The Medium-Run Natural Interest Rate and the Short-Run Natural Interest Rate

Note: This post was the lead-up to my post “On the Great Recession.” After reading this one, I strongly recommend you take a look at that post.

Online, both in the blogs and on Twitter, I see a lot of confusion about the natural interest rate. I think the main source of confusion is that there is both a medium-run natural interest rate and a short-run natural interest rate. Let me define them:

- medium-run natural interest rate: the interest rate that would prevail at the existing levels of technology and capital if all stickiness of prices and wages were suddenly swept away. That is, the natural rate of interest rate is the interest rate that would prevail in the real-business cycle model that lies behind a sticky-price, sticky-wage, or sticky-price-and-sticky-wage model.

- short-run natural interest rate: the rental rate of capital, net of depreciation, in the economy’s actual situation. From here on, I will shorten the phrase “real rental rate of capital, net of depreciation” to "net rental rate.“

Both the short-run and medium-run natural interest rates are distinct from actual interest rate, but in the short run, the short-run natural interest rate is much more closely linked to the actual interest rate than the medium-run natural interest rate is.

The Long Run, Medium Run, Short Run and Ultra Short Run

Introductory macroeconomics classes make heavy use of the concepts of the "short run” and the “long run.” To think clearly about economic fluctuations at a somewhat more advanced level, I find I need to use these four different time scales:

- The Ultra Short Run: the period of about 9 months during which investment plans adjust–primarily as existing investment projects finish and new projects are started–to gradually bring the economy to short-run equilibrium.

- The Short Run: the period of about 3 years during which prices (and wages) adjust gradually bring the economy to medium-run equilibrium.

- The Medium Run: the period of about 12 years during which the capital stock adjusts gradually to bring the economy to long-run equilibrium.

- The Long Run: what the economy looks like after investment, prices and wages, and capital have all adjusted. In the long run, the economy is still evolving as technology changes and the population grows or shrinks.

Obviously, this hierarchy of different time scales reflects my own views in many ways. And it is missing some crucial pieces of the puzzle. Most notably, I have left out entry and exit of firms from the adjustment processes I listed. I don’t know have fast that process takes place. It could be an important short-run adjustment process, or it could be primarily a medium-run adjustment process. Or it could be somewhere in between.

The Medium-Run Natural Interest Rate

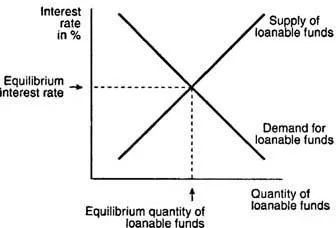

The importance of the medium-run natural interest rate is this: it is the place the economy will tend to once prices and wages have had a chance to adjust–as long as those prices and wages adjust fast enough that the capital stock won’t have changed much by the time that adjustment is basically complete. (I called that last assumption the “fast-price adjustment approximation” in my paper “The Quantitative Analytics of the Basic Neomonetarist Model”–the one paper where I had a chance to use the name of my brand of macroeconomics: Neomonetarism. See my post “The Neomonetarist Perspective” for more on Neomonetarism. The fast-price adjustment approximation is what makes good math out of the distinction between the short run and the medium run.) The medium-run natural interest rate is not a constant. Indeed, at the introductory macroeconomics level, the standard model of the market for loanable funds is a model of how the medium-run natural interest rate is determined. Here is the key graph for the market for loanable funds, from the Cliffsnotes article on “Capital, Loanable Funds, Interest Rate”:

A common mistake students make is to try to use the market for loanable funds graph to try to figure out what the interest rate will be in the short run. That doesn’t work well. Although technically possible, it would be confusing, since how far the economy is above or below the natural level of output has a big effect on both the supply and the demand for loanable funds that using the market for loan. To understand the short-run natural interest rate, it is much better to use a graph designed for that purpose–a graph that focuses on how the short-run natural interest rate is determined by the demand for capital to use in production and by monetary policy.

The Short-Run Natural Interest Rate

Above, I defined the short-run natural interest rate as the "rental rate of capital, net of depreciation,“ or "net rental rate,” for short. What does this mean?

Renting Capital. First, to understand what it means to rent capital, think of those ubiquitous office parks. If the capital a company or other firm needs is an office to work in, it can rent one in an office park like this:

In retail, the capital a firm needs to rent might be retail space in a strip mall:

If a firm is in construction or landscaping, the capital it needs might be a bulldozer, which it can rent from the Cat Rental Store, among other places.

Of course, sometimes a firm needs specialized machine that it has to buy, because those machines are hard to rent. In that case, let me treat it as two different firms: one that buys the specialized machine and puts it out for rent, and another firm that rents the machine. The same trick works for a specialized building that is hard to rent, such as a factory designed for a particular type of manufacturing. When firms that own buildings or machinery are short of cash, sometimes they separate themselves into exactly these two pieces, and sell the piece that owns the specialized buildings or machines so the other piece of the firm can get the cash from the sale of those buildings or machines, while still being able to use those buildings and machines by paying to rent them.

The (Gross) Rental Rate. I will call the gross rental rate simply “the rental rate." The rental rate is equal to the rent paid on a building or piece of equipment divided by the purchase price of that building or piece of equipment. Because this is one price (expressed for example in dollars per year) divided by another price (dollars per machine), the rental rate is a real rate–that is, it does not need to be adjusted for inflation. The rental rate is usually expressed in percent per year, meaning the percent of the purchase price that has to be paid every year in order to rent the machine.

The Net Rental Rate. It is useful to adjust the rental rate for depreciation, however. The paradigmatic case of depreciation is physical depreciation: a machine or building wearing out. More generally, a machine or building might become obsolete or start to look worse in comparison with newer machines. I am going to treat obsolescence as a form of depreciation. Obsolescence shows up in the price of new machines or buildings of that type falling relative to the prices of other goods in the economy. There are other things that can affect the prices of machines and buildings that will matter for the story below, but the rate of physical depreciation and the rate of obsolescence measured by declines in the real price of new machines and buildings of given types at the long-run trend rate are the two to subtract from the rental rate to get the net rental rate.

The Determination of Physical Investment

Physical investment is the creation of new capital–such as machines, buildings, software, etc.–that can be used as factors of production to help produce goods and services. Notice that I am using the phrase "physical investment” to distinguish what I am talking about from “financial investment.” So in this case, at some violence to the English language, I include writing new software in “physical investment."

The amount of physical investment is determined by the costs and benefits of creating new machines, buildings, software, etc. now instead of later. Say we are talking about whether to create or purchase a building or machine now, or a year from now. The benefit of creating a new building or machine a year earlier is the rent that building or machine could earn in that year. In the absence of capital and investment adjustment costs (to which I return below), the cost of creating a new building or machine a year earlier is

- interest on the amount paid to create or purchase the building or machine.

- physical depreciation

- obsolescence

Dividing all of the costs and benefits by the amount paid to create or purchase the building or machine, the costs and benefits per dollar spent on the machine are

benefit relative to amount spent = rental rate

cost relative to amount spent = real interest rate + physical depreciation rate + obsolescence rate

The reason it is the real interest rate in the cost relative to amount spent is because the obsolescence rate is being measured in terms of a real price decline.

In the absence of capital and investment adjustment costs, the rule for physical investment is:

- If the rental rate is less than (the real interest rate + physical depreciation rate + obsolescence rate), invest later.

- If the rental rate is more than (the real interest rate + physical depreciation rate + obsolescence rate), invest now.

If I move the physical depreciation rate and the obsolescence rate to the other side of the comparison, I can say the same thing this way:

- If the rental rate net of net of physical depreciation and obsolescence is below the real interest rate, invest later.

- If the rental rate net of physical depreciation and obsolescence is above the real interest rate, invest now.

