Michael Reddell: The Zero Lower Bound and Miles Kimball’s Visit to New Zealand

Michael Reddell has had a distinguished career in monetary policy making in New Zealand (as well as in Papua New Guinea and as an IMF appointee in Zambia). He recently retired from his job at the Reserve Bank of New Zealand and began a blog “Croaking Cassandra” about economic policy. (He also blogs about religion on his blog “Among Traditions.”)

I was delighted to get an email from him yesterday morning saying he had seen my talk at the New Zealand Treasury Friday, July 24 on the Economics of Happiness and would love to get together to talk about eliminating the zero lower bound. (I had spoken on Wednesday, July 22 at the Reserve Bank of New Zealand about eliminating the zero lower bound.) As it happened, I went to lunch a few hours later with both Michael Reddell and Carsten Schousboe (who is a Senior Health Economist at the Pharmaceutical Management Agency here in Wellington, the capital of New Zealand).

In his email introducing himself, Michael pointed me to this blog post, which he kindly agreed to let me mirror here. Here is what Michael had to say:

One of my persistent messages on my blog “Croaking Cassandra” has been that central banks and finance ministries need to be much more pro-active in dealing with the technological and regulatory issues that make the near-zero lower bound a binding constraint on how low policy interest rates can go, and hence on how much support monetary policy can provide in periods of excess capacity (and insufficient demand).

I’ve found it surprising that the central banks and governments of other advanced economies have not done more in this area. In most of these countries, policy interest rates have been at or near what they had treated as lower bounds since 2008/09. A few have been plumbing new depths in the last year or so, but half-heartedly (the negative rates have not applied to all balances at the central bank), and no one is confident that policy interest rates could be taken much below -50bps (or perhaps -75bps) without policy starting to become much less effective. The ability to convert to physical currency without limit is the constraint. There are holding costs to doing so, but for all except day-to-day transactions, the holding costs would be less than the cost of continuing to hold deposits once interest rates get materially negative. For asset managers and pension funds, for example, that shift would look attractive. I would certainly recommend that the Reserve Bank pension fund (of which I’m an elected trustee) transferred much of its short-term fixed income holdings into cash if the New Zealand OCR (Official Cash Rate) looked likely to be negative for any length of time.

I’ve been surprised by the lack of much urgency in grappling with this issue in other countries. I suspect there must have been a sentiment along the lines of “well, getting to zero was a surprise, and inconvenient, but we got through that recession, it is too late to do anything now, and before too long policy rates will be heading back up to more normal levels”. But they haven’t, despite false starts from several central banks. And each of these countries is exposed to the risk of a new recession, with little or no macroeconomic policy ammunition left in the arsenal. Interest rates can’t be cut, and the political limits to further fiscal stimulus are severe in most advanced countries.

If the rather sluggish reaction of other advanced country central banks (and finance ministries) is a surprise, the lack of any initiative by the New Zealand and Australian authorities is harder to excuse. Neither country hit the zero bound in 2008/09, or in the more recent slowdown (Australian policy rates are now at their lows, and commentators increasingly expect that New Zealand’s soon will be). The period since 2008/09 should have shown authorities that the zero lower bound is much more of a threat that most of us previously realised (not just, for example, a Japanese oddity). It should have suggested some serious contingency planning – as, for example, the Reserve Bank of New Zealand had done as part of whole of government preparedness for the possibility of a flu pandemic. Both countries have had years to get ready for the possibility of the zero lower bound. It is not as if the experience of the countries who have hit zero is exactly encouraging – slow and weak recoveries and lingering high unemployment.

But neither New Zealand nor Australia appears to have done anything about it. Indeed, in the most recent Reserve Bank of New Zealand Statement of Intent these issues don’t even rate a mention. I’m not suggesting it is the single most urgent or important issue the central banks face. Contingency planning never is, but that does not make doing it any less important. I’m also not suggesting that New Zealand is as badly placed as some – if we were to get to a zero OCR, our yield advantage would disappear and the exchange rate would probably be revisiting the lows last seen in 2000. And we have some more room for fiscal stimulus than some other countries. But no central bank or finance ministry should contemplate with equanimity the exhaustion of monetary policy ammunition. Nasty shocks are often worse than we allow for.

