The Aquatic, Groupish, Warlike Ape

Darwin’s Dangerous Idea has been one of the most influential books in my thinking and in my life. One of the most memorable examples in that book was Max Westenhoefer and the Alister Hardy’s “Aquatic Ape Hypothesis”: the idea that human beings are evolved for living on the seashore. The idea of being an “aquatic ape” resonates with me because I have always loved swimming and I love seeing ocean waves crash against a beach. Curtis Marean’s article “The Most Invasive Species of All” in the August 2015 issue of Scientific American touched on the Aquatic Ape Hypothesis. He writes on page 36:

Genetic and archaeological evidence suggests that H. sapiens underwent a population decline shortly after it originated, thanks to a global cooling phase that lasted from around 195,000 to 125,000 years ago. Seaside environments provided a dietary refuge for H. sapiens during the harsh glacial cycles that made edible plants and animals hard to find in inland ecosystems and were thus crucial to the survival of our species. These marine coastal resources also provided a reason for war. Recent experiments on the southern coast of Africa, led by Jan De Vynck of Nelson Mandela Metropolitan University in South Africa, show that shellfish beds can be extremely productive, yielding up to 4,500 calories per hour of foraging. My hypothesis, in essens, is that coastal foods were a dense, predictable and valuable food resource. As such, they triggered high levels of territorialisty among humans, and that territoriality led to intergroup conflict. This regular fighting between groups provided conditions that selected for prosocial behaviors within groups–working together to defend the shellfish beds and thereby maintain exclusive access to this precious resource–which subsequently spread throughout the population.

Paul Krugman on the Gravity Equation of Trade →

This is a very interesting column by Paul Krugman in his area of professional expertise.

An Underappreciated Power of a Central Bank: Determining the Relative Prices between the Various Forms of Money Under Its Jurisdiction

Any unlimited opportunity to lend to the government at a zero interest rate creates a zero lower bound. In practice, when currency regions have gone to negative interest rates, as Switzerland, Denmark, Sweden and the euro zone have, they have lowered their interest rates on reserves, so it is the unlimited opportunity to lend to the government at a zero interest rate by withdrawing paper currency from the bank that seems to be the toughest issue.

The opportunity to lend to the government at a zero interest rate by prepaying taxes is another interesting issue. but as my brother Chris and I argued in “However Low Interest Rates Might Go, the IRS Will Never Act Like a Bank,” for the US at least, it is a limited one, unless the Secretary of Treasury intends to subvert the negative interest rate policy. Once one is paying all one’s taxes at the beginning of the tax year, there is no further available arbitrage on that front, since the between-year tax rate is by law supposed to be set by the Secretary of the Treasury in line with other short-term interest rates.

How can a central bank keep people from shifting their money into paper currency when interest rates are negative? The long answer can be found in all the links in my bibliographic post “How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide.” The short answer can be found in the CEPR’s 5-minute interview with me:

The basic idea depends on one of the roles of central banks that many “Money and Banking” textbooks fail to mention: the role of determining how much, among all the forms of money under its jurisdiction, each type is worth compared to the others. Let me use the example of Japan, since I thought about this issue in the context of writing “Is the Bank of Japan Succeeding in Its Goal of Raising Inflation?” and “Japan Should Be Trying Out a Next-Generation Monetary Policy” last week. Ultimately, it is not the numbers “10000” and “1000” written on them that make a ten-thousand-yen note equal in value to ten one-thousand-yen notes—it is the fact that the Bank of Japan is willing to freely convert a ten-thousand-yen note into ten one-thousand-yen notes and vice versa. Such conversions happen at a part of the central bank so underappreciated that some central bankers don’t even know where it is: the cash window.

It Isn’t the Face Value that Determines How Much Each Type of Paper Currency is Worth. To see this role of a central bank clearly, consider a case where not only direct access to the central bank, but access to the banking system in general is problematic: the criminal underworld. Think of the standard scene in American mob movies in which the mobster demands a suitcase full of cash in tens and twenties. Why tens and twenties? Using the banking system often increases the chance that a criminal will get caught. Money can be laundered, but it is easier to launder tens and twenties. So, at least near the point of money laundering, ten ten-dollar bills are worth more than one hard-to-launder hundred-dollar bill. That means that if you bring me a suitcase full of one-hundred dollar bills with the same face value as a suitcase full of tens and twenties, you are bringing me less value—you have cheated me.