Or more concisely:

- If the net rental rate is less than the real interest rate, invest later.

- If the net rental rate is more than the real interest rate, invest now.

Finally, using the definition of the short-run natural interest rate as the net rental rate and flipping the order, I can describe the rule for investment this way:

- If the real interest rate is above the short-run natural interest rate (the net rental rate), invest later.

- If the real interest rate is below the short-run natural interest rate (the net rental rate), invest now.

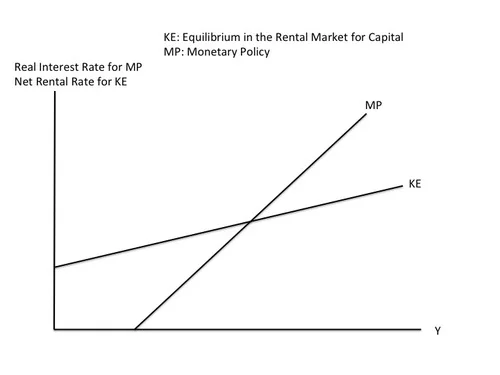

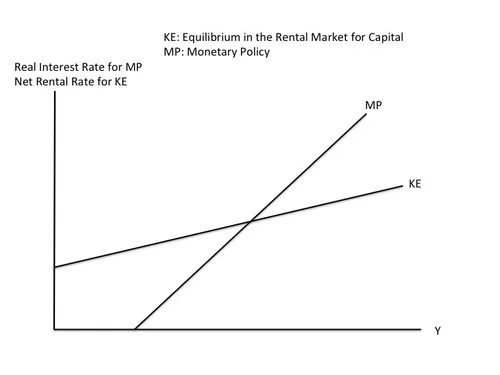

The Determination of the Short-Run Natural Interest Rate: Capital Equilibrium (KE) and Monetary Policy (MP)

Susanto Basu and I have a rough working paper on the determination of the short-run natural interest rate and about very-short-run movements of the actual interest rate in relation to the short-run natural interest rate:

"Investment Planning Costs and the Effects of Fiscal and Monetary Policy” by Susanto Basu and Miles Kimball.

We also have a set of slides to go along with the paper:

Slides for “Investment Planning Costs and the Effects of Fiscal and Monetary Policy” by Susanto Basu and Miles Kimball.

The short-run natural interest rate is determined by (a) equilibrium in the rental market for capital and (b) monetary policy.

Capital Equilibrium (KE): Supply and Demand for Capital to Rent

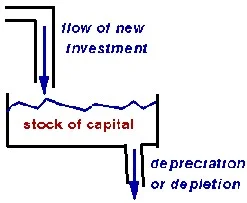

The Supply of Capital to Rent: The supply of capital to rent cannot change very fast. It takes time to create enough new machines, buildings, software, etc. through physical investment to affect the total amount of capital available to rent in any significant way. Wikipedia has an excellent article “Stock and flow” about this relationship between capital and physical investment. The canonical illustration is this picture of a bathtub:

Turning the tap on full blast might double the flow of water, but it will still take time for that flow to significantly affect the overall level of water in the tub. Similarly, turning investment on full blast may double the rate of physical investment creating new machines, buildings, software, etc., but it will still take time to significantly affect the overall amount of capital that exists in the form of machines, buildings, software, etc.

The Demand for Capital to Rent: The most important thing to understand about the demand for capital to rent is that it is higher in booms than in recessions. The more goods and services people want to buy, the more capital firms will want to rent at any given rental price in order to produce those goods and services. Ask any business person who has been involved in a decision to buy capital and they will tell you that they are more eager to get hold of capital to use when business is good than when business is bad.

The way I think of why the demand for capital to rent is higher in a boom than in a recession is this:

- Since profit is revenue minus cost, whatever amount of output a profit-maximizing firm decides to produce to sell or inventory, it should try to produce that amount of output at the lowest possible cost.

- In a boom a firm will produce more output than in a recession (other things equal).

- Since the stock of capital can’t change very fast, when the economy booms and firms add worker hours, a typical firm will not have as much capital per unit of labor as before.

- The more the economy booms, the higher wages will be. (How much depends on whether wages are sticky or not. On sticky wages, if you are prepared for a hardcore economics post, see “Sticky Prices vs. Sticky Wages: A Debate Between Miles Kimball and Matthew Rognlie.”)

- What is true of labor is also true for intermediate goods firms use as material inputs into production: when the economy booms and firms buy more materials to use, a typical firm will not have as much capital per unit of material inputs as before.

- Also, the more the economy booms, the higher the price of intermediate goods used as material inputs will be. (How much depends on whether the prices of the material inputs are sticky or not.)

- When the typical firm has less capital per unit of other inputs, it will be more eager to rent capital at any given rental price.

- If the firm is employing more labor and using more of other inputs despite wages and other input prices being high, it will be especially eager to rent additional capital at a given rental price, since capital then is relatively cheaper than other inputs.

The math behind this story is in the Basu-Kimball paper “Investment Planning Costs and the Effects of Fiscal and Monetary Policy.” There, although it is not needed to get these results, for simplicity we use the fact that for Cobb-Douglas production functions, the ratio of how much a cost-minimizing firm spends on labor and on capital is fixed. (See the relatively hardcore post “The Shape of Production: Charles Cobb’s and Paul Douglas’s Boon to Economics.”) Using the letters

- R for the the rental rate,

- K for the amount of capital,

- W for the wage, and

- L for the amount of total worker hours,

that means

RK = constant * WL.

Dividing both sides of this equation gives an equation for the rental rate:

R = constant * WL/K.

Since the total amount of capital K in the economy can’t change very fast, the total amount of capital in the typical firm also can’t change fast, so increases in wages W and total worker hours will push up the rental rate. And the net rental rate will parallel the overall gross rental rate very closely.

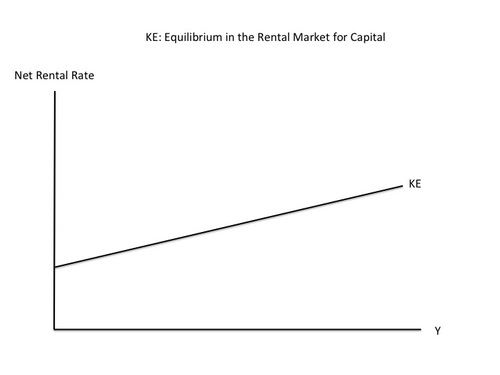

The KE Curve. With the supply of capital relatively fixed (or technically “quasi-fixed”) at any moment in time, a higher demand for capital means a higher equilibrium rental rate in the market for renting capital. How much a typical firm chooses to produce is closely related to how much output the economy as a whole produces. (Indeed, the amount firms produce must add up to the amount of output in the economy as a whole.) So the overall gross rental rate–and the net rental rate–will be increasing in the amount of output the economy as a whole produces. And of course, the amount of output the economy as a whole produces is GDP, for which we will use the single letter y. Thus, the graph below, which has GDP on the horizontal axis, and like the graph at the top of this post, shows an upward slope for the KE curve:

The KE Curve vs. the IS Curve. The IS curve has no microfoundations. The KE curve does. That is, I just explained where the KE curve comes from. The explanations of where the IS curve comes from are either incoherent, or really imply something very different from the IS curve taught in introductory and intermediate macroeconomics classes. Let me critique several ways people convince themselves the IS curve is OK. (Don’t worry if you haven’t heard of some of the interpretations I am critiquing.)

- The consumption Euler equation as an IS curve: The consumption Euler equation is an equation about changes rather than levels. Much more seriously, the consumption Euler equation acts like some sort of IS curve only in models that don’t have investment or other durables. Investment and other durables play such a big role in economic fluctuations that it It is hard to take a model of economic fluctuations that leaves out investment and other durables seriously. Bob Barsky, Chris House and I show how big a difference it makes to sticky price models to bring in investment or other durables goods in our paper “Sticky-Price Models and Durables Goods,” which appears in the American Economic Review.

