Quartz #41—>Gather ’round, Children, Here’s How to Heal a Wounded Economy

Here is the full text of my 41st Quartz column, “Gather ’round, children, here’s how to heal a wounded economy,” now brought home to supplysideliberal.com. It was first published on December 17, 2013. Links to all my other columns can be found here.

I did several followup posts to this column, including 4 YouTube videos:

- Dylan Matthews: The Only Kid’s Book You Need to Understand the Federal Reserve

- The Story of Ben the Money Master (YouTube video of Miles reading the story aloud)

- The Story of Ben the Money Master—Operatic Ballad Version (YouTube video of Miles singing the story as an operatic ballad)

- The Story of Ben the Money Master—A Bad Rap (YouTube video of Miles attempting, and failing at a rap version)

- Tom Grey’s Excellent Electronic Money Rap (YouTube video of Tom Grey’s wonderful rap text)

If you want to mirror the content of this post on another site, that is possible for a limited time if you read the legal notice at this link and include both a link to the original Quartz column and the following copyright notice:

© December 17, 2013: Miles Kimball, as first published on Quartz. Used by permission according to a temporary nonexclusive license expiring June 30, 2015. All rights reserved.

University of Missouri-Kansas City professor Stephanie Kelton threw down the gauntlet for everyone serious about influencing economic policy into the next generation when she put out her MMT Coloring Book as a downloadable stocking-stuffer (pdf). (MMT stands for “Modern Monetary Theory,” the name of Stephanie’s viewpoint.) In response, I tweeted:

…and sent out a plea for creative help with a macroeconomic coloring book laying out my views about monetary policy. Donna D’Souza answered my call and did a great job illustrating the story. The downloadable coloring book (pdf) and colored-in storybook (pdf) are our gift to you and your children and grandchildren during this season of lights. You can also read the colored-in storybook version just below, followed by an explanation of the economics behind the story.