The Exchange Rate Between Paper Currency and Electronic Money. Just as central banks determine the relative value of different denominations of paper currency by how they treat them at the cash window, they also determine how much paper currency is worth compared to electronic money in a reserve account by how they treat the paper currency at the cash window. A reserve account here is a private bank’s bank account with the central bank; for the Bank of Japan, the balance in a reserve account is a number in the Bank of Japan’s computer system. If the Bank of Japan treated a paper 1000-yen note as worth 990 electronic yen, that is what it would be worth. Here is what it means to treat a 1000-yen note as worth 990 electronic yen: (a) when a private bank came to the cash window of the Bank of Japan and hands in a paper 1000-yen note to have the money put into its reserve account the Bank of Japan would add only 990 yen to that private bank’s reserve account; (b) when a private bank came to the cash window of the Bank of Japan and asked for a paper 1000-yen note, only 990 yen would be deducted from its reserve account.

By the phrase “forms of money under its own jurisdiction” I mean forms of money that a central bank has the authority to print or otherwise create in unlimited quantities. If a central bank can create unlimited quantities of two forms of money, it can commit to exchange one form for the other at any exchange rate it declares without any reason to worry that it won’t be able to provide the form a bank wants to change another form of money under its authority into. In other words, the central bank has unlimited firepower for defending any exchange rate it declares between different forms of money under its jurisdiction. Moreover, an exchange of one form of money for another at a declared exchange rate does not, in itself, directly change the quantity of high-powered money under the central bank’s jurisdiction (though altering the exchange rate between different forms of money may).

To emphasize, a central bank can easily defend any exchange rate it declares between paper currency and electronic money–just as, say, the Fed can easily defend the exchange rate between $20 bills and $10 bills–since it has the authority to create as much of either one that banks want to change the other into.

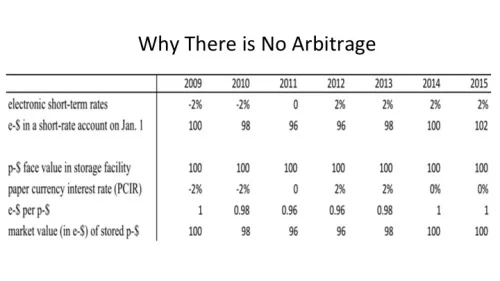

Using the Exchange Rate Between Paper Currency and Electronic Money to Create a Non-Zero Paper Currency Interest Rate. Once a central bank uses it power to determine the relative price of different forms of money under its jurisdiction in earnest, it is straightforward to insure that there is no way to circumvent negative interest rates by storing paper currency. Consider this slide from my presentation “18 Misconceptions about Eliminating the Zero Lower Bound”:

In this example contemplating an alternate history, the central bank has a -2% target rate for two years: 2009 and 2010. To get anything close to a -2% market equilibrium interest rate, the central bank must also reduce it interest rate on reserves to something close to zero. And it needs to reduce its paper currency interest rate to something closer to -2% than to 0. How can it do that? $100 will still have a $100 face value no matter how long it is stored (until cash physically disintegrates). But its market value is determined by how that paper currency with a face value of $100 is treated at the cash window of the central bank. If the central bank treats it as 100 electronic dollars on January 1, 2009, gradually decreasing to 98 electronic dollars on January 1, 2010, and to 96 electronic dollars on January 1, 2011, the rate of return of that paper currency will be -2% per year throughout 2009 and 2010. The idea is to match the paper currency interest rate to the target rate. (One could have a small spread relative to the target rate–say .5% in either direction without causing too much trouble, but the example is simplest if the target paper currency spread is zero.) To match the paper currency interest rate to the 0 target rate in 2011, the central bank need to treat the $100 face value worth of paper currency as $96 electronic throughout 2011. Then with the target rate equal to +2% per year in 2012 and 2013, the central bank can gradually bring the value of the $100 in face value of paper currency back up to being worth $100 electronic around January 1, 2014.

Where the Magic Is. How can an exchange rate between paper currency and electronic money avoid arbitrage without elaborate tracking of each paper note? It is because the rate of change of the exchange rate automatically keeps track of the cumulative paper currency interest rate over the time the paper currency is in private hands–and the paper currency interest rate (really a capital gains rate) is kept equal to the target rate. To reemphasize, it is not the level of the exchange rate between paper currency and electronic money that does the magic, but the rate of change. Just as a sundial keeps track of how much time has passed by how far the shadow has moved, the exchange rate between paper currency and electronic money keeps track of the cumulative interest on paper currency by how far it has moved.