- Q-theory as a foundation for the IS curve: Like the consumption Euler equation, Q-theory yields a dynamic equation, instead of one that can be drawn as a simple curve with output on the horizontal axis and the real interest rate on the vertical axis. Q-theory says that firms might invest now even if the interest rate is above the net rental rate as long as the level of investment is increasing over time. The reason is that it will be harder to invest later when investment is proceeding faster, so it could make sense to get a jump on things and invest now. On the other hand, firms might delay investment even if the interest rate is below the net rental rate if the level of investment is decreasing over time. The reasons is that it will be easier to invest later when investment is proceeding more slowly, so it could make sense to wait until later when investment can be done in a more leisurely way. Suppose that we show the short-run equilibrium in terms of output and the real interest rate (rather than the net rental rate) and that higher investment is associated with higher GDP, as is usually the case. Then in relation to the KE curve, what Q-theory means is that the short-run equilibrium can be above the KE curve if that equilibrium point is moving to the right (GDP is increasing along with investment), while the short-run equilibrium can be below the KE curve if the equilibrium point is moving to the left (GDP is decreasing along with investment). But the slower the equilibrium point is moving, the closer it has to be to the KE curve. So when the “short-run” lasts a long time, as it has in the last five years since the bankruptcy of Lehman Brothers, the short-run equilibrium needs to be quite close to the KE curve. I discuss how the speed with which the economy is headed toward the medium-run equilibrium affects what can be gotten out of the Q-theory story in “The Quantitative Analytics of the Basic Neomonetarist Model.”

- Heterogeneity of investment projects as a foundation for the IS curve: Heterogeneous investment projects, with some being able to clear a high interest-rate hurdle and some only being able to clear a low-interest-rate hurdle is the traditional story for the IS curve. This is actually a very interesting story, and one my coauthors Bob Barsky, Rudi Bachmann and I have been thinking about for a project in the works, but it actually points to something much more complex than an IS curve. For example, if potential investment projects are heterogeneous, then in general, one needs to keep track of how many are still available of each type. In any case, there is nothing simple about such a story.

The MP Curve. Central banks periodically meet to determine the interest rate they will set. The rate they set is a nominal interest rate, where “nominal” just means it is the interest rate that non-economists think of. The real interest rate is the nominal interest rate minus expected inflation. Inflation expectations tend to change quite slowly and sluggishly, so the nominal interest rate the central bank chooses determines the real interest rate in the short run and the very short run. Central banks ordinarily raise their interest rate target when the economy is booming and lower it when the economy is in recession, so the interest rate (both nominal and real) will be upward sloping in output. Indeed, in order to make the economy stable, the central bank should make sure that the real interest rate goes up faster with output than the net rental rate does, so that, going from left to right, the MP curve showing how the central banks target interest rate depends on output cuts the KE curve from below, as shown in the complete KE-MP diagram:

In the KE-MP model, the intersection of the KE and MP curves is the short-run equilibrium of the economy. In short-run equilibrium, the real interest rate equals the net rental rate, or equivalently, the real interest rate equals the short-run natural interest rate.

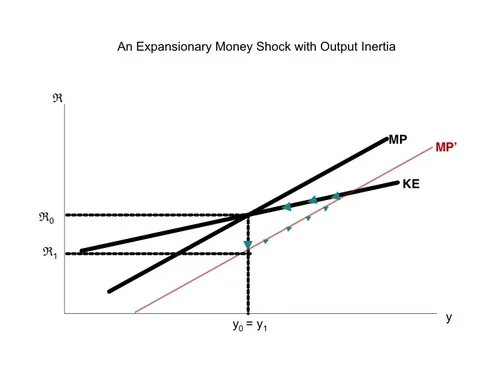

The Ultra Short Run

What brings the economy to short-run equilibrium is the adjustment of investment based on the gap between the net rental rate determined by the KE (capital rental market equilibrium) curve and the real interest rate determined by the MP (monetary policy) curve. But it takes time for firms to adjust their investment plans. Indeed, the level of investment is unlikely to adjust much faster than existing investment projects are completed and a new round of investment projects is started, as Susanto Basu and I discuss in “Investment Planning Costs and the Effects of Fiscal and Monetary Policy.” In the meanwhile, before investment has had time to full adjust, output can be away from its short-run equilibrium level, and the interest rate determined by the MP curve can be different from the net rental rate determined by the KE curve.

For example, suppose that the economy starts out in short-run equilibrium, but then the central bank decides to make a change in the interest rate change for some reason other than a change in the level of output. Since output is unchanged, the change in the interest rate corresponds in the KE-MP model to a shift in the MP curve. The graph below, taken from Slides for “Investment Planning Costs and the Effects of Fiscal and Monetary Policy,” shows the effects of a monetary expansion.

The movement up along the MP’ curve reflects the ultra-short-run adjustment of investment to get to the new short-run equilibrium–a process that might take about 9 months. The movement back along the unchanging KE curve reflects the short-run adjustment of prices to get back to the original (and almost unchanged) medium-run equilibrium. Since the real interest rate is on the axis, the point representing first ultra-short-run equilibrium, and then short-run equilibrium, is always on the MP curve. (The graph does not show the gradual shift of the MP curve back to return the economy to the medium-run equilibrium. One way for that adjustment of the MP curve to happen is if there is some nominal anchor in the monetary policy rule so that the level of prices matters for monetary policy, not just the rate of change of prices.)

Why It Matters: Remarks About the KE-MP Model

- The reason I wrote this post is because many people don’t seem to understand that low levels of output lower the net rental rate and therefore lower the short-run natural interest rate. Leaving aside other shocks to the economy, monetary policy will not tend to increase output above its current level unless the interest rate is set below the short-run natural interest rate. That means that the deeper the recession an economy is in, the lower a central bank needs to push interest rates in order to stimulate the economy. In the Q-theory modification of the KE-MP model, the belief that the economy is going to recover fast could generate extra investment even if interest rates are somewhat higher, but when such confidence is lacking, the remedy is to push interest rates below the net rental rate that is the short-run natural interest rate.

- As discussed in “Investment Planning Costs and the Effects of Fiscal and Monetary Policy” and the Slides for “Investment Planning Costs and the Effects of Fiscal and Monetary Policy,” fiscal policy and technology shocks have counterintuitive effects on the KE curve. This is grist for another post. Also grist for another post is the way a version of the Keynesian Cross comes into its own in the ultra short run, but only during the 9 months or so of the ultra short run.

- If a country makes the mistake of having a paper currency policy that prevents it from lowering the nominal interest rate below zero, then the MP curve has to flatten out somewhere to the left. (The zero lower bound on the nominal interest rate puts a bound of minus expected inflation on the real interest rate. That makes the floor on the real interest rate higher the lower inflation is.) The lower bound on the MP curve might then make it hard to get the interest rate below the net rental rate (a.k.a. the short-run natural interest rate). In my view, this is what causes depressions. QE can help, but is much less powerful than simply changing the paper currency policy so that the nominal interest rate can be lowered below the short-run natural interest rate, however low the recession has pushed that short-run natural interest rate. (See the links in my post “Electronic Money, the Powerpoint File” and all of my posts on my electronic money sub-blog.)