My prompt for this post is the visit to New Zealand this week of Miles Kimball, Professor of Economics at the University of Michigan (and an interesting blogger across a range of topics). Kimball has probably been the most active figure in exploring and promoting practical ways to deal with the regulatory constraints and administrative practices that make the ZLB a problem. They are all government choices. I’ve linked to some of his work previously. I noticed Kimball’s visit through a flyer for a guest lecture he is giving at Treasury on Friday, on a quite unrelated topic. I presume he will also be spending time at the Reserve Bank, addressing some of the monetary issues. This would seem like a good opportunity for some serious and enterprising journalist to get in touch with Kimball – whether directly, or via the Reserve Bank or Treasury – for an interview on some of his work in this area, and the reaction he is getting as he promotes his ideas, and practical solutions, around the world.

I’ve suggested previously that if our authorities are not willing to start on serious preparations to overcome the ZLB then the Minister should think much more seriously about raising the inflation target. I’d prefer to avoid a higher inflation target – indeed, in the long-run a target centred nearer zero would be good – but current inflation targets (here and abroad) were set before people really appreciated just how much of a constraint the zero lower bound could be. Better to act now so that in any future severe recession there is no question as to ability of the Reserve Bank to cut the OCR just as much as macroeconomic conditions warrant.

Here are some other previous posts where I have touched on ZLB issues:

- On the physical currency monopoly, and thus block to innovation, held by central banks

- On a sceptical speech on these issues by a senior Federal Reserve official

Aristotle's Eudaimonia

“Aristotle saw people not as striving to maximize a state of satisfaction, and also not as striving to perform a list of duties. He saw them, instead, as striving to achieve a life that included all the activities to which, on reflection, they decided to attach intrinsic value.”

– Martha Nussbaum, Cultivating Humanity: A Classical Defense of Reform in Liberal Education, pages 119-120.

John Stuart Mill’s Laffer Curve

When Maryland tried to tax the Second Bank of the United States, Daniel Webster argued before the Supreme Court in McCulloch v. Maryland that “An unlimited power to tax involves, necessarily, a power to destroy.” The Supreme Court echoed his words, saying “That the power to tax involves the power to destroy … [is] not to be denied.” John Stuart Mill addressed the same issue in paragraph 9 of On Liberty “Chapter V: Applications,” but came to a different rule: taxation must be limited to no higher than the revenue-maximizing rate–otherwise, it is clear that the intent of the taxation is to destroy rather than to raise revenue. He wrote:

A further question is, whether the State, while it permits, should nevertheless indirectly discourage conduct which it deems contrary to the best interests of the agent; whether, for example, it should take measures to render the means of drunkenness more costly, or add to the difficulty of procuring them by limiting the number of the places of sale. On this as on most other practical questions, many distinctions require to be made. To tax stimulants for the sole purpose of making them more difficult to be obtained, is a measure differing only in degree from their entire prohibition; and would be justifiable only if that were justifiable. Every increase of cost is a prohibition, to those whose means do not come up to the augmented price; and to those who do, it is a penalty laid on them for gratifying a particular taste. Their choice of pleasures, and their mode of expending their income, after satisfying their legal and moral obligations to the State and to individuals, are their own concern, and must rest with their own judgment. These considerations may seem at first sight to condemn the selection of stimulants as special subjects of taxation for purposes of revenue. But it must be remembered that taxation for fiscal purposes is absolutely inevitable; that in most countries it is necessary that a considerable part of that taxation should be indirect; that the State, therefore, cannot help imposing penalties, which to some persons may be prohibitory, on the use of some articles of consumption. It is hence the duty of the State to consider, in the imposition of taxes, what commodities the consumers can best spare; and à fortiori, to select in preference those of which it deems the use, beyond a very moderate quantity, to be positively injurious. Taxation, therefore, of stimulants, up to the point which produces the largest amount of revenue (supposing that the State needs all the revenue which it yields) is not only admissible, but to be approved of.

Even apart from the need for revenue, it has always seemed to me that within reason taxes were a gentler way of discouraging something, more consistent with freedom than ironclad rules. The changes in defaults and framing that go by the name of libertarian paternalism or soft paternalism seem even gentler and yet more consistent with freedom.