Another Applications of a Central Bank’s Power to Determine the Relative Price of Different Currencies Under Its Jurisdiction: the Electronic Mark.

We are used to thinking of each central bank as having one currency. But it is quite possible for a single institution to supervise more than one currency. I explore the possibilities of a possibility that changes an international exchange rate in conjunction with the exchange rate between paper currency and electronic money in my column “How the Electronic Deutsche Mark Can Save Europe.” The reintroduction of a paper Deutsche Mark would be likely to create immediate, serious problems. The introduction of a purely electronic German mark would work well. In general, when the straightjacket of a single currency becomes too tight, it causes fewer problems to split off a strong currency in electronic form, rather than splitting off a weak currency (as in the worry over Grexit and the reintroduction of the Greek drachma, narrowly averted for now).

Noah Smith—The Fight of the Ages: Pain and Death

This is Noah’s 13th guest religion post on supplysideliberal.com. Don’t miss Noah’s other guest religion posts!

- God and SuperGod

- You Are Already in the Afterlife

- Go Ahead and Believe in God

- Mom in Hell

- Buddha Was Wrong About Desire

- Noah Smith: Judaism Needs to Get Off the Shtetl

- Why Do Americans Like Jews and Dislike Mormons?

- Render Unto Ceasar

- Original Sin

- Islam Needs To Separate Church and State

- Noah Smith—Jews: The Parting of the Ways

- Noah Smith: You With the Fro

Here is Noah:

The other day a good friend of mine killed himself. So I’ve been thinking a bit more about death lately.

For a long time, I’ve thought of death not as a single event, but a continuous process. Elements of your personality, your desires, your beliefs and habits–everything that makes you you–are constantly being altered by experience. An individual is like a ship that gets taken apart and rebuilt plank by plank, until it’s not clear when the old ship died and the new ship came to life. Life is experience, experience is change, and change is death.

This isn’t necessarily a bad thing. Who wants to be preserved in amber? If you want to imagine how bizarre and inhuman that would be, just read “Daddy’s World” by Walter Jon Williams, or “The Wedding Album” by David Marusek.

We fear death because of inborn self-preservation instinct. We’re sad about the deaths of our friends and family because of the lost opportunity of interacting with them in the future, and–sometimes–because we feel frustrated that our friends and family didn’t get the chance to live as much as they should have. But death isn’t necessarily a bad thing–it’s an inevitable and natural thing. It’s what you and I are both experiencing right this moment.

Far worse, I’d argue, is a bad life.

We don’t know why people commit suicide (though we know factors that forecast it, and there are some theories). But it seems certain that for most suicidal people, life involves a great deal of either physical or psychological pain. That pain is a tragedy that is distinct from the tragedy of death itself.

We often see suicide as a mistake, at least when neither terminal illness nor extreme physical pain are involved. We certainly tell people it’s a mistake, in order to stop our friends and family from committing suicide. In fact, it probably is a mistake, from a rational-optimizing-agent economics-type point of view. I know firsthand that depression dramatically distorts people’s estimates of the probability of living a good life. I have no doubt that suicidal feelings (which are not quite the same as depression) create similar breakdowns of rationality. Things like cognitive behavioral therapy and narrative psychology are intended to help people be more rational and not make that big mistake.

But even though suicide is usually a big mistake doesn’t mean that it comes out of the blue. The psychological pain of suicidal people is obvious and undeniable. For some suicidals, the pain lasts for years or decades before it finally becomes too much. And I’d argue that it’s that pain that’s the biggest tragedy. Life is crueler than death.

As a society, we expend a lot of effort trying to stop people from committing suicide. When I searched on Google for reasons that people commit suicide, it sent me straight to the National Suicide Prevention Lifeline (Thanks, Google!). But we spend a lot less time and effort trying to alleviate people’s psychological pain long before they have suicidal ideation. As happens so often with our healthcare system, we ignore preventative medicine and focus entirely on crisis management.

This may be due to a lingering tendency of our society to downplay psychological pain. People who have never been depressed often regard depression as a choice. Deep down, many people probably regard depression and suicidal feelings as a weakness of will, or a manipulative plea for support and sympathy from others.

How many times have you heard some hippie barista in a coffee shop tell you that “Happiness is a choice?” That sounds cute, but it’s really just a modern hipster equivalent of a military commander slapping a soldier with PTSD and yelling at him to snap out of it. We seem to think that if someone doesn’t have a gun to his head right this minute, he’s not in big trouble.