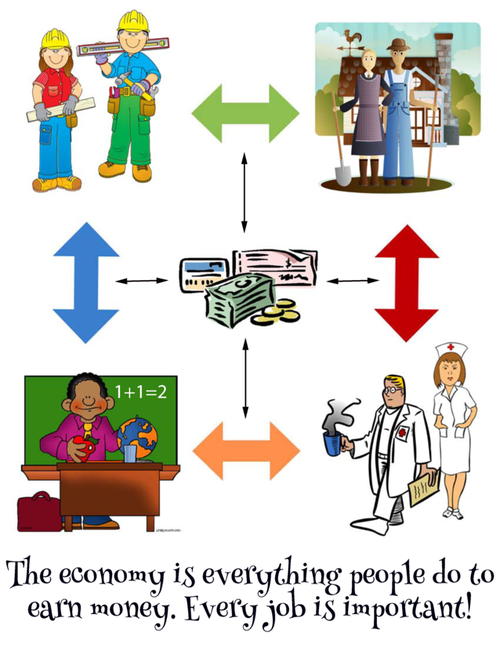

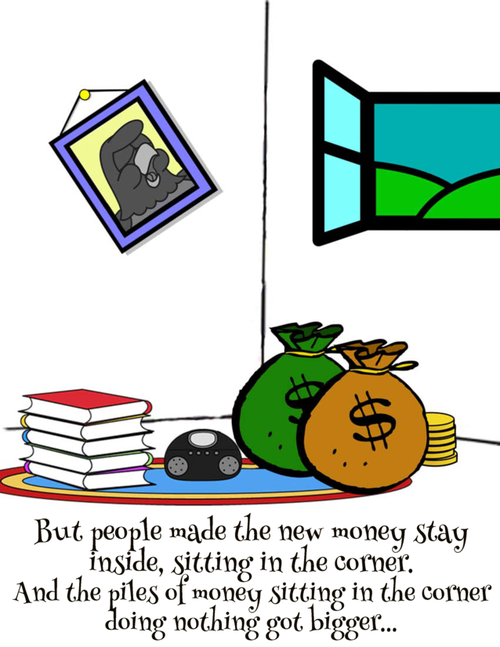

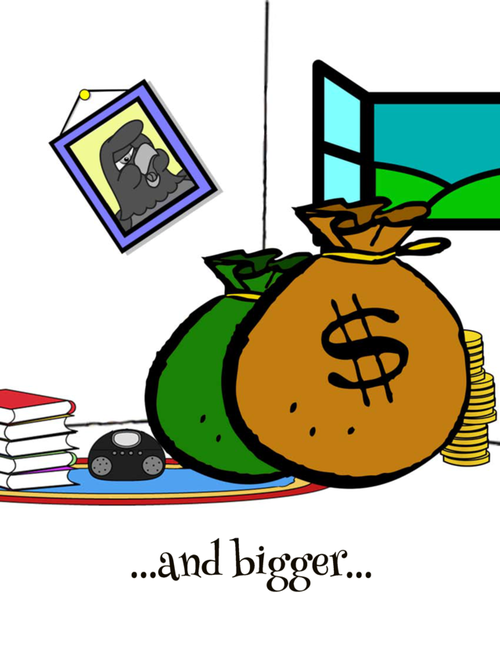

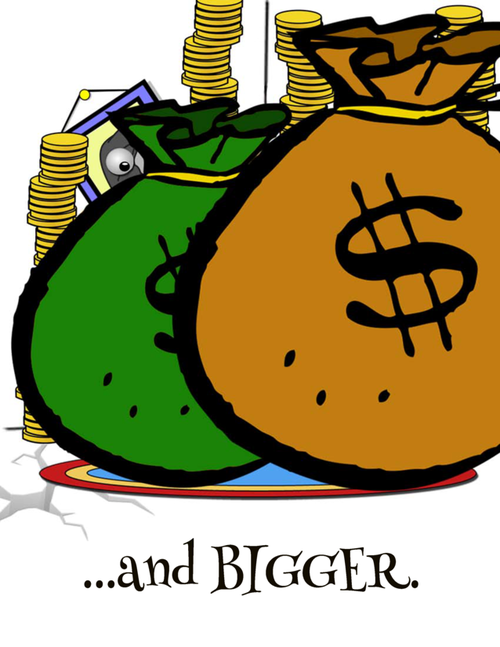

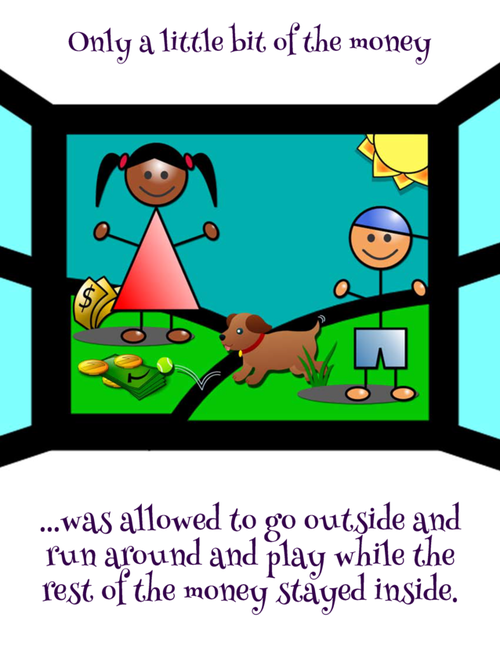

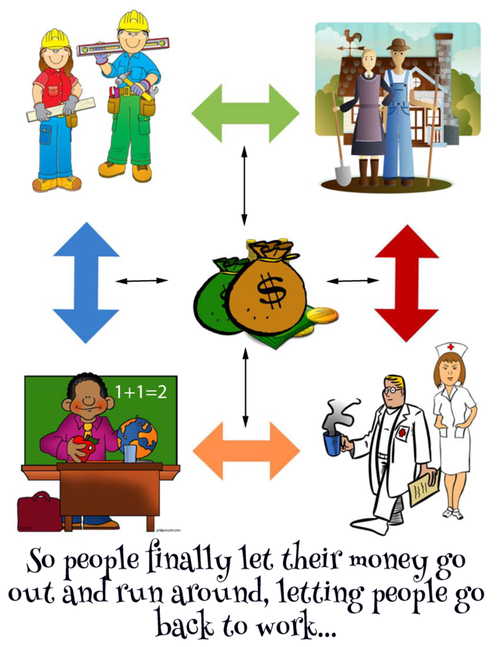

Milton the Maltese Falcon represents Milton Friedman, who was one of the greatest champions of monetary policy the world has known and one of the most effective economists ever at explaining economics to the public. Milton Friedman used an equation for the effects of monetary policy that emphasized two things: the quantity of money and the velocity of money. Money sitting in a bank vault or under a mattress has no velocity, and drags down the average velocity of money throughout the economy. It is only when money is being lent out and used (to build factories, buy equipment, build houses, buy cars) that it stimulates the economy.