U.S. Team Takes Second at International Mathematical Olympiad | Mathematical Association of America →

I was interested in the news about the US Math Team (of high school students) this year because I was asked to be an alternate to the US Math Team in 1977, the end of my senior year in high school. I tell that story here, in a set of storified tweets that I link at my sidebar:

Clay Christensen, Jerome Grossman and Jason Hwang on the Three Basic Types of Business Models

In The Innovator’s Prescription, Clay Christensen, Jerome Grossman and Jason Hwang make good use of a typology of business models laid out by C. B. Stabell and Øystein Fjeldstad in their May, 1998 Strategic Management Journal article “Configuring Value for Competitive Advantage: On Chains, Shops and Networks.” Modifying Stabell and Fjeldstad’s terminology a bit for clarity, Clay and his coauthors call the three types of business models solutions shops, value-adding processes, and facilitated networks. Clay, Jerome and Jason argue that these three types of business models are so different that it is difficult to efficiently house them under one roof. They give these definitions for these three types of business models (from about location 360):

Solution Shops

These “shops” are businesses that are structured to diagnose and solve unstructured problems. Consulting firms, advertising agencies, research and development organizations, and certain law firms fall into this category. Solution shops deliver value primarily through the people they employ—experts who draw upon their intuition and analytical and problem-solving skills to diagnose the cause of complicated problems. After diagnosis, these experts recommend solutions. Because diagnosing the cause of complex problems and devising workable solutions has such high subsequent leverage, customers typically are willing to pay very high prices for the services of the professionals in solution shops.

The diagnostic work performed in general hospitals and in some specialist physicians’ practices are solution shops of sorts. …

Value-Adding Processes

Organizations with value-adding process business models take in incomplete or broken things and then transform them into more complete outputs of higher value. Retailing, restaurants, automobile manufacturing, petroleum refining, and the work of many educational institutions are examples of VAP businesses. Some VAP organizations are highly efficient and consistent, while others are less so.

Many medical procedures that occur after a definitive diagnosis has been made are value-adding process activities….

Facilitated Networks

These are enterprises in which people exchange things with one another. Mutual insurance companies are facilitators of networks: customers deposit their premiums into the pool, and they take claims out of it. Participants in telecommunications networks send and receive calls and data among themselves; eBay and craigslist are network businesses. In this type of business, the companies that make money tend to be those that facilitate the effective operation of the network. They typically make money through membership or user fees.

Networks can also be an effective business model for the care of many chronic illnesses that rely heavily on modifications in patient behavior for successful treatment. Until recently, however, there have been few facilitated network businesses to address this growing portion of the world’s health-care burden. …

Clay, Jerome and Jason’s central idea is that medicine will be more efficient if there is one medical institution designed for inherently expensive “solution shop” activities such as difficult diagnoses, other much more convenient and inexpensive clinics for the routine treatment of well-diagnosed diseases, and online networks for patients to discuss their contribution as patients to disease management with others who have the same disease. What wouldn’t survive would be the current hospital model where the solution shop aspect of what they do confers high expense on many other activities that don’t have to be so expensive. Here is the way Clay, Jerome and Jason say it:

The two dominant provider institutions in health care—general hospitals and physicians’ practices—emerged originally as solution shops. But over time they have mixed in value-adding process and facilitated network activities as well. This has resulted in complex, confused institutions in which much of the cost is spent in overhead activities, rather than in direct patient care. For each to function properly, these business models must be separated in as “pure” a way as possible.

This is not just a matter of static efficiency:

The health-care system has trapped many disruption-enabling technologies in high-cost institutions that have conflated two and often three business models under the same roof. The situation screams for business model innovation. The first wave of innovation must separate different business models into separate institutions whose resources, processes, and profit models are matched to the nature and degree of precision by which the disease is understood. Solution shops need to become focused so they can deliver and price the services of intuitive medicine accurately. Focused value-adding process hospitals need to absorb those procedures that general hospitals have historically performed after definitive diagnosis. And facilitated networks need to be cultivated to manage the care of many behavior-dependent chronic diseases. Solution shops and VAP hospitals can be created as hospitals-within-hospitals if done correctly.

Further Musings: Even apart from this application to health care, I have found the typology of solution shop, value-adding process and facilitated network very interesting to think about for understanding my own work life (as a complement to the kind of analysis I talked about in my post “Prioritization”).

I work at the University of Michigan. Universities combine research–which is quintessentially a solution shop activity–with teaching, which has a big component of value-adding processes. And of course, Tumblr, Twitter and Facebook, where I put in effort as a blogger, are facilitated networks.

The idea of a value-adding process highlights the gains to be had from routinizing something. It is good to periodically ask oneself if there is anything in my daily activities that I can make more routine and streamlined.

The idea of a facilitated network highlights the gains to be had by having users do a lot of the work. That in turn is related both to the benefits of laissez faire under a decent system of rules and the idea of delegation, which typically involves giving up some control at the detailed level.

I find for me, however, that I love the “solution-shop” aspect of life so much that I think I resist routinization. I don’t know if this is what I should be doing, but I would rather keep thinking about how I am doing things than have everything fade into the background of routine. That does cost me extra time, as I do things inefficiently because I am thinking too much about them as I do them.

Here is a link to a sub-blog of all of my posts tagged as being about Clay Christensen’s work

Rich People Who Believe in Behavioral Economics

From Harvard Magazine, July-August 2014:

… the [Harvard] Faculty of Arts and Sciences disclosed a $17-million donation from the Pershing Square Foundation–founded by Bill (William A.) Ackman ‘88, M.B.A. '92, CEO of the Pershing Square Capital Management hedge fund, and Karen Ackman, M.L.A. '93–for a “foundation of human behavior” initiative grounded in behavioral economics and other disciplines. That gift provides for three new professorships and a research fund.

Matthew O'Brien: The 10 Biggest U.S. Cities by GDP →

In addition to Matthew O'Brien’s article “The 10 Biggest U.S. Cities by GDP,” as a counterpoint, see Richard Florida’s list of US metro areas by GDP per person: “America’s Most Productive Metros.” That list looks very different.

Math Camp in a Barn

Image created by Miles Spencer Kimball. I hereby give permission to use this image for anything whatsoever, as long as that use includes a link to this post. For example, t-shirts with this picture (among other things) and http://blog.supplysideliberal.com/post/92400376217/math-camp-in-a-barn on them would be great! :)

I like Naomi Schefer Riley’s account in the Wall Street Journal of Ben Chavis’s math camp in North Carolina’s poorest county: “Math Camp in a Barn: Intensive Instruction, No-Nonsense Discipline” (googling the title of a Wall Street Journal article jumps over the paywall, so my link is to the search page). Naomi’s article illustrates two related principles I have written about. First, almost anyone can learn math with enough hard work and a can-do attitude, as Noah Smith and I write in “There’s One Key Difference Between Kids Who Excel at Math and Those Who Don’t.” Second, a key element of learning is simply time spent learning, as I write about in “Magic Ingredient 1: More K-12 School.” Lengthening the school year is one of the most straightforward ways to increase learning, especially in hard subjects. Naomi points out the arithmetic of math instruction:

From 8:30 a.m. to 4 p.m. Monday through Friday the children learn math, interspersed with some reading, physical education and lunch. Each gets 120 hours of instruction during the three weeks, equivalent to what they would get in a year at a typical public school.

Among many other serious problems with education in the United States, our attachment to the idea of summer vacation is an important one.

John Stuart Mill's Rejection of Anarcho-Capitalism

The Anarcho-Capitalism of Murray Rothbard does not recognize the legitimacy of taxation even to fund police protection. John Stuart Mill has a broader view of what a state can legitimately do. In On Liberty, Chapter IV, “Of the Limits to the Authority of Society over the Individual” paragraphs 1-3, he writes:

What, then, is the rightful limit to the sovereignty of the individual over himself? Where does the authority of society begin? How much of human life should be assigned to individuality, and how much to society?

Each will receive its proper share, if each has that which more particularly concerns it. To individuality should belong the part of life in which it is chiefly the individual that is interested; to society, the part which chiefly interests society.