Part of that is understandable. Psychological pain is much less visible than physical pain, and it also probably varies more from person to person. But part of our disdain for psychological pain probably comes from a lingering culture of personal toughness and responsibility.

This approach to psychological pain is not working. The U.S. suicide rate has soared by about 30 percent in recent years. The suicide prevention hotlines are not getting the job done, folks.

As for what we can do to eliminate psychological pain, I have some ideas. But those will have to wait for another time. The point I want to make today is that we need to stop thinking so much about the tragedy of death, and start thinking more about the tragedy of lives filled with psychological pain. Like Mel Gibson said in “Braveheart,” everyone dies, but not everyone truly lives.

“What is indoctrination and how is it different from regular instruction? Indoctrination, suggests Christina Hoff Summers, is characterized by three features, the major conclusions are assumed beforehand, rather than being open to question in the classroom; the conclusions are presented as part of a ‘unified set of beliefs’ that form a comprehensive worldview; and the system is ‘closed,’ committed to interpreting all new data in the light of the theory being affirmed.

Whether this account gives us sufficient conditions for indoctrination, and whether, so defined, all indoctrination is bad college pedagogy, may certainly be debated. According to these criteria, for example, all but the most philosophical and adventurous courses in neoclassical economics will count as indoctrination, since undergraduate students certainly are taught the major conclusions of that field as established truths which they are not to criticize from the perspective of any other theory or worldview; they are taught that these truths form a unitary way of seeing the world; and, especially where microeconomics is concerned, the data of human behavior are presented as seen through the lens of that theory. It is probably good that these conditions obtain at the undergraduate level, where one cannot simultaneously learn the ropes and criticize them–although one might hope that the undergraduate will pick up in other courses, for example courses in moral philosophy, the theoretical apparatus needed to raise critical questions about these foundations.”

– Martha Nussbaum, Cultivating Humanity: A Classical Defense of Reform in Liberal Education, p. 203.

Japan Should Be Trying Out a Next-Generation Monetary Policy

Here is a link to my 66th column on Quartz, “Japan should be trying out a next-generation monetary policy.” My working title was “Japan is wasting its time trying to raise inflation.”

Monday’s post “Is the Bank of Japan Succeeding in Its Goal of Raising Inflation?” was written in conjunction with writing this column.

The Negative Zones

I often have occasion to say that I have presented my proposal for eliminating the zero lower bound all around the world. I give the full list of where I have given talks on eliminating the zero lower bound in “Electronic Money: The Powerpoint File.” To see how literal that statement can be taken, I wanted to tally up how many time zones I can account for, only counting presentations at central banks and their branches. I intend to keep this updated as I add additional time zones.

Here they are, in the order of sunrise on a particular calendar date, with the first date listed when I have been to more than one central bank or branch of a central bank in that time zone. Note that UTC 0 is the same as Greenwich Mean Time.

- UTC+12: Reserve Bank of New Zealand, July 22, 2015

- UTC+9: Bank of Japan, June 18, 2013

- UTC+7: Bank of Thailand, September 29, 2016

- UTC+3: Qatar Central Bank (This was in Education City, off-site from the central bank itself, but a central bank official was my discussant.)

- UTC+2: Bank of Finland, May 20, 2015

- UTC+1: National Bank of Denmark, September 6, 2013

- UTC 0: Bank of England, May 20, 2013

- UTC-5: Federal Reserve Board, November 1, 2013

- UTC-6: Federal Reserve Bank of Chicago, September 3, 2015

To put this in perspective, let me point out that some time zones are not as well provided with central banks and central bank branches as other time zones! But other time zones I hope to add soon.

Beyond Happiness and Satisfaction: Toward Well-Being Indices Based on Stated Preference →

My paper coauthored with Dan Benjamin, Ori Heffetz and Nichole Szembrot on how to build national well-being indices in a principled way is now available to the everyone free on PubMed at the link above.

Slavoj Zizek on the Psychological Insecurities of Terrorists

The Wikipedia article on Charlie Hebdo reports that after the French satirical magazine Charlie Hebdo published cartoons making fun of the the prophet Mohammed,

On 7 January 2015, two Islamist gunmen[53] forced their way into the Paris headquarters of Charlie Hebdo and opened fire, killing twelve: staff cartoonists Charb, Cabu, Honoré,Tignous and Wolinski,[54] economist Bernard Maris, editors Elsa Cayat and Mustapha Ourrad, guest Michel Renaud, maintenance worker Frédéric Boisseau and police officers Brinsolaro and Merabet, and wounding eleven, four of them seriously.

