anti-establishment digital movement perceived to be highly accommodating to the black market and all those who would ordinarily have feared an outright cash ban. This makes it exponentially easier to roll out. Bitcoin has done the bulk of the educating.

2) What was once viewed as a potentially oppressive government conspiracy to rid the public of its privacy can be communicated as being progressive and innovative as a result.

3) Banks have been given more than five years to prove their economic worth and have failed to do so. If they haven’t done so by now, they probably never will, meaning there’s unlikely to be a huge economic penalty associated with undermining them on the deposit front or in transforming them slowly into fully-funded fund managers.

4) The open-ledger system which solves the digital double-spending problem has been robustly tested. Flaws, weaknesses and bugs have been understood, accounted for, and resolved.

All that is left is to develop an economically efficient deployment plan! Lucky for us Miles Kimball, professor of economics and survey research at the University of Michigan, has exactly such a plan.

We’ve reviewed Kimball’s dual framework plan before here and here.

Very loosely it involves a central bank centrally issuing e-money and allowing it to trade side by side with paper money for a period of time. Use of e-money could be incentivised by a favourable rate environment for e-money, or by an enticing exchange rate for swapping out of paper money for e-money. In that sense it would be similar to the parallel Rollad system envisioned by Willem Buiter in 2009. Its use could be further encouraged by a general campaign to stigmatise the use of paper cash.

We were originally unconvinced that a transitory dual framework period would be needed. We worried in fact that it might come across as too confusing. The success of Bitcoin, however, shows that the public is more than capable of understanding and adopting a parallel value system which provides it with an explicit interest rate or exchange rate advantage.

Kimball noted to us, however, that before any such system could be deployed the legal status of electronic money would have to be defined by government. But he is optimistic that all the preparations could be completed within two years or so.

And there’s no reason at all why a central e-money system couldn’t replicate many components of the Bitcoin open-ledger system in a way that ensures a similar level of privacy, as well as equally competitive transaction costs (or lower) because the computational costs end up being borne by the central bank directly rather than by miners.

Once everyone was captured by the system, it would then be possible to manage the exchange or interest rates on e-money (relative to cash) in such a way that an implicit negative rate was achieved.

Kimball is confident that it’s a question of when rather than if the system is deployed. He also believes if the US government doesn’t act first some other central bank will instead.

What it would effectively mean is that everyone would via the process be able to bank directly with the central bank if they wished, and only invest in bank deposits if they were prepared to bear the associated risks in exchange for potentially greater payoffs.

If and when an official e-money currency of this sort was launched it’s fair to state it would probably prove a major competitor of Bitcoin or other altcoin systems, offering as it does price stability, trust, liquidity, ubiquity, reputation, mutual interest, a government guarantee system, not to mention protection from overbearing wealth concentration or debasement. All features that happen to depend on the presence of a central planner, who acts in the interests of the people because it is accountable to them.

That’s not to say the incentive to hold or use alternative currencies would be eliminated entirely. It would, however, be linked entirely to those coins’ speculative value rather than their superior functionality, and in that sense be influenced as much by central bank interest rates policy as any other speculative asset class is currently influenced today.

Though, of course, the greater the negative interest rate, the greater the incentive to hold alternative coins. The greater the incentive to hold alternative coins ,the greater the incentive to produce them. The greater the incentive to produce them, the greater the chances of oversupply and collapse. The more sizeable the collapse, the more desirable the managed official e-money system ultimately becomes in comparison.

Either way, the key point with official e-money is that the hoarding incentives which would be generated by a negative interest rate policy can in this way be directed to private asset markets (which are not state guaranteed, and thus not safe for investors) rather than to state-guaranteed banknotes, which are guaranteed and preferable to anything negative yielding or risky (in a way that undermines the stimulative effects of negative interest rate policy).