Though society is not founded on a contract, and though no good purpose is answered by inventing a contract in order to deduce social obligations from it, every one who receives the protection of society owes a return for the benefit, and the fact of living in society renders it indispensable that each should be bound to observe a certain line of conduct towards the rest. This conduct consists first, in not injuring the interests of one another; or rather certain interests, which, either by express legal provision or by tacit understanding, ought to be considered as rights; and secondly, in each person’s bearing his share (to be fixed on some equitable principle) of the labours and sacrifices incurred for defending the society or its members from injury and molestation. These conditions society is justified in enforcing at all costs to those who endeavour to withhold fulfilment. Nor is this all that society may do. The acts of an individual may be hurtful to others, or wanting in due consideration for their welfare, without going the length of violating any of their constituted rights. The offender may then be justly punished by opinion, though not by law.

John’s argument that “every one who receives the protection of society owes a return for the benefit” is one that Elizabeth Warren has been echoing to argue for the legitimacy of taxation to support a wide range of government activities. E. J. Dionne’s review of her book A Fighting Chance in the Washington Post offers these quotations from the book:

1. “There is nobody in this country who got rich on his own,” she said. “Nobody. You built a factory out there? Good for you. But I want to be clear: You moved your goods to market on the roads the rest of us paid for. You hired workers the rest of us paid to educate. You were safe in your factory because of police forces and fire forces that the rest of us paid for.” …

2. “There’s nothing pro-business about crumbling roads and bridges or a power grid that can’t keep up,” she writes. “There’s nothing pro-business about cutting back on scientific research at a time when our businesses need innovation more than ever. There’s nothing pro-business about chopping education opportunities when workers need better training.”

Although her specific examples of government action in these quotations sound fairly benign, the way Elizabeth is using the argument that "every one who receives the protection of society owes a return for the benefit" does not provide any obvious principle for putting a bound on what the government can legitimately raise taxes for. I suspect that, if magically revived in the modern world, John Stuart Mill would argue for a more limited government than the one Elizabeth Warren advocates. (And it is clear from the passage in On Liberty quoted above that he would not go along with her invocation of a “social contract.”)

7 Strategies to Help Raise Happy Kids | Nourishment Notes →

The “You, too, can learn math” column Noah Smith and I wrote (currently, my most popular column, by far) is flagged in one of the 7 points about raising kids in the link above. :)

Count to ten when a plane goes down... →

John Beck is a friend of mine from middle school and high school. At the link above, he tells this story of Korean Airlines flight 007, which may have lessons for today.

Just a little under 31 years ago, I played a key role in a conspiracy theory that grew up around a passenger plane downed by a Russian missile. Trust me, I did not mean to be involved. …

Update: Quartz picked this blog post up here.

Bruce Bartlett on Access to Research Results

Bruce Bartlett, who also appears in the post “Bruce Bartlett on Careers in Economics and Related Fields” gave this reaction to my presentation “On the Future of the Economics Blogosphere”:

I think you missed an opportunity to criticize academic journals for excessive cost and severe paywall constraints. The inability of many readers to access the underlying research is a major problem for blogs to advance serious debate. While in many cases, working paper versions can be located, this applies to only a fraction of the research that is out there. You should criticize academics who don’t post their work in places like SSRN or on personal web sites. My understanding is that unless you literally sign away your rights, you have the right to post your own work on your own web site.

In other words, each of us who produces published research has a lot of discretion to make the results of our research available inexpensively. Let’s do it.

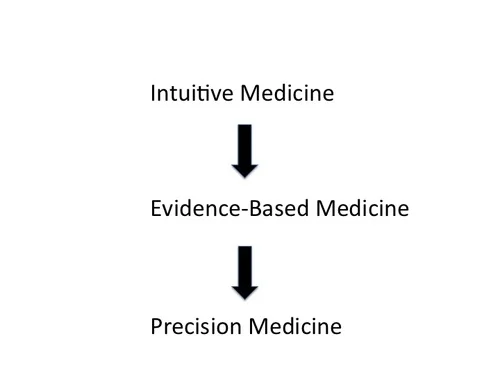

Clay Christensen, Jerome Grossman and Jason Hwang on Intuitive Medicine vs. Precision Medicine

I found the passage below from The Innovator’s Prescription (location 333), by Clay Christensen, Jerome Grossman and Jason Hwang especially insightful. It puts diagnosis at the center of medicine, especially when viewing medicine from a business point of view. Better and better diagnosis opens up the possibility of more cost-efficient treatments for those diseases that are precisely identified. But that possibility must be seized.

Our bodies have a limited vocabulary to draw upon when they need to express that something is wrong. The vocabulary is comprised of physical symptoms, and there aren’t nearly enough symptoms to go around for all of the diseases that exist—so diseases essentially have to share symptoms. When a disease is only diagnosed by physical symptoms, therefore, a rules-based therapy for that diagnosis is typically impossible—because the symptom is typically just an umbrella manifestation of any one of a number of distinctly different disorders.

The technological enablers of disruption in health care are those that provide the ability to precisely diagnose by the cause of a patient’s condition, rather than by physical symptom. These technologies include molecular diagnostics, diagnostic imaging technology, and ubiquitous telecommunication. When precise diagnosis isn’t possible, then treatment must be provided through what we call intuitive medicine, where highly trained and expensive professionals solve medical problems through intuitive experimentation and pattern recognition. As these patterns become clearer, care evolves into the realm of evidence-based medicine, or empirical medicine—where data are amassed to show that certain ways of treating patients are, on average, better than others. Only when diseases are diagnosed precisely, however, can therapy that is predictably effective for each patient be developed and standardized. We term this domain precision medicine.

… disruption-enabling diagnostic technologies long ago shifted the care of most infectious diseases from intuitive medicine (when diseases were given labels such as “consumption”) to the realm of precision medicine (where they can be defined as precisely as different types of infection, different categories of lung disease, and so on). To the extent that we know what type of bacterium, virus, or parasite causes one of these diseases—and when we know the mechanism by which the infection propagates—predictably effective therapies can be developed—therapies that address the cause, not just the symptom. As a result, nurses can now provide care for many infectious diseases, and patients with these diseases rarely require hospitalization. Diagnostics technologies are enabling similar transformations, disease by disease, for families of much more complicated conditions that historically have been lumped into categories we have called cancer, hypertension, Type II diabetes, asthma, and so on.

When I was a kid, we talked about “curing cancer” as the prototypical world-shaking accomplishment. The reason there is no one “cure for cancer” is that cancer is not one disease but hundreds of different diseases involving different genes going awry in the direction of too much growth. A cure needs to be found for each one of those diseases in order for there to be a cure for the amorphous notion of “cancer.” Many of these diseases have been cured and others are well on their way to being cured. But other diseases under the general heading of “cancer” have not even been identified yet (in the sense of carefully distinguishing them from other diseases with similar symptoms). Once they have been identified at the level of the particular gene that goes awry to produce that particular disease, they will be halfway to being cured.

The term “personalized medicine” is sometimes used for what I would call “treating the disease someone actually has instead of some other disease.” A better phrase for that is the phrase Clay, Jerome and Jason use: “precision medicine.”

Quartz 49—>Will Narendra Modi’s Economic Reforms Put India on the Road to Being a Superpower?

Here is the full text of my 49th Quartz column, “Why you really want India to join the US and China as a superpower" now brought home to supplysideliberal.com. It was first published on June 13, 2014. Links to all my other columns can be found here.

I kept my working title as the title of this companion post, since it better reflects the content of the column.

If you want to mirror the content of this post on another site, that is possible for a limited time if you read the legal notice at this link and include both a link to the original Quartz column and the following copyright notice:

© June 13, 2014: Miles Kimball, as first published on Quartz. Used by permission according to a temporary nonexclusive license expiring June 30, 2017. All rights reserved.

Iraq joined Syria in civil war and Ukraine’s crisis persisted this week. And yet let me argue that this week’s most important geopolitical news is the economic program of India’s new prime minister, Narendra Modi.

Any increase in the chances for a full-scale supply-side transformation of India’s economy is cause to cheer for many reasons. First and foremost, faster economic growth in India would lift hundreds of millions of people out of dire poverty. But its geopolitical significance should not be underestimated. India is the only nation that rivals China in its population–and is on track to surpass China’s population. As I wrote in a previous Quartz piece, “Benjamin Franklin’s strategy to make the US a superpower worked once, why not try it again?”:

The reason China’s economic rise matters for US grand strategy is that China has a much larger population than the United States. … if China has ¼ the per capita GDP, but four times as many people, its total GDP will be the same size. … Power corrupts. So … it should surprise no one that the US has done some bad things as a superpower. Yet I am convinced that the combination of Chinese nationalism and “Communist” oligarchy—or the combination of Chinese nationalism with some tumultuous future political transition in China—would lead a dominant China to behave much worse than the US has.

I believe a future in which India joins China and the US as a superpower would be a safer world than one in which China and the United States are the only superpowers. News of Chinese saber-rattling over territorial disputes has become a commonplace in the last few years. Here is a recent example. And the 25th anniversary of the Tiananmen Square Massacre is a reminder of the ugliness of China’s politics now and the tough road China has ahead even in the best-case scenario in which it does become more democratic.

Narendra Modi’s own past is a reminder that India has its own political ugliness. He is the only person to ever have been denied a US visa based on a law designed to punish foreign officials for “severe violations of religious freedom,” since as the head of the Indian state of Gujarat, he failed to stop a Hindu vs. Muslim riot that left more than 1,000 people dead.

Yet, India has been a functioning democracy since 1950, with genuine handoffs of power between different political parties since 1977. And both the religious tensions Modi fatally mishandled and the welfare state he now challenges point to the orientation of Indian politics primarily toward domestic issues, rather than territorial disputes with neighboring countries. What ideological gap exists between the Indian electorate and the US electorate would be narrowed further if further economic liberalization in India is successful. So I do not worry about what India might do as a future superpower the way I worry about what China might do.

What does India’s new government plan to do to make the Indian economy as big as possible, as fast as possible? One key element of the policy address by India’s president Pranab Mukherjee earlier this week, reflecting the prime minister’s agenda, is to make making agricultural markets more competitive, so that farmers can get a better price for their crops. The Wall Street Journal explains:

Subsidies and make-work schemes discourage farmers from concentrating on maximizing yields. Under the Agriculture Produce Marketing Committee Act, they are required to sell produce to monopolistic middlemen. As a result, much of India’s harvest rots before it gets to consumers, further driving up food prices.

The policy address outlines the rest of Modi’s agenda:

- “Minimum government, maximum governance;”

- “basic infrastructure such as roads, shelter, power and drinking water” in rural areas;

- helping farmers to farm better in order to raise yields;

- pursuing irrigation projects;

- more use of massively open online courses (MOOCs) for education with the most bang for the buck;

- toilets for everyone;

- garbage collection;

- making sure girls receive an education and are protected from violence;

- encouraging groups of states within India to cooperate on economic development;

- combating corruption with “transparent systems and timebound delivery of government services;”

- trying to eliminate “obsolete laws, regulations, administrative structures and practices;”

- digitization of government records;

- “Wi-Fi zones in critical public areas” and broad-band in every village;

- social media as a way of getting feedback about how government is doing;

- “rationalisation and simplification of the tax regime to make it non-adversarial and conducive to investment, enterprise and growth” including reducing taxation of saving and investment by shifting toward a value added tax;

- reducing red tape to “enhance the ease of doing business;”

- providing workers with “access to modern financial services;”

- creating “dedicated freight corridors and industrial corridors” as attractive destinations for investment;

- more airports and upgraded seaports;

- 100 newly developed cities;

- allowing more foreign investment in making military equipment to make this sector more efficient.

There is always a big gap between government promises and government performance. But this list of initiatives is remarkable for what it doesn’t emphasize. There is not much in the way of direct handouts. By contrast, I learned at a “Cashless Society” workshop, sponsored by New York University’s Urbanization Project, that under the previous Indian government, when government officials came to take the biometric measurements to make it possible to establish identitywithout needing an identity card, people were happy to cooperate because they see government officials coming to town as a sign that some new handout, subsidy, or goody is on the way.

Most of the things Modi’s government is promising are things that, if delivered, will foster the quantity and quality of private economic activity. To give just two examples, more toilets would not only reduce the number of girls who get raped while going out to the fields to relieve themselves, it would save those girls a lot of time every day that they could devote to their schoolwork. And pushing the educational system heavily in the direction of massively open online courses could speed India toward the kind of low-cost, effective education that ace management guru Clay Christensen and his coauthors predict is the future of education everywhere in the world.

The policy address by the new Indian government is also relatively sophisticated in realizing the obstacles to rolling out new policies. It recognizes that, as a practical matter, many things that need to be done for economic development need to be done at the level of Indian states or groups of Indian states, rather than at the national level. If some states are more willing to work with the national government to foster economic development than others, those states can move ahead faster, and hopefully at some point, citizens of the remaining states will insist on policies like the successful policies of neighboring states.

In a previous election, Modi’s Bharatiya Janata Party (BJP) began using the slogan “India Shining.” If the new Indian government is able to implement even half of its policy agenda, and subsequent Indian governments continue to push further along the road of supply-side improvement, it won’t be long before “India Shining” is no longer just a slogan. It will be an accurate description of the world’s newest superpower.

- Important Note: Thirumaran makes the case in these storified tweets that Narendra Modi has been given a bad rap for his performance during the Gujarat riots in 2002.What I say in my column about that incident is based entirely on the Wall Street Journal article "Why Narendra Modi Was Banned From the U.S.” I would be glad to hear reactions to Thirumaran’s additional perspective.

Populations of the Most Populous Nations. I found the population figures in Wikipedia’s “World population” for the most populous countries very interesting.

- China: 1,364,970,000

- India: 1,245,280,000

- United States: 318,201,000

- Indonesia: 247,008,052

- Brazil: 201,032,714

- Pakistan: 186,709,000

- Nigeria: 173,615,000

- Bangladesh: 152,518,015

- Russia: 143,657,134

- Japan: 127,180,000

I hadn’t realized that the US was the third most populous nation. All of Europe, including 110,000,000 in the European part of Russia, is only listed at 742,000,000. The reason it makes sense to focus on population figures is that catch-up economic growth up to the cutting-edge level of income per capita is much easier than the economic goal of the US of pushing income per capita to levels the world has never seen before for any large nation.

I was clued into India being headed for beating out China in overall population by Thomas Piketty’s Capital in the 21st Century. It is a fat enough book that I am only partway through. And I am glad I am reading it on a Kindle.

“The type of personal responsibility that is needed to be good in the clutch is different. It is always there, but under pressure it becomes purely focused and is the underlying force in the action: I am doing this because it is the right thing to do, and if I fail, I know I tried. Responsibility here is not accounting for your actions; it is your actions. And however it turns out, you are the one who did it. … That is responsibility. That is doing what is right and leaving the rest to be sorted out.”

– Paul Sullivan, Clutch p. 143

Will Women Ever Get the Mormon Priesthood?

Until I was almost 18 years old, the Mormon Church would not ordain men of black African descent to the Mormon priesthood. That all changed in 1978–a change I wrote about in these posts:

- The Pope and the Prophet: Letting Go

- Flexible Dogmatism: The Mormon Position on Infallibility

- Christian Kimball on the Fallibility of Mormon Leaders and on Gay Marriage

Having changed its policy to allow men of African descent to be ordained, could the Mormon Church ever allow women to be ordained? On the one hand, the Mormon Church recently excommunicated Kate Kelly for founding and leading the group Ordain Women, which advocates allowing women to be ordained to the Mormon priesthood. (See Emma Green’s June 24, 2014 Atlantic article “Kicked Out of Heaven for Wanting Women Priests.” And here is a podcast of an excellent interview with Kate Kelley that Sid Sharma alerted me to.) On the other hand, it seems as if Ordain Women’s efforts are having some effect. Among those efforts, one of the most powerful has been organizing women to line up to get into (and get turned away from) the “Priesthood Session” of the Mormon Church’s twice-a-year “General Conference.” The Mormon Church’s sensitivity to this bit of activism is indicated by the efforts it has made to ban news cameras from Temple Square to avoid more pictures of Ordain Women’s protest about women being excluded.

Kate Kelly did not want to be thrown out of the Mormon Church. My view is that, given the realities of how the Mormon Church as an institution operates, Kate Kelly’s sacrifice of being willing to stand her ground and be excommunicated was an important contribution toward greater equality between men and women in the Mormon Church, for two reasons. First, organizing women for a highly visible protest of women’s exclusion–and Kate’s excommunication itself–get Mormons talking about the issue.

Second, the advocacy of Ordain Women creates space for quite a bit of movement toward greater equality under cover of saying “Those women trying to get into the Priesthood Session of General Conference are going too far, but …”. In other words, progress often requires someone to volunteer to be the hippie for “hippie-punching.” (See Josiah Neeley’s guest post “The Science of Hippie-Punching on Noah Smith’s blog Noahpinion for an explanation of the term "hippie-punching.”)

Even top leaders of the Mormon Church can now push for greater equality between men and women while reassuring more conservative colleagues that they won’t go too far in undoing the traditional exclusion of women from positions of power by agreeing that Kate Kelly had to be excommunicated. (The concern of more conservative Mormon leaders would be to (a) keep the Mormon Church from looking bad and (b) to set limits.) Given the likely discussions among top Mormon leaders about what to do about Ordain Women before Kate Kelly was actually excommunicated, it is appropriate to see Mormon Apostle Dallin Oaks’s General Conference talk “The Keys and Authority of the Priesthood” as the outcome of such dynamics within the leadership of the Mormon Church. (As you can see from Suzette Smith's Ordain Women blog post “Reflections on Elder Oaks’ Remarks in the Priesthood Session of General Conference," I am not alone in seeing Dallin Oaks’s talk as a favorable development for women’s equality in the Mormon Church.)

In the Mormon Church, the longest-serving apostle still alive becomes the head–President and Prophet–of the Mormon Church. And seniority in this sense of time in rank is also very important in how Mormon leaders interact with one another. Dallin Oaks is currently the 5th most senior apostle, and several of the more senior apostles are in poor health due to advanced age. Also, before being appointed to high church office, Dallin Oaks was a high-powered lawyer. So other Mormon Church leaders trust him to present their position well. Given his lawyer’s training, Dallin is careful to represent the collective views of the Mormon Church leadership, but he himself has a mild liberal streak, having served as founding member of the editorial board of Dialogue: A Journal of Mormon Thought, which sometimes hosts articles in opposition to official positions of the Mormon Church (including keyarticles that helped prepare the way for the extending the Mormon priesthood to men of black African descent.

Here are some key passages from Dallin’s General Conference talk "The Keys and Authority of the Priesthood” with my commentary after each passage.

1. With the exception of the sacred work that sisters do in the temple under the keys held by the temple president, which I will describe hereafter, only one who holds a priesthood office can officiate in a priesthood ordinance.

Mormon temples are at a much higher level of sacredness than the regular meetinghouses where Sunday services are held. They are the site of many powerful and very interesting rituals that non-Mormons never see. The passage just above from Dallin’s talk is remarkable for openly acknowledge that in Mormon temples, women officiate in certain rituals in what to all appearances is a priestly capacity fully parallel to the way in which men officiate in a priestly capacity in the corresponding rituals. If Mormon women took roles this closely parallel to those taken by men in rituals outside of temples as well, they would have a version of the Mormon priesthood in all but name.

2. We are accustomed to thinking that all keys of the priesthood were conferred on Joseph Smith in the Kirtland Temple, but the scripture states that all that was conferred there were “the keys of this dispensation” (D&C 110:16). At general conference many years ago, President Spencer W. Kimball reminded us that there are other priesthood keys that have not been given to man on the earth, including the keys of creation and resurrection.

Dallin’s reference to one of my (unfortunately deceased) grandfather Spencer W. Kimball’s statements is a reminder that, as the official distillation of Mormon belief into thirteen “Articles of Faith” says, “we believe that [God] will yet reveal many great and important things pertaining to the kingdom of God.” In context, this is a positive note that God could open the door to ordination, or at least more extensive priestly or priest-like roles for Mormon women. (A good example of an additional priest-like role for Mormon women that would not be too radical a change from current policy would be if Mormon women were once again encouraged, as they were in the 19th century, to give healing blessings–that is, when appropriate, to put their hands on someone’s head while saying a prayer for that person to recover from a sickness.)

3. The divine nature of the limitations put upon the exercise of priesthood keys explains an essential contrast between decisions on matters of Church administration and decisions affecting the priesthood. The First Presidency and the Council of the First Presidency and Quorum of the Twelve, who preside over the Church, are empowered to make many decisions affecting Church policies and procedures—matters such as the location of Church buildings and the ages for missionary service. But even though these presiding authorities hold and exercise all of the keys delegated to men in this dispensation, they are not free to alter the divinely decreed pattern that only men will hold offices in the priesthood.

Just as Mormon Church leaders said about extending the Mormon priesthood to men of African descent, Dallin is saying it would take a special revelation from God to extend the Mormon priesthood to women. But of course, Mormons believe that God did give a special revelation in 1978 that the Mormon priesthood should be offered to all faithful men. So that is not at all ruling out more extensive priestly roles for women, only saying that Mormon Church leaders would have to feel they had a powerful subjective spiritual experience (which they interpreted with confidence as an actual communication from God) in favor of such a change before they would think they had the warrant to do so.

4. In an address to the Relief Society, President Joseph Fielding Smith, then President of the Quorum of the Twelve Apostles, said this: “While the sisters have not been given the Priesthood, it has not been conferred upon them, that does not mean that the Lord has not given unto them authority. … A person may have authority given to him, or a sister to her, to do certain things in the Church that are binding and absolutely necessary for our salvation, such as the work that our sisters do in the House of the Lord. They have authority given unto them to do some great and wonderful things, sacred unto the Lord, and binding just as thoroughly as are the blessings that are given by the men who hold the Priesthood.”

In that notable address, President Smith said again and again that women have been given authority. To the women he said, “You can speak with authority, because the Lord has placed authority upon you.” He also said that the Relief Society “[has] been given power and authority to do a great many things. The work which they do is done by divine authority.” And, of course, the Church work done by women or men, whether in the temple or in the wards or branches, is done under the direction of those who hold priesthood keys. Thus, speaking of the Relief Society, President Smith explained, “[The Lord] has given to them this great organization where they have authority to serve under the directions of the bishops of the wards … , looking after the interest of our people both spiritually and temporally.”

Thus, it is truly said that Relief Society is not just a class for women but something they belong to—a divinely established appendage to the priesthood.

We are not accustomed to speaking of women having the authority of the priesthood in their Church callings, but what other authority can it be? When a woman—young or old—is set apart to preach the gospel as a full-time missionary, she is given priesthood authority to perform a priesthood function. The same is true when a woman is set apart to function as an officer or teacher in a Church organization under the direction of one who holds the keys of the priesthood. Whoever functions in an office or calling received from one who holds priesthood keys exercises priesthood authority in performing her or his assigned duties.

In giving this quotation from Joseph Fielding Smith, an earlier church leader who later became President of the Mormon Church, Dallin not only alludes again to the clearly priest-like functions women perform in Mormon temples, but also says that while women do not have “the priesthood,” they routinely have “the authority of the priesthood” in the many “callings” (appointive church volunteer positions) in which they serve in the Mormon Church. The effect is to more nearly equate the prestige of the callings women serve in to the callings men serve in.

5. As stated in the family proclamation, the father presides in the family and he and the mother have separate responsibilities, but they are “obligated to help one another as equal partners.” Some years before the family proclamation, President Spencer W. Kimball gave this inspired explanation: “When we speak of marriage as a partnership, let us speak of marriage as a full partnership. We do not want our LDS women to be silent partners or limited partners in that eternal assignment! Please be a contributing and full partner.”

In the eyes of God, whether in the Church or in the family, women and men are equal, with different responsibilities.

Despite its origins as a document hoping to hold the line against legal gay marriage (a topic I address here), and its essentialist views on gender, “The Family: A Proclamation to the World” does say that men and women are equal. This and other official statements that men and women are equal because they have the potential to counteract the very understandable inference by Mormons that since only men hold the priesthood, men are more than equal to women. It is this difficult-to-suppress inference that is the most damaging aspect of Mormon women being excluded from priesthood offices–much more damaging than the (significant) hurt from not being able to perform certain rituals.

6. In his insightful talk at BYU Education Week last summer, Elder M. Russell Ballard gave these teachings:

“Our Church doctrine places women equal to and yet different from men. God does not regard either gender as better or more important than the other. …

“When men and women go to the temple, they are both endowed with the same power, which is priesthood power. … Access to the power and the blessings of the priesthood is available to all of God’s children.”

In most religions that have ordained women, women have gained the opportunity to take on exactly the same offices as men. That is the usual pattern. But in Mormonism, what the threads of past tradition point to as a more likely resolution of the current structural inequality between men and women is (a) the recognition of a parallel priesthood for women that is different, but of equal dignity and (b) inclusion of women in all the decision-making councils of the church on the basis of their separate but equal priesthood. Already it is well within the discretion of the bishop who leads a Mormon congregation to include female leaders in the key decision-making meetings. (And many do.) A simple step for the Mormon Church would be to insist that all bishops do this, rather than merely allowing it. A more radical step would be to recognize the top female leader in a Mormon congregation as the co-equal of the bishop, just as the church leaders Dallin quotes recognize the wife as a co-equal of the husband in a marriage.

One of the great strengths of Mormonism is its adaptability. Unlike in Catholicism, where the Pope is limited to interpreting the preexisting tradition, the Mormon Prophet can declare de novo revelations from God. And to the extent precedents are desired, Joseph Smith, the founder of Mormonism, was creative enough (and other Mormon leaders also felt latitude to be creative given the doctrine that they could get inspiration from God) that a wide variety of precedents are available. The Mormon hierarchy is set up in such a way that it is led by old men, who have a great deal of wisdom from their life experience. So it is resistant to fads and sometimes resistant to changes that should happen. But with the lag one would expect from the age structure of the leadership, many changes that should happen eventually do happen. Someday, I expect women to have a much more equal station in the Mormon Church than they do now. As part of that equality, I see a future Mormon Church that is led by wise old women as well as wise old men.

Despite being a non-supernaturalist myself, I know that religions that expect belief in the supernatural matter a lot to their adherents, just as religions that fully welcome non-supernaturalists matter to people like me. And having grown up within Mormonism, and having many friends and family who are still believers, makes me care about Mormonism. I think that equality between men and women is important for both supernaturalist and non-supernaturalist religions. However, in religions that believe in the supernatural, beliefs about the distribution of supernatural gifts between men and women matter. One way or another, I hope that Mormonism finds its way to a greater level of equality between men and women, as I think it will.

– written in Rome

Tomas Hirst on the Decline in the Medium-Run Natural Interest Rate →

In the Alphaville post linked above, Tomas Hirst gives a persuasive account of why the level of interest rates that will hold after economic recovery is likely to be lower than in the past.

(For the difference between the medium-run natural interest rate and the short-run natural interest rate, see “The Medium-Run Natural Interest Rate and the Long-Run Natural Interest Rate.”)

Clay Christensen, Jerome Grossman and Jason Hwang on the Personal Computer Revolution

I saw the personal computer revolution firsthand. It all went down very fast. In December 1973, when I was 13, I got a chance to use a calculator for the first time. I was visiting my brother Christian Kimball (1, 2), who was then an undergraduate at Harvard; there was a calculator in one of the Harvard libraries that allowed me to do conversions between 3-dimensional radial coordinates of nearby stars to xyz coordinates so I could better understand the layout of our interstellar neighborhood. A year and half later, in 1975, I learned a little computer programming at an NSF supported math camp at Utah State University. In 1978 and 1979 I had to get special access to Harvard Business School computers in order to run some regressions. But in August 1983, I convinced my father (1, 2) to help me buy a used Osborne “portable” computer. It wasn’t easy to learn to use, but I did ultimately write my Harvard Ph.D. program economic history paper “Farmer’s Cooperatives as Behavior Towards Risk” (which was ultimately published in the American Economic Review). In 1986 and 1987, when I wrote my dissertation, I was only able to manage to typeset all of the equations because my wife Gail was an ace scientific secretary with access to the needed computers and software. (After I convinced her to marry me and move to Massachusetts, she found a job working as a secretary first for professors at Harvard Business School and then later for Eric Maskin, Mike Whinston in the Economics Department.) But by Fall of 1987, as a new assistant professor at the University of Michigan, I could typeset equations myself using TeX (not yet LaTeX) on the new desktop computer the University of Michigan had given me.

In The Innovator’s Prescription (location 316), Clay Christensen, Jerome Grossman and Jason Hwang give this analytical account of the personal computer revolution:

Until the 1970s there were only a few thousand engineers in the world who possessed the expertise required to design mainframe computers, and it took deep expertise to operate them. The business model required to make and market these machines required gross profit margins of 60 percent just to cover the inherent overhead. The personal computer disrupted this industry by making computing so affordable and accessible that hundreds of millions of people could own and use computers.

The technological enabler of this disruption was the microprocessor, which so simplified the problems of computer design and assembly that Steve Wozniak and Steve Jobs could slap together an Apple computer in a garage. And Michael Dell could build them in his dorm room.

However, by itself, the microprocessor was not sufficient. IBM and Digital Equipment Corporation (DEC) both had this technological enabler inside their companies, for example. DEC eschewed business model innovation and tried instead to commercialize the personal computer from within its minicomputer business model, a model that simply could not make money if computers were priced below $50,000. IBM, in contrast, set up an innovative business model in Florida, far from its mainframe and minicomputer business units in New York and Minnesota. In its PC business model, IBM could make money with low margins, low overhead costs, and high unit volumes. By coupling the technological and business model enablers, IBM transformed the computing industry and much of the world with it, while DEC was swept away.

And it wasn’t just the makers of expensive computers that were swept away. The systems of component and software suppliers, and the sales and service channels that had sustained the mainframe and minicomputer industries, were all disrupted by a new supporting cast of companies whose economics, technologies, and competitive rhythms matched those of the personal computer makers. An entire new value network displaced the old network.

The analogy Clay, Jerome and Jason draw to health care is that one need not despair when seeing how the bulk of health care providers are set up to do things in a very expensive way. As long as we don’t let regulations smother new providers, doing things in new, less expensive ways–though perhaps at first in somewhat lower quality ways–there is hope. (See “Clay Christensen, Jerome Grossman and Jason Hwang on the Agenda for the Transformation of Health Care” and “Tyler Cowen: Regulations Hinder Development of Driverless Cars.”)