In response, many of those who saw this as an affront to free speech used the slogan “Je suis Charlie,” or “I am Charlie.” But what of the murderers? I liked what the article “Slavoj Žižek on the Charlie Hebdo massacre: Are the worst really full of passionate intensity?”(tweeted to me by John L. Davidson) had to say:

William Butler Yeats’ “Second Coming” seems perfectly to render our present predicament: “The best lack all conviction, while the worst are full of passionate intensity.” …

However, do the terrorist fundamentalists really fit this description? What they obviously lack is a feature that is easy to discern in all authentic fundamentalists, from Tibetan Buddhists to the Amish in the US: the absence of resentment and envy, the deep indifference towards the non-believers’ way of life. If today’s so-called fundamentalists really believe they have found their way to Truth, why should they feel threatened by non-believers, why should they envy them? When a Buddhist encounters a Western hedonist, he hardly condemns. He just benevolently notes that the hedonist’s search for happiness is self-defeating. In contrast to true fundamentalists, the terrorist pseudo-fundamentalists are deeply bothered, intrigued, fascinated, by the sinful life of the non-believers. One can feel that, in fighting the sinful other, they are fighting their own temptation.

It is here that Yeats’ diagnosis falls short of the present predicament: the passionate intensity of the terrorists bears witness to a lack of true conviction. How fragile the belief of a Muslim must be if he feels threatened by a stupid caricature in a weekly satirical newspaper?

“There exist in American life many great habilitating organizations. People meet them young, often before they even know what they are. One of these is the US armed forces; another is the economics profession.”

– David Warsh, Economic Principals: Masters and Mavericks of Modern Economics, p. 289.

Is the Bank of Japan Succeeding in Its Goal of Raising Inflation?

image source

On June 29, 2012, I posted “Future Heroes of Humanity and Heroes of Japan,” advocating just the sort of massive asset purchases the Bank of Japan has undertaken. Although I now think that using deep negative interest rates after eliminating the zero lower bound is a far superior policy, I am still interested to see how well massive quantitative easing has worked.

Japan’s GDP shrank by .4% in the 2d quarter of 2015. It is now slightly below the level it had in the first quarter of 2008, although with the shrinking of the Japanese population, per capita GDP is up about 1% since the first quarter of 2008. Overall, Japan has managed to clamber back up from blows of the Great Recession, but can it achieve sustained, robust economic growth?

Japan's Real GDP

Source: Cabinet Office of Japan. Real GDP shown as the logarithmic percentage above the GDP peak in the first quarter of 2008.

The remarkable Japanese election in December 2012 put Prime Minister Shinzo Abe in charge, and induced a major change in monetary policy, as the Bank of Japan under Governor Haruhiko Kuroda embarked on a program of quantitative easing on steroids, committing to buying bonds and other securities equal in value to over half of GDP every year.

Prices of Key Components of Japan’s GDP

Source: Cabinet Office of Japan. Deflators for components of Real GDP shown as the logarithmic percentage above the price peak in the third quarter of 2008.

“Abenomics” seems to have had an effect. One of the key objectives for monetary policy has been to turn deflation into inflation of 2%. The quarter before Abe’s election was the low point for prices. Since the third quarter of 2012, consumption prices (blue), house construction prices (red) and business investment prices (green) have been on an upward track. Both the consumption prices and residential investment prices have a big jump up between the first and second quarter of 2014 due to Japan’s big sales tax increase. That jump due to the sales tax increase says nothing about whether or not monetary policy is working, so the upward trend in consumption prices is quite unimpressive. But because business spending is exempt from sales taxes, the business investment prices are unaffected by the sales tax increase; business investment prices show a steady increase since Abe was elected.

The steady increase in business investment prices, and volatile upward trend of house construction prices are important because the reason Japan wants to have more inflation is that when businesses build a factor or buy a machine, or someone builds a house, they are comparing the interest rate they have to pay to how fast the value of their investment or house will go up with time—of which inflation is an important component. And the price trends that matter for such investment decisions are the price trends for residential investment and business investment. (Indeed, Bob Barsky, Chris Boehm, Chris House and I have an early stage working paper arguing that for this reason central banks should pay much more attention to investment goods prices than they do.)