Related links

- Negative interest in cash, or goodbye banknotes - FT Alphaville

- A digital solution for the repo squeeze? – FT Alphaville

- The ‘high-powered money’ problem - FT Alphaville

- Guest post: The case for digital legal tender – FT Alphaville

Tom Grey’s Excellent Electronic Money Rap

When I followed up “Gather ’round, Children, Here’s How to Heal a Wounded Economy” with a lame rap video version of the storybook, I begged for someone to try their hand at a real rap version. Tom Grey stepped up to the plate and hit a home run. He totally rewrote the words of the story to make it work as a rap, but kept the same essential meaning. Donna D'Souza put the new text together with the pictures and the Tom Grey’s audio track to make the YouTube video.

The video is the spoken rap version without music. A version with music is coming. If you want to print out the storybook with the rap text, here it is.

I am not proud of my own rap version, but I think my read-aloud version and my operatic ballad version of the story on YouTube are fine.

Many, many thanks to Tom. A wonderful New Year’s present!

The Institute for Social Research Summarizes the Argument for Electronic Money

Diane Swanbrow, Susan Rosegrant and Eva Menezes put together the newsletter for the Institute for Social Research at the University of Michigan. They put together a nice summary of my interview with Dylan Matthews of the Washington post “Can we get rid of inflation and recessions forever? (My direct answer to that question is in my companion post.) Here is the summary:

How would you feel if you put $1 into the bank, and when you took it out a year later, it was only worth 95 cents? Probably like it’s not a good time to be saving money. And that’s exactly why ISR researcher Miles Kimball argues that negative interest rates should be one tool available for economic policymakers. In a Nov. 18 Q&A in The Washington Post, Kimball acknowledged that high interest rates often are appropriate, encouraging people and businesses to save. But when economies are in recession, companies become reluctant to borrow or invest and people shy away from buying automobiles and houses, exactly the kinds of activities needed to jump start the economy. Allowing negative interest rates could help spark those activities and more quickly return the economy to health. Moreover, Kimball contends that if governments did most transactions electronically, it would be easier to manage negative interest rates. “Anything you can do to firm up the legal status of electronic money as the real thing makes it easier to do what it takes to go to negative interest rates,” Kimball said.

Bret Stephens and Paul Krugman: What Should a Correction Look Like in the Digital Era?

In my presentation “On the Future of the Economics Blogosphere” I talk about how the websites of newspapers and magazines that began as creatures of print often do things on their websites that are not best practice for online journalism. Underusing links is one example. Another related example is the way corrections are handled. Bret Stephens’s misuse of nominal income statistics in his piece “Obama’s Envy Problem” and the manner of the correction he made provide a good case study.

To help you get up to speed, let me say that this post is a followup to my posts

- The Wall Street Journal’s Quality-Control Failure: Bret Stephens’s Misleading Use of Nominal Income in His Editorial “Obama’s Envy Problem”

- Bret Stephens Issues a Correction: “About Those Income Inequality Statistics”

One reason I thought a followup would be worthwhile is that my post “The Wall Street Journal’s Quality-Control Failure: Bret Stephens’s Misleading Use of Nominal Income in His Editorial ‘Obama’s Envy Problem’” is at this moment my 3d most popular blog post ever.

In his January 8, 2014 post “Do Publications Have Any Responsibility to Screen Their Editorials? (Part 2)” R. Davis wondered why the original Bret Stephens article as it appears on the Wall Street Journal’s website has no link to Bret Stephens’s correction piece, and indeed no indication of any problem. Paul Krugman took Bret Stephens to task for the same thing in his post “The Undeserving Rich,” writing:

Oh, and for the record, at the time of writing this elementary error had not been corrected on The Journal’s website.

As this sentence stands, it is false, because it says “website” rather than “the version of the original article appearing on the website.” In addition to his correction on January 3, 2014, “About Those Income Inequality Statistics: An answer to Paul Krugman” on the Wall Street Journal's website, there was a formal January 5, 2014 acknowledgement in “Corrections & Amplifications.”

In his followup "Department of Corrections, and Not,“ Paul Krugman gives more precision, saying what counts in his book as a correction:

… you fix the error in the online version of the article, including an acknowledgement of the error; and you put another acknowledgement of the error in a prominent place, so that those who read it the first time are alerted. In the case of Times columnists, this means an embarrassing but necessary statement at the end of your next column.