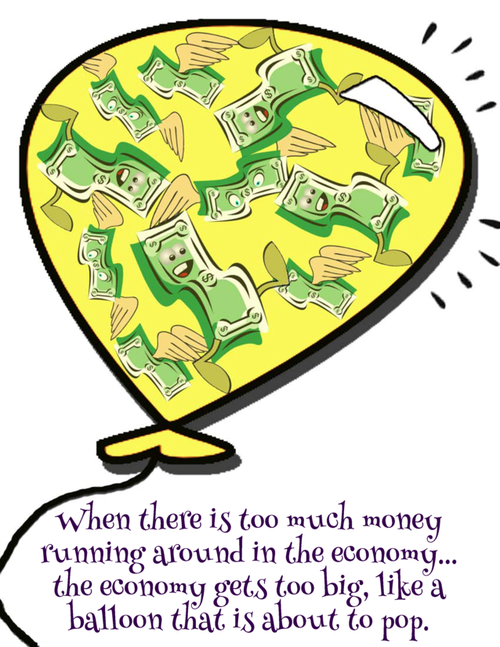

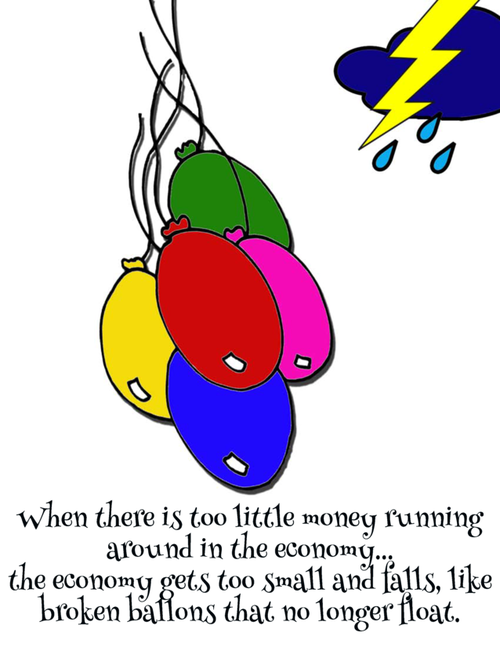

Of course, too much monetary stimulus is bad because it causes inflation (the balloon about to pop). But too little monetary stimulus is bad because it causes unemployment (the broken balloons). And how much stimulus a given amount of money provides depends a lot on whether it is at work in the economy (running around) or locked away in a bank vault, in a corporate treasury, or under a mattress, doing nothing.

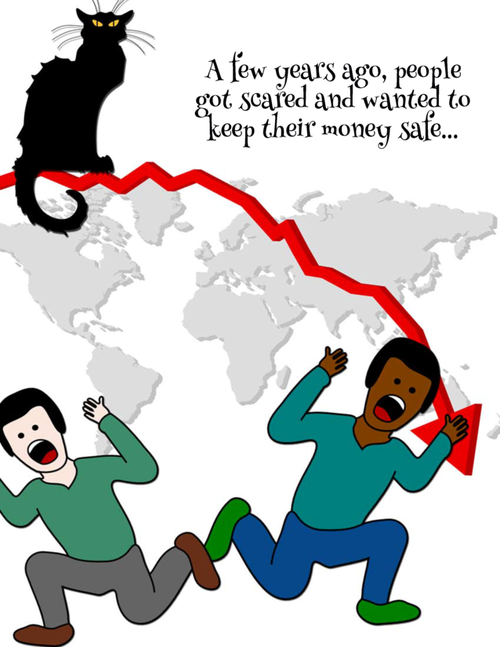

The reason a lot of money has been lying around doing nothing is because the appropriate interest rate for the economy has been very low—below zero. If we had negative interest rates for a year or so, things would get back to normal. Without that tonic, bad times drag on and on.