One way of seeing how well Japan has turned around its price trends is look at Japanese inflation compared to US inflation. In the graph below, a flat line would mean that Japanese inflation was equal to US inflation. Even after correcting for the sales tax increase, since Prime Minister Abe’s election late in 2012, inflation for consumption and business investment don’t look that different in Japan than in the US, and the lower inflation for residential investment reflects relatively high inflation for that component of GDP in the US rather than a lack of inflation in Japan.

Japanese Price Trends Compared to US Price Trends

Source: Cabinet Office of Japan. Deflators for components of Japan’s Real GDP shown as the logarithmic percentage above the price peak in the third quarter of 2008 minus the logarithmic percentage of the corresponding US prices above their level in the third quarter of 2008.

Japan’s Performance is Still Substandard. So far, this sounds like a rosy picture. But it isn’t. A stagnant economy is a bad outcome. And even if Japan’s current inflation trends continue, they still don’t make a zero interest rate low enough in comparison to set off the investment boom that is needed to jump-start the Japanese economy. After all, the US inflation statistics used as a point of reference for Japan’s above don’t give the Fed that much room to maneuver under current policy parameters either.

How Japan Can Get Out of Its Bind. What Japan needs is an even more dramatic shift in its monetary policy: deep negative interest rates.

In a recent Quartz column, I talk about the growing acceptance of the idea that the so-called “zero lower bound” or “effective lower bound” on interest rates can be eliminated. In particular, a time-varying paper currency deposit fee on net deposits at the cash window of a central bank can make it possible to cut interest rates as low as needed, without having to worry about people hoarding paper currency. The secret is that the central bank is promising to convert money in the bank into more and more paper currency in the future—at a more than 1-for-1 exchange rate, so storing cash is a worse deal than taking a negative interest rate in the bank but then being able to convert those funds into cash at a favorable exchange rate in the future. If interest rates later turn positive, this process can be reversed, or if necessary, it can go on indefinitely. I have personally visited central banks all over the world explaining such an approach, and take care to explain to central bank staffers and decision-makers how smoothly this can work.

When I visited the Bank of Japan in June 2013 to explain how to eliminate the zero lower bound on interest rates and use deep negative rates to revive the Japanese economy, the Bank of Japan wasn’t ready. Given the partial success that they have had with massive quantitative easing, and the dramatic election results it took to get to that far, I still don’t think don’t think the Bank of Japan is ready for deep negative interest rates. But that is the first step on Japan’s road back to a vibrant economy.

John Stuart Mill on the Gravity of Divorce

One thing I like in John Stuart Mill’s On Liberty is his consistent distinction between what deserves criticism from what deserves legal prohibition. Divorcing without sufficient cause someone who has been encouraged by fair promises to build their life on the assumption that a marriage will be lasting is a good example. Here is what he says in paragraph 11 of On Liberty “Chapter V: Applications”:

Baron Wilhelm von Humboldt, in the excellent essay from which I have already quoted, states it as his conviction, that engagements which involve personal relations or services, should never be legally binding beyond a limited duration of time; and that the most important of these engagements, marriage, having the peculiarity that its objects are frustrated unless the feelings of both the parties are in harmony with it, should require nothing more than the declared will of either party to dissolve it. This subject is too important, and too complicated, to be discussed in a parenthesis, and I touch on it only so far as is necessary for purposes of illustration. If the conciseness and generality of Baron Humboldt’s dissertation had not obliged him in this instance to content himself with enunciating his conclusion without discussing the premises, he would doubtless have recognised that the question cannot be decided on grounds so simple as those to which he confines himself. When a person, either by express promise or by conduct, has encouraged another to rely upon his continuing to act in a certain way—to build expectations and calculations, and stake any part of his plan of life upon that supposition—a new series of moral obligations arises on his part towards that person, which may possibly be overruled, but cannot be ignored. And again, if the relation between two contracting parties has been followed by consequences to others; if it has placed third parties in any peculiar position, or, as in the case of marriage, has even called third parties into existence, obligations arise on the part of both the contracting parties towards those third persons, the fulfilment of which, or at all events the mode of fulfilment, must be greatly affected by the continuance or disruption of the relation between the original parties to the contract. It does not follow, nor can I admit, that these obligations extend to requiring the fulfilment of the contract at all costs to the happiness of the reluctant party; but they are a necessary element in the question; and even if, as Von Humboldt maintains, they ought to make no difference in the legal freedom of the parties to release themselves from the engagement (and I also hold that they ought not to make much difference), they necessarily make a great difference in the moral freedom. A person is bound to take all these circumstances into account, before resolving on a step which may affect such important interests of others; and if he does not allow proper weight to those interests, he is morally responsible for the wrong. I have made these obvious remarks for the better illustration of the general principle of liberty, and not because they are at all needed on the particular question, which, on the contrary, is usually discussed as if the interest of children was everything, and that of grown persons nothing.