I fully agree with Paul Krugman about how a correction should be done in the digital era. Arguably, "About Those Income Inequality Statistics: An answer to Paul Krugman,” counts as “the next column,” so Bret seems to have done that. And the Wall Street Journal did what would have been adequate in the paper era in "Corrections & Amplifications.“But in the digital era, that is inadequate. Whenever a correction of a serious error is made, it needs to be either made directly on the web version of the original article or addressed with a clearly signaled link. The Wall Street Journal neglected to do this. To the extent that this is based on a standard practice of the Wall Street Journal, that is the more inadequate, since it will affect many articles.

In his article "Stephens: Krugman and the Ayatollahs” Bret expresses some pique at Paul’s accusation that the article had not been corrected on the website. He never focuses on the fact that the original article as presented on the website has no clue of the correction, emphasizing his correction on January 3, 2014, “About Those Income Inequality Statistics: An answer to Paul Krugman,” and the formal January 5, 2014 acknowledgement in “Corrections & Amplifications.” Bret should be agitating strongly for a correction to appear on the online version of his original article as well. I look forward to seeing that correction appearing on the website version of the original article–especially if it betokens a general change in the Wall Street Journal's standard procedures for representing corrections on its website.

By the way, according to the principle I am enunciating here, and under the circumstances of a dispute like this, I would urge Paul to make sure that the online version of his column "The Undeserving Rich“ gets a link added to ”Department of Corrections, and Not,“ which provides the necessary clarification for the on-its-face inaccurate statement in ”The Undeserving Rich“ that the Wall Street Journal website had no correction for the error in Bret’s original article.

One final note: I am perfectly comfortable with silent edits of posts if errors are caught before they have become the basis for other people’s posts. I discuss my own policy in that regard in my post "It Isn’t Easy to Figure Out How the World Works” (Larry Summers, 1984)“:

… I routinely allow myself silent edits in my blog posts without an update notification. I am not running for office, I am not on trial, and I already have tenure, so I don’t have to play the game of “gotcha.” In my case, it is my words that matter, not me, and the words that matter are the ones I am willing to stand behind in the end.

One should, of course, forthrightly admit that an error was made previously if anyone asks, but as long as an error is corrected, I see no duty to advertise that previous error. The number one duty is to get things right for the readers. Beyond that, it is a simple matter of honesty about previous errors should the issue come up.

It is only when errors become the basis of other people’s posts or other writings that one needs to clearly signal errors, since knowledge of the error is required for readers to understand what the discussion is all about. Errors that are the basis of comments on the original post are a gray area. If the value of the relevant part of the comment is just to point out the error, then correction of the error respects the point of that comment. On the other hand, if the comment has something brilliant to say that is stimulated by the error, then it would be good form to somehow preserve the record of the error in order to avoid destroying the record of the stimulus for that comment. But the record of the error need not be in the original location; after all, there are other objectives served by having a casual reader able to read something correct straightaway without necessarily going through the whole convoluted path.

Josh Barro: We Need a New Supply Side Economics—Here Are 8 Things We Can Do

Noah Smith and Christopher Cordeiro tweeted that Josh Barro’s column “We Need A New Supply Side Economics — Here Are 8 Things We Can Do” sounded like ideas I would favor. They are right.

I fully agree with Josh’s lead-in:

Demand stimulation remains the right goal today, but it’s not going to be the right goal forever. …

We’re going to need a new supply side economics that encourages people to work, invest and innovate.

Some of Josh’s proposals cost money, for which he proposes more progressive income taxes as a revenue source (as his 8th point). I have proposed tapping the resources of the rich in a different way. I want to finance an expansion of the nonprofit sector (see the links in “The Red Banker on Supply-Side Liberalism”). To get there politically, I enunciated the principle of “No Tax Increase Without Recompense.” So I cannot go along with Josh’s proposal raise income taxes at the upper end in a conventional way. (Also see the Twitter discussions “Daniel Altman and Miles Kimball: Should We Expand Government or Expand the Nonprofit Sector?” and “Daniel Altman and Miles Kimball: Is It OK to Let the Rich Be Rich As Long As We Take Care of the Poor?”) The expansion of the nonprofit sector that I propose will help the poor tremendously in many ways beyond the dimension Josh is focuses on.