In the arena of encouraging actions to help the environment, I personally often find social disapproval to be a more onerous, less freedom-respecting means of getting compliance than a modest tax with the same overall effectiveness (and with rebates to maintain neutrality vis a vis the income distribution) would be. It uses up a lot of air time in social interactions for people to be guilting others into green actions that could be encouraged subtly in the background of life with an appropriate Pigou tax. Maybe it is just me, but I often bridle at someone telling me directly what to do, but don’t have any psychological resistance to responding to price signals, within reason.

“Scientific progress makes moral progress a necessity; for if man’s power is increased, the checks that restrain him from abusing it must be strengthened.”

– Madame de Staël, The Influence of Literature upon Society. Thanks to my brother Joseph for reminding me of this quotation.

Answering Adam Ozimek’s Skepticism about a US Sovereign Wealth Fund

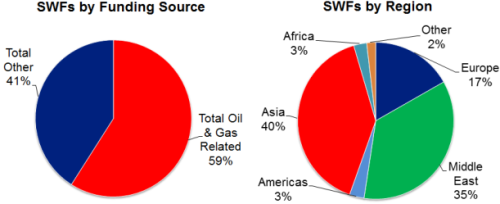

image source (2013)

In many blog posts and Quartz columns, I have argued that major economies such as the US should establish sovereign wealth funds even when issuing bonds is required to capitalize the funds. Sovereign wealth funds are already standard for countries that have positive net liquid assets. The new idea is to say that major countries that have negative net liquid assets should also have sovereign wealth funds as stabilization tools. A good post to turn to first for this is “Roger Farmer and Miles Kimball on the Value of Sovereign Wealth Funds for Economic Stabilization.”

In my tour of central banks to advocate eliminating the zero lower bound, I point out that even if monetary policy is someday done well enough to essentially keep the economy at the natural level of output all the time, there could still be a financial cycle. This possibility becomes clear if one writes down an entirely real general equilibrium noise trader model (as I have done in some very early stage research with Jing Zhang that might involve other coauthors before we are through). Even if the business cycle is entirely conquered in the sense of a zero output gap from sticky prices at all times, the financial cycle can cause welfare losses. Welfare losses can occur even when high enough equity requirements have taken away the implicit bailout subsidy for leverage. A contrarian sovereign wealth fund can help counteract the messed-up price signals caused by the noise traders.

In a July 19, 2015 post, “Skepticism About A U.S. Sovereign Wealth Fund,” Adam Ozimek worries about implementation difficulties for a sovereign wealth fund or other major economy. The first thing to say is that in general, institutions tend to be better in countries that–apart from natural resources–would be the richer ones, and so the right benchmark for the likely quality of a US sovereign wealth fund is Norway’s sovereign wealth fund rather than, say Saudi Arabia’s.

The second thing to say is that both Roger Farmer and I recommend a rule that the sovereign wealth fund is only allowed to invest in (low-fee) exchange traded funds. The importance of this is to keep the government from (a) micromanaging the investments and to keep the government from (b) voting the shares and micromanaging the behavior of the firms that way. In the US at least, if a sovereign wealth fund such as I recommend could ever be established, such aspects of the initial design of the fund can be maintained by the difficulty of getting changes opposed by one party through both Congress and a potential presidential veto. An initial bipartisan agreement on principles could not easily be broken.

The third thing to say is that I know in practice how to get the fund started off with a contrarian philosophy: I would recommend appointing John Campbell as the first head of the US Sovereign Wealth Fund.

On the objective of a sovereign wealth fund, the more I think about it, the more I realize that calculating the optimal policy for a large country’s sovereign wealth fund given a concern with overall social welfare in the usual way is a very interesting research problem. Basically, there is a technical answer to this question in the same sense that there is a technical answer for optimal monetary policy, after what I think is easier math than for optimal monetary policy.

The small country problem is, of course, even easier: a small country faces something much more akin to the standard portfolio problem, with the issue of what level of risk aversion to use when investing on behalf of a nation’s citizens. And of course, just as an individual household needs to integrate human capital into its portfolio decision, a small country sovereign wealth fund needs to integrate a wide variety of assets the country’s citizens and government already hold into its portfolio decision.

David Dreyer Lassen, Claus Thustrup Kreiner and Søren Leth-Petersen—Stimulus Policy: Why Not Let People Spend Their Own Money?

Note: This figure is from Kreiner, Lassen and Leth-Petersen (2014). It presents a local polynomial regression of the marginal propensity to spend the 2009 stimulus, which is collected by survey in January 2010, on the household marginal interest rate calculated from third party reported data with information about all individual deposit and loan accounts in 2007-2008. The regression is based on 5,055 observations.

Copenhagen was the third stop on my tour campaigning for the elimination of the zero lower bound. At the University of Copenhagen I also learned that the Danes were ahead of me on my “National Rainy Day Accounts” proposal. The Danes are showing the way toward technocratic stabilization policy for nations that share their monetary policy with other countries and sometimes need something more than the common monetary policy. (Denmark is not in the eurozone, but by long and hallowed custom has kept a fixed exchange rate relative to the mark and then the euro, so now it effectively shares its monetary policy with the eurozone.)

I am delighted to be able to host this guest post by David Dreyer Lassen, Claus Thustrup Kreiner and Søren Leth-Petersen on the Danish use of national rainy day accounts, based on their research:

How is it possible to stimulate the economy when traditional monetary and fiscal policy instruments are exhausted? Using an unprecedented policy tool the Danish government allowed people in 2009 to prematurely withdraw pension funds that were previously collected into individual accounts through a government mandate, thereby letting people spend their own money while leaving the government budget unaffected. Such a policy will have significant effects on spending if people are liquidity constrained. Evidence from a new study confirms this conjecture.

From 1998 to 2003 almost all Danes contributed 1% of their income to a mandatory pension plan, the so-called Special Pension (SP) savings plan. The funds were kept in individual, non-accessible accounts and were to be paid out starting at the public retirement age. Taking the entire population (as well as pundits and commentators) by surprise, on March 1, 2009 the government suddenly announced that the funds accumulated could be withdrawn during a window starting 1 June 2009 and ending 31 December 2009. The objective of the policy was to stimulate household spending.

The policy is interesting for several reasons: First, the Danish stimulus policy changed the timing of access to the individual funds while leaving individual wealth unaffected. Spending the pension funds today directly lowers consumption possibilities in the future. In this sense, the Danish stimulus policy implicitly imposed Ricardian equivalence at the micro level, and is thus almost ideal for measuring the importance of liquidity constraints for the spending response. Second, the payout was large. 70% of the population aged 25 or more had accounts. Almost 95% of all funds were taken out. The average individual payout amounted to approximately 1900 USD after taxes, and the total payout amounted to about 1.4% of GDP. Third, the policy was transparent and funds easy to access: All account holders received a personal letter stating the balance of the account. To have the balance paid out, account holders should sign a slip and return it in an enclosed, stamped envelope. The money would then be transferred directly to the holder’s main bank account, already on file. Finally, the policy was announced without any previous discussion in the public. This is important for measuring the effect of the policy because it makes it possible to bound the time frame where possible spending responses could be observed.

To measure the spending effect of the reform, we conducted a telephone survey in January 2010, just after the payout window had closed, resulting in about 5,000 completed interviews with information about spending behavior related to the SP-payout. The survey indicates that almost 65% of the respondents used the entire payout for increasing their spending, corresponding to almost 2% of total private spending in 2009.

To get further insight into whether this huge spending effect is driven by individuals affected by liquidity constraints, we match the survey data at the person level to income tax records and other administrative registers with information about household characteristics, income, and broad categories of financial assets for the period 1998-2009. In addition, we exploit a novel administrative data set that provides third party reported information about all individual deposit and loan accounts held by our survey respondents in 2007-2008. These data enable us to calculate account specific interest rates and, based on this, to estimate the interest rate on marginal liquidity for 2008 for each survey respondent and their household.

These household specific marginal interest rates represent a measure of the interest wedge between borrowing and lending rates, and is a continuous measure of the intensity of liquidity constraints. We correlate them with information about the propensity to spend the stimulus from the survey. The result is presented in the figure at the top of the post showing a strikingly linear and significant relationship between the propensity to spend the stimulus and the marginal interest rate.

The correlation is significant also when controlling for a number of covariates including income, financial asset holdings, demographics and expectations regarding future economic constraints, showing that the marginal interest rate is a robust predictor of the propensity to spend the stimulus. This suggests that credit market imperfections are important for explaining consumption responses to stimulus policies ̶ just as standard theory suggests.