Nowadays, people are often advised that they must plan as if a marriage won’t last. That is not costless. For example, there are many important forms of relationship-specific human capital–knowledge and skills that are valuable if one stays with one’s current spouse but would not carry over to the next spouse. Acting as if a relationship won’t last inhibits the accumulation of such relationship-specific human capital, which in turn can make the relationship more likely to break up, in at least a partially self-fulfilling prophecy.

It is quite awkward to talk about divorce, since speaking of divorce as a failure seems like speaking against one’s divorced friends. But a divorce is a failure–just as a bankruptcy is a failure. People often pick themselves up and achieve success after a business failure, but that doesn’t make a business failure a good thing in itself. Similarly, people often pick themselves up after a divorce and make a good life for themselves thereafter (sometimes involving a second marriage and sometimes not), but the divorce itself was not a good thing unless something else worse than a divorce happened or was revealed before the divorce.

Of people I know who have divorced, I definitely think many of them have made the right decision. Yet I wonder how often everyone’s knowledge that divorces are relatively common on the part of at least one of the two spouses helped make things go bad enough that they got to that point–either because someone made an incautious choice of mate because they knew they could get out of the marriage, because the acquisition of relationship-specific human capital was inadequate, or because feasible efforts to work things out didn’t seem worth the heroic efforts required.

I wrote one post of marriage advice on Valentine’s Day 2014: Marriage 101. I consider research on how to make marriages better and more stable extremely important.

It is said that two heads are better than one. Two hearts are also better than one. Marriage has the potential to bring human beings to a higher plane. But its ability to do so is severely compromised if people bail out too quickly. Among many other things, a spouse is a mirror, who helps us see ourselves more clearly–the ugly parts of our souls as well as the beautiful parts. Besides its many other practical consequences, bailing out too quickly from a marriage makes it much less likely that one will deal with the ugly parts of one’s soul.

Ben Thompson: Networked Robot Cars vs. Networked Carpooling →

The Stratechery post linked above is a very interesting additional twist to the discussion I bulletpointed on robot cars in my post “The Economist on the End of Cars as We Know Them” three days ago.

One other idea that is missing from “The Economist on the End of Cars as We Know Them” is the idea that to the extent people don’t own cars, but use a different car for each trip, it becomes much easier to electric cars. For certain trips, the short range of electric cars is a big problem, but for many trips, it is fine. And a robot-driven car can look for moments in its many peregrinations when it is close to a fast-charging station. (If a robot-driven electric car is in use a really high fraction of the time, then it will be hard to find a time to charge it that doesn’t have a serious opportunity cost. So there will be a premium on fast charging. But the fast-charging stations can be fairly widely spaced apart since the robot-driven car covers a lot of ground. This means that high-fixed-cost fast-charging stations will make sense.

Owen Nie: Maryland’s 1733 Monetary Helicopter Drop

Leonardo Da Vinci’s “aerial screw” helicopter is the only type of helicopter designed early enough to have delivered Maryland’s 1733 monetary injection.

I am pleased to host another guest post by University of Michigan graduate student Owen Nie on monetary history. Don’t miss Owen’s earlier guest posts:

- Playing Card Currency in French Canada

- Pre-Revolutionary Paper Money in Pennsylvania

- Monetary Policy in Colonial New York, New Jersey and Delaware.

This one is drawn from Richard Lester’s chapter “Social dividend in Maryland in 1733” in Monetary Experiments: Early American and Recent Scandinavian (New York: Augustus M. Kelley, 1970, pp. 142-151).

Maryland, for the first thirty years of the 18th century, had been using tobacco, their main product for exports to Britain, as currency and the value of it naturally varied with world price of tobacco. In 1733 a bill was passed for 90,000 pounds of paper money to be issued, 48,000 pounds of which was an outright gift to the inhabitants in order for the monetary expansion to take effect swiftly; the rest was introduced as loans. This helped avoid diverting resources from tobacco plantations and revived trade. It would have had a greater effect had paper money been declared legal tender before 1747.