More generally, I think it is better to build progressivity into the spending side of the government’s activities–including transfers–than into the tax side. Instead, I think Josh’s proposed enhancements of programs to direct more resources toward the poor can also serve as ways to compensate the poor for increases in increases in taxes on externalities such as carbon dioxide emissions and the consumption of soft drinks and junk food that affect the behavior of all those around us through not-fully-conscious social influences.

Here is Josh’s list, minus the income tax increase, with my comments:

1. Invest in smart infrastructure, ideally without building much.

Yes! Noah and I have an column on infrastructure investment. And I agree with Josh that it is a bad habit to get into to think of infrastructure investment as a demand-side thing. We need to keep in our sights getting supply-side benefits from the infrastructure investments that we make.

I would emphasize government support for basic research in the same breath as infrastructure investment. Indeed, I think there is even more supply-side benefit to be had from government support for basic research than from additional infrastructure investment.

2. Reform means-tested entitlements without soaking the poor.

Josh wants to phase out aid to the poor more slowly with higher income, in order to avoid discouraging people from working hard and avoid discouraging people from building their careers through education and other means. This is great, but it will cost the government more money. I would like to reward healthy eating and not contributing too much to global warming across the whole population, as well as rewarding the poor for working hard and getting an education. That combination can finance itself.

3. Move the deregulatory agenda down to the state and local level.

This is one of Josh’s points that I think needs to be shouted from the rooftops. Here is the full text of what he said on this point:

In the 1970s, the big deregulation fights were properly at the federal level. Then the government deregulated airlines and trucking. Though technological change, regulation has become less important in broadcasting and telecommunications. Bank deregulation has been a mixed bag over this period; people talk about it as a cautionary tale, but some of the deregulations (such as ending the limit on savings account interest and allowing interstate banking) have served consumers very well.

The big federal regulatory fights that remain are in mostly areas where the federal government properly uses a heavy hand: banking and securities, and environmental protection.

The next round of big deregulation fights should be at the state and local level. Governments impose pro-incumbent regulations on a variety of industries from barbering to interior design to medicine to restaurants. These rules raise incomes for existing practitioners, but they make it difficult for new practitioners to enter the fields, and they raise consumer prices.

State and local governments should stop doing this.

In the interest of promoting interstate commerce, the federal government should pre-empt many of these regulations. For example, states should be forced to allow a broad scope of practice for nurse practitioners so they can serve as independent primary care providers. This would reduce doctors’ incomes, but it would reduce the cost of health care, raise patients’ real incomes and help to control government expenditure.

What I have said on this topic can be found in my post

4. Deregulate America’s most overregulated industry: real estate.

Here, Josh is on the same side as Matthew Yglesias, who wrote the book on this issue: The Rent is Too Damn High. I am part of the cheering section for their efforts. Given the fraction of household budgets spent on housing, this is a huge issue.

5. Reform intellectual property — by weakening it.

I endorse this idea in my link post “The Wonderful, Now Suppressed, Republican Study Committee Brief on Copyright Law.” I also muse on how much protection is necessary in my post “Copyright.” Wonderful, amazing new things will happen if we shift to less restrictive intellectual property rules. And if we overshoot in a way that undercompensates creators, that can easily be fixed later. It is high time we experimented with more fluid rules.

Given the pace of innovation and the rate at which things become obsolete, one change that almost certainly a winner is to shorten the term for patents and copyrights. The only place this seems problematic is in retaining adequate incentives for the development of new drugs. There, combining a shorter period of exclusivity with the government paying for half of the cost of drug trials would probably keep just as much innovation while still helping the government budget, since the government pays for drugs as part of Medicare now.

6. Improve education, somehow.

I have written a fair amount about education. Improving education will be an ongoing theme for me. Here is a link to my sub-blog on education, and here are some of the most important posts:

- Magic Ingredient 1: More K-12 School

- There’s One Key Difference Between Kids Who Excel at Math and Those Who Don’t (coauthored with Noah Smith)

- Visionary Grit

- The Unavoidability of Faith

- Two Types of Knowledge: Human Capital and Information

7. Admit more high-skill immigrants.

More open borders is something I am passionate about. But I would not limit it to high-skill immigrants. Helping the poor who are currently in other countries is also important. Here are some of my more important posts in that vein:

- The Hunger Games is Hardly Our Future: It’s Already Here

- Benjamin Franklin’s Strategy to Make the US a Superpower Worked Once, Why Not Try It Again?

- Obama Could Really Help the US Economy by Pushing for More Legal Immigration

- A Bare Bones Model of Immigration

- Immigration Tweet Day, February 4, 2013: Archive

- You Didn’t Build That: America Edition

Genius Can Only Breathe Freely in an Atmosphere of Freedom

Encouraging genius comes at a price: allowing nonconformity. John Stuart Mill makes that case eloquently in On Liberty chapter III, “Of Individuality, as One of the Elements of Well-Being,” paragraph 11:

Persons of genius, it is true, are, and are always likely to be, a small minority; but in order to have them, it is necessary to preserve the soil in which they grow. Genius can only breathe freely in an atmosphere of freedom. Persons of genius are, ex vi termini [from the force of the term], more individual than any other people—less capable, consequently, of fitting themselves, without hurtful compression, into any of the small number of moulds which society provides in order to save its members the trouble of forming their own character. If from timidity they consent to be forced into one of these moulds, and to let all that part of themselves which cannot expand under the pressure remain unexpanded, society will be little the better for their genius.

Shall we try to fit ourselves into boxes?

Radagast the Brown: Modeling the Climate of Middle Earth

Link to the full article in Dwarvish (screen shot below)

Hat tip to John Aziz for his retweet on this one.

Quartz #41—>Gather ’round, Children, Here’s How to Heal a Wounded Economy

Here is the full text of my 41st Quartz column, “Gather ’round, children, here’s how to heal a wounded economy,” now brought home to supplysideliberal.com. It was first published on December 17, 2013. Links to all my other columns can be found here.

I did several followup posts to this column, including 4 YouTube videos:

- Dylan Matthews: The Only Kid’s Book You Need to Understand the Federal Reserve

- The Story of Ben the Money Master (YouTube video of Miles reading the story aloud)

- The Story of Ben the Money Master—Operatic Ballad Version (YouTube video of Miles singing the story as an operatic ballad)

- The Story of Ben the Money Master—A Bad Rap (YouTube video of Miles attempting, and failing at a rap version)

- Tom Grey’s Excellent Electronic Money Rap (YouTube video of Tom Grey’s wonderful rap text)

If you want to mirror the content of this post on another site, that is possible for a limited time if you read the legal notice at this link and include both a link to the original Quartz column and the following copyright notice:

© December 17, 2013: Miles Kimball, as first published on Quartz. Used by permission according to a temporary nonexclusive license expiring June 30, 2015. All rights reserved.

University of Missouri-Kansas City professor Stephanie Kelton threw down the gauntlet for everyone serious about influencing economic policy into the next generation when she put out her MMT Coloring Book as a downloadable stocking-stuffer (pdf). (MMT stands for “Modern Monetary Theory,” the name of Stephanie’s viewpoint.) In response, I tweeted:

…and sent out a plea for creative help with a macroeconomic coloring book laying out my views about monetary policy. Donna D’Souza answered my call and did a great job illustrating the story. The downloadable coloring book (pdf) and colored-in storybook (pdf) are our gift to you and your children and grandchildren during this season of lights. You can also read the colored-in storybook version just below, followed by an explanation of the economics behind the story.

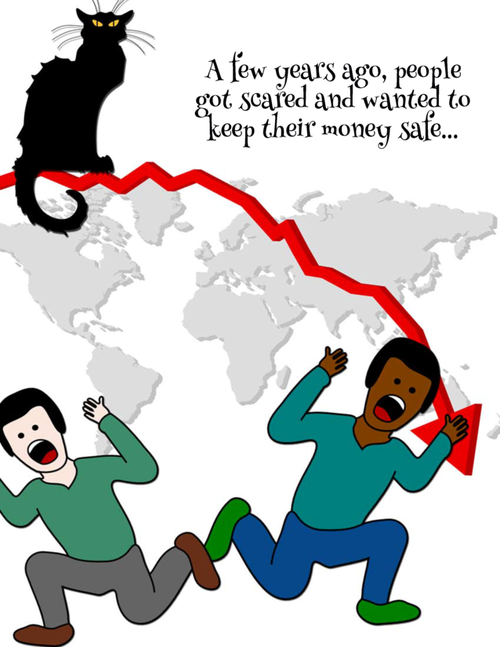

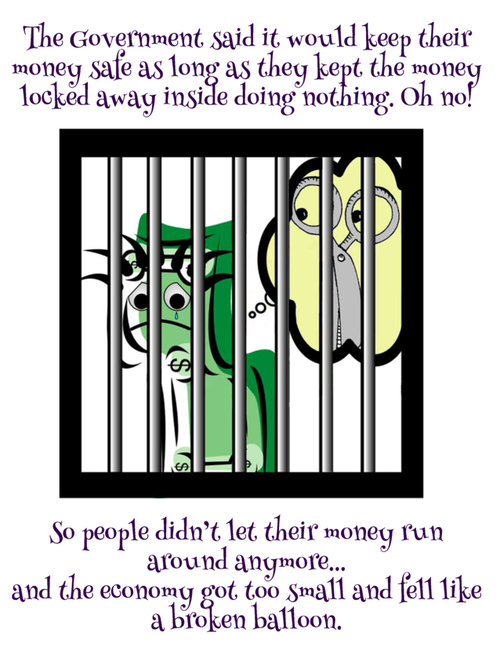

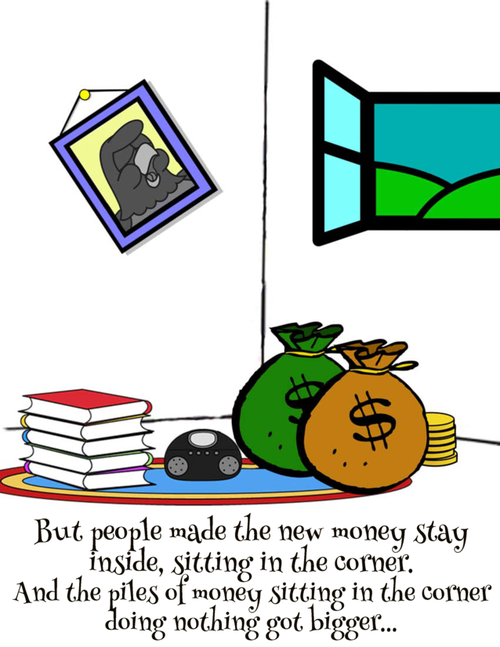

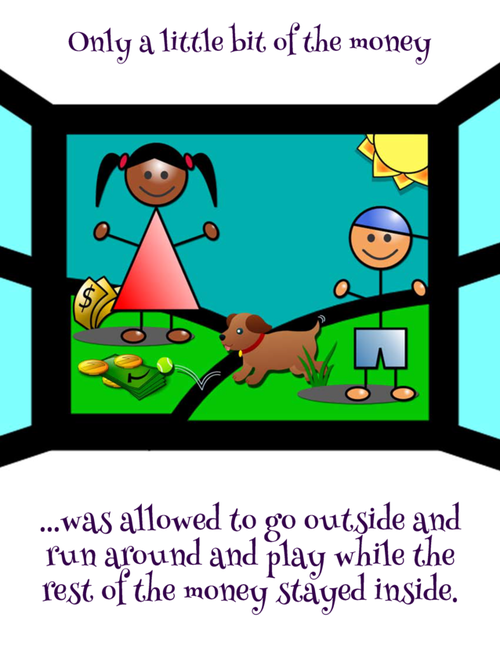

Milton the Maltese Falcon represents Milton Friedman, who was one of the greatest champions of monetary policy the world has known and one of the most effective economists ever at explaining economics to the public. Milton Friedman used an equation for the effects of monetary policy that emphasized two things: the quantity of money and the velocity of money. Money sitting in a bank vault or under a mattress has no velocity, and drags down the average velocity of money throughout the economy. It is only when money is being lent out and used (to build factories, buy equipment, build houses, buy cars) that it stimulates the economy.

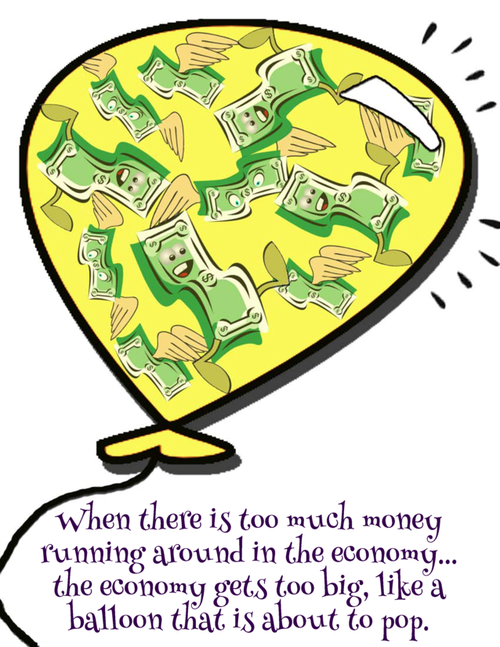

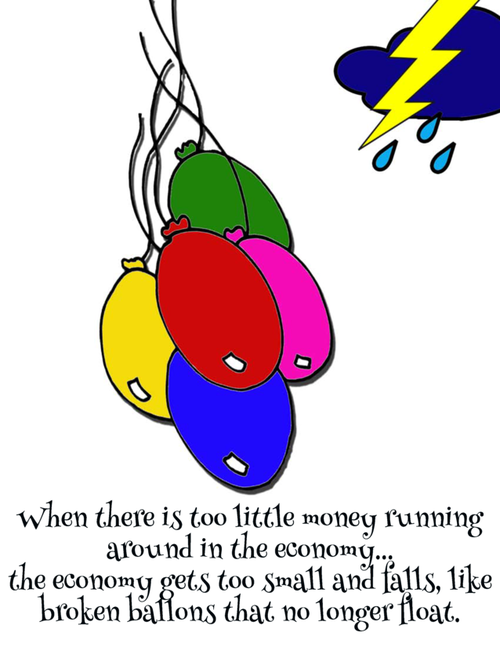

Of course, too much monetary stimulus is bad because it causes inflation (the balloon about to pop). But too little monetary stimulus is bad because it causes unemployment (the broken balloons). And how much stimulus a given amount of money provides depends a lot on whether it is at work in the economy (running around) or locked away in a bank vault, in a corporate treasury, or under a mattress, doing nothing.

The reason a lot of money has been lying around doing nothing is because the appropriate interest rate for the economy has been very low—below zero. If we had negative interest rates for a year or so, things would get back to normal. Without that tonic, bad times drag on and on.

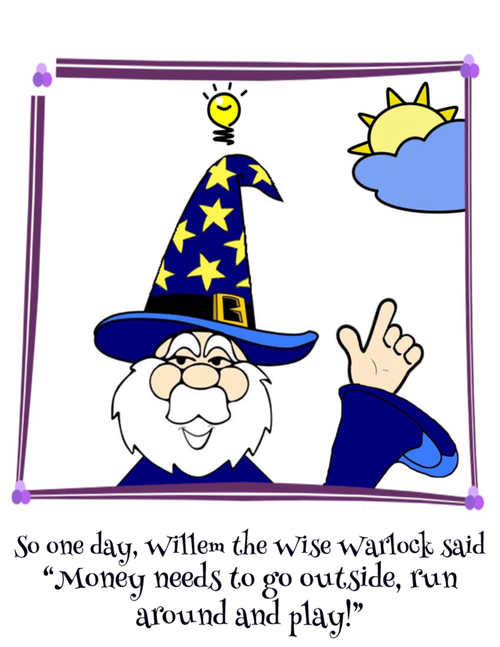

A key thing to understand is that the rest of the government is preventing the Federal Reserve (Ben the Money Master and his friends) from doing what it needs to do to heal the economy. Here is how: the government prevents interest rates from going below zero by the way it handles paper currency. As things are now, holding a pile of paper currency is a way for people to earn a zero interest rate without putting their money to work in the economy.

There is a solution, due in its modern form to Willem Buiter, now chief economist of CitiGroup, who appears in the story as “Willem the Wise Warlock.” Buiter discusses various options for repealing what economists call “the zero lower bound”: the economically damaging government guarantee that anyone can lend as much as they want to the government at a zero interest rate just by keeping a big pile of cash. I have elaborated on one of Willem Buiter’s ideas in Quartz, on my blog, and in presentations to central banks around the world, including the Federal Reserve Board.

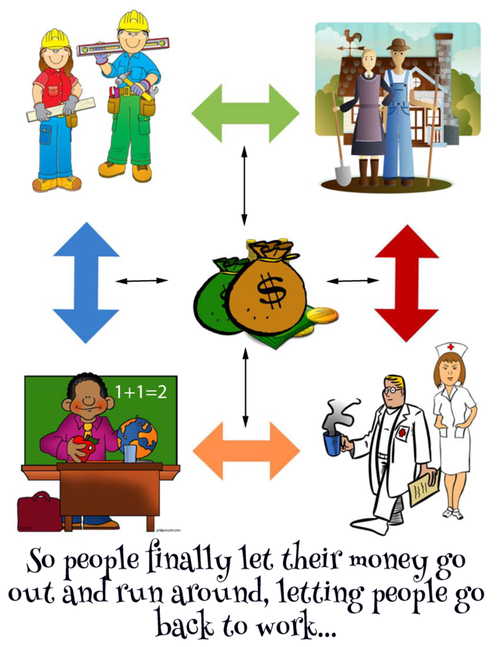

If we do what it takes to make money sitting around doing nothing shrink, it will provide a strong boost to the economy as people put money to work in the economy. Not everyone will like it, but it will quickly bring full economic recovery, without the bad side effects of other means of trying to stimulate the economy (such as budget deficits or encouraging financial bubbles). Once the economy recovers, everything can go back to what people are used to. Some economists talk about the possibility that negative interest rates might be needed for a long time, but I don’t buy it. In my view, negative interest rates should only be needed for a short time during serious economic slumps. If the Fed and other central banks are given that authority, recessions can be brief and people can get back to work again.

One of the most important reasons we need to keep the economy in good working order—in this case with appropriate monetary policy—is so that economics can recede a bit more into the background of people’s lives. Then people can concentrate again on the things that should matter most: nurturing relationships with friends and family, creating wild, wonderful varieties of meaning in their lives, and taking time to stand in awe of the universe.

We all know that the way to prevent the troubles that would be caused by shooting ourselves in the foot is to avoid shooting ourselves in the foot. Just so, our economic troubles have a straightforward cause and a straightforward technical solution. Both the cause of our troubles and the essence of the solution to our troubles are told in Milton the Maltese Falcon’s ballad.

On the Future of the Economics Blogosphere

On December 16, 2013, I gave a talk at the University of Michigan Library “On the Future of the Economics Blogosphere.” Here is the video of the talk.

Before watching the video, I recommend taking a look at the very high quality storify creation P. F. Anderson put together from the talk, including two sets of live tweets sent out during the talk. This was far, far from being a polished presentation, but there is a lot of substance to the talk, which you can see in P. F. Anderson’s storify piece.

The Powerpoint file is not so interesting all by itself; but here it is, if you want to refer to it.

You can see other talks in the series here.

Daniel Altman and Miles Kimball: Is It OK to Let the Rich Be Rich As Long As We Take Care of the Poor? →

The debate continues! This discussion is at just as high a level as yesterday’s.

Daniel Altman and Miles Kimball: Should We Expand Government or Expand the Nonprofit Sector? →

This was a very interesting Twitter discussion with Daniel Altman and others. I easily put it in my top 5 Twitter discussions during the 19 and a fraction months I have been blogging.

Several related links are collected in my post “The Red Banker on Supply-Side Liberalism.”

Free Kittens Through Dedigitization

Via murketing:

Arguably the ultimate in dedigitization.

And via procrastinaut:

This is a concept GIF showcasing how kittens will be free on the Internet one day.