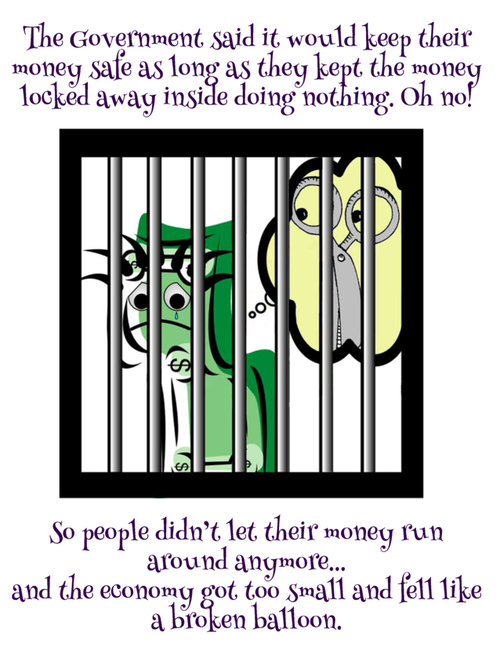

A key thing to understand is that the rest of the government is preventing the Federal Reserve (Ben the Money Master and his friends) from doing what it needs to do to heal the economy. Here is how: the government prevents interest rates from going below zero by the way it handles paper currency. As things are now, holding a pile of paper currency is a way for people to earn a zero interest rate without putting their money to work in the economy.

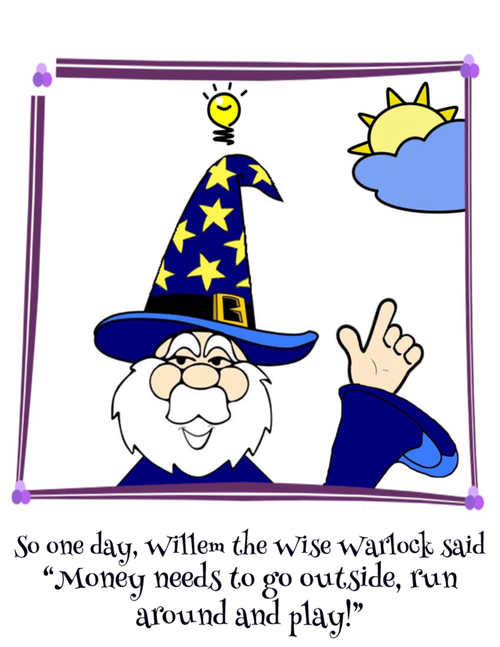

There is a solution, due in its modern form to Willem Buiter, now chief economist of CitiGroup, who appears in the story as “Willem the Wise Warlock.” Buiter discusses various options for repealing what economists call “the zero lower bound”: the economically damaging government guarantee that anyone can lend as much as they want to the government at a zero interest rate just by keeping a big pile of cash. I have elaborated on one of Willem Buiter’s ideas in Quartz, on my blog, and in presentations to central banks around the world, including the Federal Reserve Board.

If we do what it takes to make money sitting around doing nothing shrink, it will provide a strong boost to the economy as people put money to work in the economy. Not everyone will like it, but it will quickly bring full economic recovery, without the bad side effects of other means of trying to stimulate the economy (such as budget deficits or encouraging financial bubbles). Once the economy recovers, everything can go back to what people are used to. Some economists talk about the possibility that negative interest rates might be needed for a long time, but I don’t buy it. In my view, negative interest rates should only be needed for a short time during serious economic slumps. If the Fed and other central banks are given that authority, recessions can be brief and people can get back to work again.

One of the most important reasons we need to keep the economy in good working order—in this case with appropriate monetary policy—is so that economics can recede a bit more into the background of people’s lives. Then people can concentrate again on the things that should matter most: nurturing relationships with friends and family, creating wild, wonderful varieties of meaning in their lives, and taking time to stand in awe of the universe.

We all know that the way to prevent the troubles that would be caused by shooting ourselves in the foot is to avoid shooting ourselves in the foot. Just so, our economic troubles have a straightforward cause and a straightforward technical solution. Both the cause of our troubles and the essence of the solution to our troubles are told in Milton the Maltese Falcon’s ballad.