Why do households face different interest rates? We use the longitudinal aspect of the administrative data and show that the level of financial assets held by the same households more than a decade earlier is negatively correlated with the marginal interest rate that we measure just before the stimulus. In other words, those individuals who held the least financial assets in 1998 face the highest marginal interest rates in 2008. Further, when we isolate the variation in marginal interest rates across households that is due to persistent differences in financial behavior, we find that the slope is five times steeper than the gradient illustrated in the figure, that is persistent differences in financial behavior impact the interest rate-spending gradient more than what appears from the raw correlation. This result holds up, and is actually reinforced, when we consider a subsample of individuals (about 50% of the original sample) who have never been unemployed during the last ten years before the stimulus. Overall, these results suggest that differences in liquidity constraint tightness across consumers, observed just before the stimulus policy implementation, reflect heterogeneity across consumers that is persistent to a degree that cannot be accounted for by shocks appearing within the horizon of a typical business cycle. The effectiveness of the policy thus appears to be rooted in persistent differences in financial behavior across households, although other factors, such as size effects, may also play a role.

The policy is remarkable in several respects. It leaves person level wealth unaffected and exploit differences in financial behavior across the population to generate spending effects that are significant at the macro economic level. Moreover, by letting people spend their own money, it has no direct effect on the fiscal budget, and may even have positive derived effects from increased activity. Thus, this type of policy may be a new way to stimulate depressed economies when standard fiscal policies are limited, for example because of high levels of sovereign debt.

This guest post is based on a research paper written by the three of us–Claus Thustrup Kreiner, David Dreyer Lassen, and Søren Leth-Petersen: “Liquidity Constraint Tightness and Consumer Responses to Fiscal Stimulus Policy.” The paper can be downloaded here.

Don’t miss the related posts:

- Getting the Biggest Bang for the Buck in Fiscal Policy

- National Rainy Day Accounts

- Joshua Hausman on Historical Evidence for What Federal Lines of Credit Would Do

- Joshua Hausman: More Historical Evidence for What Federal Lines of Credit Would Do

- How Italy and the UK Can Stimulate Their Economies Without Further Damaging Their Credit Ratings

- Preventing Recession-Fighting from Becoming a Political Football

- Noah Smith Joins My Debate with Paul Krugman: Debt, National Lines of Credit, and Politics

- After Crunching Reinhart and Rogoff’s Data, We Found No Evidence High Debt Slows Growth

(Note that as long as some decision makers think debt is a problem, it will lead to underuse of traditional fiscal policy, so that a national rainy day account policy is helpful in getting around fear of debt even in situations where national debt itself is not a problem.)

Live: The Message of Mormonism for Atheists Who Want to Stay Atheists

Note: You can see the written text for this sermon and some useful graphs and tables in my earlier post “The Message of Mormonism for Atheists Who Want to Stay Atheists.” Click on the picture above to see the video.

I made a false prediction when I gave this sermon on May 20, 2012, eight days before I inaugurated this blog: that I would avoid talking about religion on my blog once I started the blog. In the event for most of the time I have been blogging, I have had a religion post every other Sunday, alternating with philosophy posts on the other Sundays. They can all be found in my “Religion, Humanities and Science” sub-blog.

“Monotheism’s boast is that ultimate reality lives in its house and nowhere else. Monotheism’s sorrow is that everything must be accommodated in that one house.”

Everything You Think You Know about Disciplining Kids is Wrong →

Research is suggesting new approaches to helping kids behave. I would like to think that the claims here are true. But I think this research needs to be replicated by a skeptic.

Research in this area is crucial, since if behavior problems can be effectively dealt with, then a big argument people make to “Keep the Riffraff Out!” can be neutralized.

Nigeria Struggling to Be Free

The June 20th issue of the Economist had a special report on Nigeria. It is very illuminating. In particular, it illustrates what I meant in my July 3d Quartz column “An economist explains why the key to a free world lies with China” when I wrote about how ‘freedom from injustice, corruption, and abuse of power in your nation,’ is the key to ‘people having many options and possibilities in their lives and the freedom to choose among them.’

It also illustrates Daron Acemoglu and James Robinson’s claim in “Why Nations Fail” that injustice, corruption and abuse of power are what keeps most nations poor (in the sense of a low per capita GDP). Here is a nice summary of the Economist’s special report, from a page entitled “Buhari’s chances: Can he do it?”:

Despite these frequent disappointments, Nigeria remains hopeful, and for good reason. It does not require a miracle for its economy to grow at a consistent 7-8% a year. What it does need is better roads, rail connections and power lines. If the poorest states had the infrastructure to allow farmers to get their produce to market, it would open up the prospect of vast numbers of new jobs in farming and agricultural processing, giving young men an alternative to joining the jihadists or ethnic militias and lifting tens of millions of people out of poverty.

Yet the cure is not as simple as it sounds, for at the root of many of Nigeria’s problems are well-entrenched vested interests and pervasive corruption. If the country’s roads are crumbling, it is not for lack of competent engineers or money to repair them: it is because the money has been diverted to someone else’s pocket so that many of the engineers sit idle. If people pay more than they should for food, power and imported manufactures, it is not because Nigeria is inherently a high-cost economy: it is because politicians, officials and their friends in business have found nefarious ways to profit from shortages and waste. If large parts of the country are ruled by armed gangs, it is because so many of the state’s institutions, from local government to the national police and army, have been hollowed out by corruption.

“… it is always radical, in any society, to insist on the equal worth of all human beings, and people find all sorts of ways to avoid the claim of that ideal, much though they may pay it lip service. … We should defend this radical agenda as the only one worthy of our conception of democracy and worthy of guiding its future.”

– Martha Nussbaum, Cultivating Humanity: A Classical Defense of Reform in Liberal Education, p. 112 (end of chapter 3). (Before getting to this passage, I said something very similar in the live version of my sermon “The Message of Jesus for Nonsupernaturalists.”)

Effort vs. Innate Ability: What I Learned from Being in the Spelling Bee

I think you will like this 61-second video. (Just click on the picture above.)

It is closely related to my columns:

- There’s One Key Difference Between Kids Who Excel at Math and Those Who Don’t (with Noah Smith) and

- How to Turn Every Child into a “Math Person”

The principles there apply to more than math.

“…critics of soft paternalism should realize that people are already being nudged all the time, and not by government. The true masters of behavioral economics are marketers in the private sector. Marketers have been studying behavioral economics for ages, and have never had any compunction about using it to take your money.

Ever wonder why prices in stores are $9.99 instead of $10? Behavioral economics. How about sales and discounts? Just raise the base price and treat the real price as a discount, and behavioral economics will make people more eager to buy. That yogurt that advertises itself as fat-free? Check out how many grams of sugar it has. And so on.

Marketing is by far the biggest application of behavioral economics, it’s perfectly legal and it’s already everywhere. You are being nudged 24/7.”

– Noah Smith, in his Bloomberg View column “We’re All Smart. And Dumb. Sometimes.”

John Stuart Mill Worries about Money Corrupting Advocacy and Facilitation

John Stuart Mill is not always as libertarian as people think. After defending free speech vigorously in an earlier chapter, in paragraph 8 of On Liberty “Chapter V: Applications,” he defends the idea of driving vice underground if the people advocating and facilitating it are likely to be advocating and facilitating it primarily for the money. However, he makes an interesting distinction: if paid facilitation is necessary to enable people to pursue vice, it must be allowed. But if home-production is adequate to make the vice possible, then it is legitimate to make the market provision of facilitation illegal in order to drive it underground, where it will be less of a bad influence. Here is what he writes:

There is another question to which an answer must be found, consistent with the principles which have been laid down. In cases of personal conduct supposed to be blameable, but which respect for liberty precludes society from preventing or punishing, because the evil directly resulting falls wholly on the agent; what the agent is free to do, ought other persons to be equally free to counsel or instigate? This question is not free from difficulty. The case of a person who solicits another to do an act, is not strictly a case of self-regarding conduct. To give advice or offer inducements to any one, is a social act, and may, therefore, like actions in general which affect others, be supposed amenable to social control. But a little reflection corrects the first impression, by showing that if the case is not strictly within the definition of individual liberty, yet the reasons on which the principle of individual liberty is grounded, are applicable to it. If people must be allowed, in whatever concerns only themselves, to act as seems best to themselves at their own peril, they must equally be free to consult with one another about what is fit to be so done; to exchange opinions, and give and receive suggestions. Whatever it is permitted to do, it must be permitted to advise to do. The question is doubtful, only when the instigator derives a personal benefit from his advice; when he makes it his occupation, for subsistence or pecuniary gain, to promote what society and the State consider to be an evil. Then, indeed, a new element of complication is introduced; namely, the existence of classes of persons with an interest opposed to what is considered as the public weal, and whose mode of living is grounded on the counteraction of it. Ought this to be interfered with, or not? Fornication, for example, must be tolerated, and so must gambling; but should a person be free to be a pimp, or to keep a gambling-house? The case is one of those which lie on the exact boundary line between two principles, and it is not at once apparent to which of the two it properly belongs. There are arguments on both sides. On the side of toleration it may be said, that the fact of following anything as an occupation, and living or profiting by the practice of it, cannot make that criminal which would otherwise be admissible; that the act should either be consistently permitted or consistently prohibited; that if the principles which we have hitherto defended are true, society has no business, as society, to decide anything to be wrong which concerns only the individual; that it cannot go beyond dissuasion, and that one person should be as free to persuade, as another to dissuade. In opposition to this it may be contended, that although the public, or the State, are not warranted in authoritatively deciding, for purposes of repression or punishment, that such or such conduct affecting only the interests of the individual is good or bad, they are fully justified in assuming, if they regard it as bad, that its being so or not is at least a disputable question: That, this being supposed, they cannot be acting wrongly in endeavouring to exclude the influence of solicitations which are not disinterested, of instigators who cannot possibly be impartial—who have a direct personal interest on one side, and that side the one which the State believes to be wrong, and who confessedly promote it for personal objects only. There can surely, it may be urged, be nothing lost, no sacrifice of good, by so ordering matters that persons shall make their election, either wisely or foolishly, on their own prompting, as free as possible from the arts of persons who stimulate their inclinations for interested purposes of their own. Thus (it may be said) though the statutes respecting unlawful games are utterly indefensible—though all persons should be free to gamble in their own or each other’s houses, or in any place of meeting established by their own subscriptions, and open only to the members and their visitors—yet public gambling-houses should not be permitted. It is true that the prohibition is never effectual, and that, whatever amount of tyrannical power may be given to the police, gambling-houses can always be maintained under other pretences; but they may be compelled to conduct their operations with a certain degree of secrecy and mystery, so that nobody knows anything about them but those who seek them; and more than this, society ought not to aim at. There is considerable force in these arguments. I will not venture to decide whether they are sufficient to justify the moral anomaly of punishing the accessary, when the principal is (and must be) allowed to go free; of fining or imprisoning the procurer, but not the fornicator, the gambling-house keeper, but not the gambler. Still less ought the common operations of buying and selling to be interfered with on analogous grounds. Almost every article which is bought and sold may be used in excess, and the sellers have a pecuniary interest in encouraging that excess; but no argument can be founded on this, in favour, for instance, of the Maine Law; because the class of dealers in strong drinks, though interested in their abuse, are indispensably required for the sake of their legitimate use. The interest, however, of these dealers in promoting intemperance is a real evil, and justifies the State in imposing restrictions and requiring guarantees which, but for that justification, would be infringements of legitimate liberty.

John Stuart Mill’s emphasis in this passage on the corrupting influence of money makes me think about the debate over restrictions on campaign contributions. There, I do think that the distinction the Supreme Court has made between direct contributions to a candidate and “independent” expenditures makes some sense. But I might draw the line a little differently: as long as money will only help a candidate win an election, this seems important enough for free speech that it should probably be allowed. But if money is given into such direct control of the candidate that the candidate can turn it to personal use–including even moderate luxury on the campaign trail–the potential for corruption seems more severe and the argument for limiting things becomes greater. This is actually an argument for prohibiting campaign funds from being used for the candidate’s comfort rather than an argument for limiting contributions to a campaign fund. If such a restriction had the side-effect of discouraging people who like high levels of material comfort–that they can’t pay for out of their own pockets–from running for office, that might not be a bad thing.

“As regards literature, postmodernism recognizes no large, collective enterprise with a clear direction that all legitimate participants must respect. Though the history of interpretation is not cyclical, there is no reason why what has been done already in interpretation may not be done again if we find it rewarding. … The more innovation comes to seem mere variation, the more easily the old and neglected can become new again. There exists no historical imperative to be obeyed or disobeyed. Nothing must be done. Anything might be done. When the results are interesting, they are not interesting because they constitute ‘progress.’ Evidence coerces. Art merely seduces.”

– Jack Miles, in Christ: A Crisis in the Life of God, pp. 330-331