Between 1733 and 1747 tobacco, coins and paper money coexisted as monetary standards. The state ordered that some tobacco be burned in 1733 to increase its price. In 1748 Maryland’s paper currency rose to par in terms of British sterling and from 1764 remained on par with gold and silver despite a sequence of issuances. Both as a business practice for the government and as a stimulus for the private sector, Maryland’s monetary expansion was a remarkable success considering its faithful redemption, maintenance of value all the way through 1776 and benefits to trade and industry.

The Economist on the End of Cars as We Know Them

{kind=link}

Google’s autonomous car. Image source.

On August 1, 2015, the Economist’s “The World If” column was titled “If Autonomous Vehicles Rule the World: From Horseless to Driverless.” Because I have had at the back of my mind the intention of writing a column on the coming transformation of automobiles, I could appreciate just what a wonderful article this is. I highly recommend it. Its thesis statement is:

… self-driving vehicles that can be summoned and dismissed at will could do more than make driving easier: they promise to overturn many industries and redefine urban life.

In bullet points, the support for this thesis statement is as follows (with a few comments of my own added in italics):

- Cars are expensive, but people use them only about 4% of the time. Google estimates that driverless cars that can be called at will might be in use as much as 75% of the time. Therefore, Stanford University computer scientist Sebastian Thrun predicts: “There will be fewer cars on the road—perhaps just 30% of the cars we have today.” Other estimates predict as few as 10% of the number of vehicles per person as now.

- Car makers will be selling mostly to commercially owned fleets, not individuals, and will be selling fewer cars than now.

- Car insurers will make less money as fewer cars, better driven, have fewer accidents. This possibility has been officially recognized by insurers in SEC filings.

- Fewer accidents also means fewer car parts will be sold.

- Robot taxis are a lot cheaper to use than human taxis–humans are expensive. Uber’s head Travis Kalanick said “When there is no other dude in the car, the cost of taking an Uber anywhere becomes cheaper than owning a vehicle.” Note also that without a driver, a robot taxi can be smaller. And it is easy to let people order the size they really need–a one-seater for simple trips; something bigger when they have luggage.

- Self-driving trucks will make trucking cheaper; they also will reduce demand for motels and restaurants along the road.

- An estimated 4.2 million car accidents and 21,100 deaths from car accidents will be avoided every year.

- “A study by the University of Texas estimates that 90% penetration of self-driving cars in America would be equivalent to a doubling of road capacity and would cut delays by 60% on motorways and 15% on suburban roads.”

- People will be able to get more done when they are in a car. (Some designs have people seated around a table.)

- Kids, senior citizens and the blind will gain independence. Parents will no longer spend such large chunks of time shuttling their kids to various classes, practices and other events.

- Much of the 24% of urban space devoted to parking will be available for repurposing. And most of the 30% of urban miles devoted to looking for a parking space can be saved.

- While the city centers can get denser without the need for so many parking spaces, the ability to sleep during one’s commute will also spur the growth of exurbs.

- Fear of driverless cars as dangerous has been much less than some have predicted. Indeed, some stuck behind them are already complaining that driverless cars drive too carefully and timidly. In the future, we may be (appropriately) afraid of having human drivers on public roads.

- Overall, the addition to growth and human welfare will be enormous if the technical challenges can be met.

- Boosting economic growth in the long-run typically requires making expensive things cheaper. And things are typically expensive because someone is earning money doing them. So making things cheaper inevitably means that some people will need to shift to other jobs from the jobs they are used to. But these adjustment costs are worth it for the benefits. It would be a big mistake to obstruct the transformation of cars.

Pope Francis: "A Change of Attitude towards Migrants and Refugees is Needed on the Part of Everyone" →

Thanks to Jonathan Portes for the link above.

Samantha Shelley: Why I'll Never Regret Being Mormon →

Linked above is an excellent post that says some things I haven’t managed to say very well in my posts on Mormonism, but have tried to circle around. You can see my attempts to make these kinds of points in these posts:

- The Message of Mormonism for Atheists Who Want to Stay Atheists

- How Conservative Mormon America Avoided the Fate of Conservative White America

- Inside Mormonism: The Home Teachers Come Over

- Will Mitt’s Mormonism Make Him a Supply-Side Liberal?

- The Mormon View of Jesus

- “Keep the Riffraff Out!” (–Not)

- Godless Religion

- Truth or Consequences

- “UU Visions”

- How Like a God!

- John Stuart Mill on Having a Day of Rest and Recreation

You might also be interested in these two guest posts about Mormonism appearing on this blog: