Purr Review Kitteh is Not Convinced by your Regression

Reblogged from econlolcats:

Everyone’s a critic. By MichaelH.

A Partisan Nonpartisan Blog: Cutting Through Confusion Since 2012

Reblogged from econlolcats:

Everyone’s a critic. By MichaelH.

“Stand up to your obstacles and do something about them. You will find that they haven’t half the strength you think they have.”

Link to Kevin Remisoski’s Twitter homepage and his LinkedIn page and an article in the local news (picture above)

In response to our column “There’s One Key Difference Between Kids Who Excel at Math and Those Who Don’t,” Noah Smith and I received many comments. Some of them gave good advice about teaching math to kids. Among those was this email from Kevin Remisoski, who graciously gave me permission to share this with you:

I liked most of the points you addressed in this article, however, I feel you missed one very important and crucial point. There are a good number of people who also have dyscalculia. This disorder is often times undiagnosed, and while some estimate that 5% of our population has this disorder, I would venture a guess that this in some form could likely affect as many as 20% of our population. Many of the symptoms seem fairly common to people I have helped with math over the years and my wife didn’t even know she had it until I gave her an assessment after she was complaining about how she always switched numbers around. This assessment went over 30 questions that are common symptoms of dyscalculia, and she answered 27 of them with yes.

I myself always excelled in math. This wasn’t due to parental drilling, flash cards, or anything of the sort. This was purely genetic, and this also seems to be the case with my stepson, though I’ve been teaching him more advanced techniques for his age as well as basic physics (he is 8).

I think somewhere along the way, teachers forgot how to teach math and left it to the text books and the curriculum to teach for them while they assist the book in the learning process. I’m sure this is most certainly due to laziness, but most human beings are lazy and just want to get home at the end of their work day. I know I struggled with some of my teachers in my youth, because countless times I’d approached them with easier ways of solving problems from basic math in elementary school all the way through college. I just don’t understand why some teachers are so focused on only teaching one solution to a problem.

You see the problem with dyscalculia, is that it is not impossible to teach math to people who suffer from this disorder. You just have to be creative, even if that means providing creative and abstract solutions at times. I have taught my wife quite a bit simply by using unorthodox approaches to math.

With all of that being said, in a base 10 number system, I feel that it is important that children understand a few basic concepts:

If A + B = C, then C – A = B, and C – B = A. I am not suggesting teaching 5 year olds the concept of substituting numbers with variables, but rather that they understand this concept as much as they will later be expected to memorize their multiplication tables. One exercise, I’ve worked on with my stepson is repetition. We don’t play with flash cards or have any visual representation, because I feel that defeats the purpose of memorization.

So, instead I would go with the range of numbers 0-9, and have him add and subtract different numbers within that range to see the relationships between those addends, sums, subtrahends, and difference. One way I went about this is as follows:

1+1, 1+2, 1+3……2+1, 2+2, 2+3…..3+1,3+2,3+3, and so on until each starting addend was added to zero through nine (despite starting with one in this example).

After I was sure he was comfortable with this, I would then have him add 1+2 for example and then 3-2, and 3-1. I would continue to have him solve addends, and then solve the difference from the sum when one of those addends was converted to a subtrahend, and then solve for the second one.

You see, I don’t believe in waiting for children to memorize addition and subtraction on their own. They should be able to look at any two numbers and solve either the sum or difference just as easily as they breathe.

The same can be said for multiplication when they are ready. They should not only write their multiplication tables out ten to twenty times a day until they have them committed to memory, but much like in my above example, they should understand the following:

If A * B = C, then C / A = B, and C / B = A.

This is the way to teach children math. I also firmly believe that until a child has memorized their multiplication tables at least through ten as well as committed addition and subtraction to memory, that they should not be allowed to even learn how to use a calculator. Genetic dispositions, as well as disorders, can be toppled by the human brain’s efficiency at memorization through repetition. If we are to believe that the day may come when no one will utter the words “I’m just not good at math.”, we also need to believe that there is a better way of instilling confidence in those young minds. Without the fundamentals of understanding the basic building blocks as I’ve described here, it’s really no wonder why so many children bomb in basic math much less algebra, geometry, trigonometry, and calculus. If Einstein could find a way to overcome dyscalculia, anyone can.

The link above is to the Japanese version. “International Finance: A Primer” in English can be found here.

When it is treated as anything more than a convenient simplification–or a solid starting place for thinking things through–one of the silliest conceits of economics is the idea that people never act against their own interests. Most often, people act against their own interests because cognitive limitations make it hard for them to figure out the right choice, even though strictly speaking, all the information they need to make an informed ex ante choice is in front of them. But sometimes, people’s psyches are riven by internal divisions. When someone’s soul is embroiled in a hammer-and-tongs civil war, it is natural and appropriate for others to want to weigh in on behalf of one side or another in that struggle. And sometimes, even when one side of an internal psychic division seems firmly in charge, others may want to foment regime change.

In On Liberty, Chapter IV, “Of the Limits to the Authority of Society over the Individual” paragraphs 3-4, John Stuart Mill lays down rules for such an intervention. In particular, he argues that punishment and strong social stigma should be off limits, but that other efforts to help people improve their lives are a good thing:

As soon as any part of a person’s conduct affects prejudicially the interests of others, society has jurisdiction over it, and the question whether the general welfare will or will not be promoted by interfering with it, becomes open to discussion. But there is no room for entertaining any such question when a person’s conduct affects the interests of no persons besides himself, or needs not affect them unless they like (all the persons concerned being of full age, and the ordinary amount of understanding). In all such cases there should be perfect freedom, legal and social, to do the action and stand the consequences. It would be a great misunderstanding of this doctrine to suppose that it is one of selfish indifference, which pretends that human beings have no business with each other’s conduct in life, and that they should not concern themselves about the well-doing or well-being of one another, unless their own interest is involved. Instead of any diminution, there is need of a great increase of disinterested exertion to promote the good of others. But disinterested benevolence can find other instruments to persuade people to their good, than whips and scourges, either of the literal or the metaphorical sort.

One big reason to limit efforts to change what seems like someone else’s self-destructive behavior to advice and preaching rather than punishing or stigmatizing is that one might be wrong. But another reason is that punishing and stigmatizing cause direct harm. For example, the many people in prison for drug use have lives that were already blighted by drugs now blighted by prison as well. Finally, punishing and stigmatizing may often be ineffective because the elements of a riven psyche one wants to encourage may have trouble seeing a punisher or stigmatizer as friendly.

The remarkable thing about this photo is how cocky I look. My cockiness when I was a teenager is also evident in the story I tell in my post “How the Idea that Intelligence is Genetic Distorted My Life—Even Though I Worked Hard Trying to Get Smarter Anyway.”

Here is the full text of my 50th Quartz column, “Odious Wealth: The Outrage is Not So Much Over Inequality but All the Dubious Ways the Rich Got Richer,” now brought home to supplysideliberal.com. It was first published on June 30, 2014. Links to all my other columns can be found here.

If you want to mirror the content of this post on another site, that is possible for a limited time if you read the legal notice at this link and include both a link to the original Quartz column and the following copyright notice:

© June 30, 2014: Miles Kimball, as first published on Quartz. Used by permission according to a temporary nonexclusive license expiring June 30, 2017. All rights reserved.

Concern about income inequality, and the even more striking inequality in wealth in the United States, is a key theme for the 2014 US congressional elections and has made Thomas Piketty’s book Capital in the Twenty-First Century a surprise bestseller. There are many reasons to be concerned about wealth inequality itself, regardless of the source of that inequality, but it is hard to pursue a discussion on the topic for long before someone makes a claim about whether the wealthy acquired their money in a deserving way. Partisans on the political left and right know which side of this argument they are supposed to emphasize: many who feel the government needs more revenue conveniently argue as if almost all wealth comes from underhanded, unscrupulous skullduggery, while many who feel the government needs less revenue conveniently argue as if almost all wealth were created by the likes of Steve Jobs, who brought us i-everything. But unlike these partisan stories, in every list of 1,500 or so billionaires, many deserve their wealth while others deserve very little of the wealth they have. While in some cases the principles for whether wealth is deserved or not are obvious, in other cases they are quite subtle.

To start with an easy category, wealth obtained by deceit is illegitimate. For example, given the way tobacco companies lied about the dangers of smoking,the gigantic legal judgments against them seem appropriate (though it is too bad how big a share of that money went into the pockets of lawyers). And although the magnitude of the crime might not be as great, GM’s recently outed behavior in hiding problems with ignition switches has a disturbing resonance with the earlier behavior of the tobacco companies. As these examples make clear, standard legal principles often make it possible to take away wealth obtained by deceit once that deceit is well established. But a greater hatred of deceit on the part of juries, judges, and legislators would help in further neutralizing this form of wealth.

If undeserved wealth always arose in cases where the logic was as simple as that for deceit, and were similarly reprehensible from a criminal or civil law point of view, then the issue of undeserved wealth could be appropriately handled in the courts. In an IMF paper, Harvard Economics professor Michael Kremer and Northwestern University Economics professor Seema Jayachandran make the intriguing proposal that debt incurred by a non-democratic government (after the appropriate international organization has declared that the debt is not in the interests of the people of a country) should be considered “odious debt” that later (and hopefully better) governments of that country need not pay back.

We could similarly talk about “odious wealth”—wealth that is hateful in its origin. But our instincts about the merits of different means of acquiring wealth often go astray. Let me take two extreme examples: old songs that people love and the kind of “vulture capitalism” whose reputation helped sink Mitt Romney’s chances in the 2012 presidential election.

There is currently a dispute over whether songs recorded before 1972 should continue to earn royalties. By naming their bill to extend royalties to pre-1972 recordings the “Respecting Senior Performers as Essential Cultural Treasures Act or “RESPECT” Act, congressmen George Holdings and John Coyners are using the fact that the musicians who recorded songs before 1972 (that we still listen to 42 years later) inspire feelings of gratitude, since songs of lasting popularity give many listeners much more pleasure than those listeners have paid for the right to listen to those songs. But the prospect of that very gratitude, plus 42 years of royalties, would have provided more than enough motivation for musicians to work hard back in 1971 to make great songs, if they had the ability.

Forty-two years is a long time. And money coming in the near future looks (and is) more valuable than money coming in the more distant future. And even songs that last typically get more play in their early years. So at the time a musician is working hard on a song, the prospect of 42 years of royalties and undying fame should, to a surprisingly close approximation, be just as motivating as, say, 80 years of royalties and undying fame. So we don’t need to extend royalties to pre-1972 recordings to bolster the confidence of musicians making songs now that they will be properly rewarded for their efforts. And on the downside, charging royalties for pre-1972 songs has the potential to inhibit the development of internet and satellite radio—and in particular how often people get to listen to the best pre-1972 songs on internet and satellite radio. So there is a lot of downside, not much upside to extending royalties to pre-1972 recordings. But the folks who would earn those royalties, if they are still alive, are attractive recipients of the money, even in cases where they are relatively wealthy.

By contrast, few ways of getting wealth seem less attractive than acquiring companies and then making them more profitable by laying off many of the employees. In August 29, 2012, Matt Taibbi wrote in the Rolling Stone essay “Greed and debt: the true story of Mitt Romney and Bain Capital:”

A man makes a $250 million fortune loading up companies with debt and then extracting million-dollar fees from those same companies, in exchange for the generous service of telling them who needs to be fired in order to finance the debt payments he saddled them with in the first place. …

Instead of building new companies from the ground up, we took out massive bank loans and used them to acquire existing firms, liquidating every asset in sight and leaving the target companies holding the note.

This is what I am calling “vulture capitalism.” But vultures have an important place in the ecosystem. Just like literal vultures, who help clear away dead carcasses, vulture capitalists help in the difficult process of moving workers from making and doing things that people don’t need as much anymore to making and doing things that people are eager to pay for. For example, Mitt Romney helped unwind K-B Toys, whose toys could no longer compete with video games. This was enormously painful for the employees of K-B Toys, who were ultimately sent on their way in an arduous transition to new jobs (and some to early retirement). But an enormous amount of good work has been accomplished by former employees of K-B Toys in new jobs with efforts that would have been squandered on trying to make unwanted toys if K-B Toys had been kept limping along for a few more years.

Since they are unlikely to get much gratitude from their brutal but useful work, vulture capitalists have to be rewarded with money. Otherwise, who would want to do that task of dismantling companies and letting go of people and other resources that should be devoted to other purposes?

None of this is to say that the incentives for vulture capitalism are precisely right. It is unfortunate when, as is too often the case, the efforts of highly trained professionals are focused on transactions that make sense only because of quirks of the tax law. But the basic idea that the old must sometimes be dismantled to provide the human and non-human building blocks for new things is sound. And if something that painful is going to happen, it sometimes makes sense to say as Jesus said to Judas: “What you are about to do, do quickly.” The wealth earned by vulture capitalists may then look like the 30 pieces of silver Judas was given for betraying Jesus, but it must be considered legitimate, nonetheless, because the job needs to be done.

There are two points to take away. First, it is not right to treat all large fortunes as odious wealth (or as otherwise illegitimate in origin) or to treat all large fortunes as beneficent wealth. Second, without careful analysis, our instincts will often lead us astray about which is which.

Although people complain a lot about wealth and income inequality, I suspect that a great deal of that anger comes from how the rich made their fortunes. An ideal version of capitalism—the version in the economic models taught in introductory economics classes around the world—would make it impossible to get rich without doing great good for society. There are certainly areas where doing great good for society is not understood and therefore not appreciated. But there are also many areas where the wrong things are rewarded because of market distortions, or where the government piles on rewards beyond those that are needed.

Among market distortions, lies and deception are a key category. But it is also a problem that the legal remedies available to deal with lies and deception are not matched by any ability to bring a legal tort claim for, say, raising the planet’s temperature by burning coal.

Among excessive rewards caused by the government, bailouts without increases in equity requirements big enough to prevent future bailouts are especially unfair. But actions by the government to protect the profits and business models of firms already in place by standing in the way of firms doing new things in new ways can in the long run be just as damaging. And in the digital age, copyright law is long overdue for reevaluation.

Wealth and income inequality are a topic of perennial fascination. But the heat has been turned up not only by increases in such inequality, but also by the feeling that the 2008 financial crisis and the Great Recession suggest that something is fundamentally wrong with our economic system. Among the many reasons to redesign the monetary plumbing of our economic system to avoid a repeat of the Great Recession, one of the most important is to help us gain clarity on the many long-run issues we face, of which economic inequality is one of the most difficult to deal with.

“In the 20th century, the development of bureaucracy had increased the potential power of the nation state enough that the Keynesian situations caused by the disabling of short-run monetary policy inherent in the gold standard made Fascism, Socialism and other variations on the theme of central planning look attractive to those who didn’t realize where it would lead.”

Image from Virginia Postrel’s Twitter Homepage

As an admirer of well-written nonfiction books and their authors, Virginia Postrel is someone who was famous to me before I ever started blogging. So I was delighted to have some interactions with her since I started blogging, especially on Twitter. One of the first interactions was when she said in the comments to Tyler Cowen’s post, “Reminiscences of Miles Kimball, and others” (near the bottom) that she wondered if I was dead, since as she later tweeted to me, Tyler’s post sounded a bit like an obituary.

It was nice to have Virginia say in that exchange she was glad I was not dead, but I was even more pleased to see her review-in-a-tweet of my post “Safe, Legal, Rare and Early.” She tweeted:

Safe, Legal, Rare and Early: Thoughtful & true post on abortion by @mileskimball

I am on the waiting list at the library for her latest book, The Power of Glamour, about which Tyler Cowen says:

Her best and most compelling book. It is wonderfully researched, very well written, the topic is understudied yet of universal import, and the accompanying visuals are striking.

Wikipedia currently says that Virginia “is an American political and cultural writer of broadly libertarian, or classical liberal, views.” But I am wondering if maybe she is at heart a Supply-Side Liberal.

On cultural issues, the dominant thread on this blog so far has been it focus on John Stuart Mill's On Liberty. (I give the links to relevant posts in “John Stuart Mill’s Brief for Freedom of Speech” and “John Stuart Mill’s Brief for Individuality.”) But there are also many other posts on my Religion, Humanities and Science sub-blog (linked at my sidebar) that address cultural issues.

By the way, I discussed the relationship between my own views and Libertarianism a bit in my “Libertarianism, a US Sovereign Wealth Fund, and I.”

Marjorie Balgooyen Drysdale is a classical soprano, music teacher, conductor, and the author of the book Tagalong Kid.

Not all of the emails Noah Smith and I received in response to our column “There’s One Key Difference Between Kids Who Excel at Math and Those Who Don’t” agreed with us. Some people said they had tried as hard as they could and still couldn’t do math. In a few cases, genuine dyscalculia might be at issue. But more often, I suspect the problem is with the quality of the math teaching. Elizabeth Green had a fascinating New York Times article “Why Do Americans Stink at Math?” a few days ago that pointed the finger squarely at the lack of adequate instruction for math teachers in how to teach math.

Marjorie Drysdale, who received a Master’s degree in Music from the University of Michigan, graciously agreed to share this email she made in response to Noah’s and my column. In addition to the issue of how math is taught, and where one is at when the math is taught, she points out that just because you can do something doesn’t mean you will love it. I agree. There are always tradeoffs in life, and time spent doing math is time away from doing something else that you may love more–maybe a lot more. But at least if you know how to do math, you can make the choice. And if math is taught well, what you learn will have some value for your life.

Dear Miles and Noah,

Regarding your essay, “There’s one key difference between kids who excel at math and those who don’t,” I have to disagree with your assertion that “For high school math, inborn talent is just much less important than hard work, preparation, and self-confidence.”

I was an excellent high school student. I worked hard, prepared, and was self-confident. I always made the high honor roll. I graduated 2nd in my class.

I went on to a competitive college and graduated with highest honors, phi beta kappa. I had two majors. I was always on the Dean’s List.

I went on to get a master’s degree and graduated with honors there, too. I became a professional musician. Supposedly, math and music go together. Not with me.

After geometry, I simply “didn’t get it." I took one more year of math—a course which, in the 60’s, was called "fusion." It was a combination of trigonometry and advanced geometry. That did me in. Until then, I had always earned A’s in math. I barely passed "fusion.”

It might have made a difference that I had skipped a grade and then was put into the “honors group”—an accelerated class. (In those days, classes were “tracked.”) In that class, we were taking courses a year ahead of our peers. Therefore, I was taking courses two years ahead of my peers. Perhaps I simply had a “readiness” problem.

I “hit a wall” and never went back to math. It had nothing to do with lack of effort, believe me.

Oddly, when I took my GRE exams after college and two years of work, my verbal and math scores were both in the 700’s. This truly surprised me. I hadn’t taken a math course in seven years.

I think that “readiness” in my case was more of a determining factor than “hard work.”

As I grew older, I understood it better, but I still didn’t like it. There are people who adore math. They light up about it. They enjoy it from the get-go. Therefore, I do think there is an innate element to these differences. Some people love math; others don’t.

I adore classical music. Most people couldn’t care less about it. The first time I heard it, I was hooked. That had nothing to do with hard work, either. Succeeding in it required hard work, of course, but the love came first.

I have been thinking more about the issues Noah Smith and I raised in our column “There’s One Key Difference Between Kids Who Excel at Math and Those Who Don’t.” So I asked permission to publish a few more of the comments Noah and I received by email. Here is a note I liked from Kate Owino:

I’d like to thank Quartz and Profs. Kimball and Smith for the wonderful article on math capabilities in kids released on October 27th, 2013. Reading it reminded me of my personal relationship with mathematics, as a subject and as a life/job-related skill.

I was born and raised in Kenya, and here the attitude toward math takes on a sexist connotation in favor of male students. It’s rare to hear of a female student saying that she excelled in math not only for the sake of passing the exams and getting into a good school or university, but also because she LOVES the subject.

From my personal experience, I was one of a handful of students in secondary school who fell in the latter category. This has proved (to date) to be a slight challenge whenever the topic of attitude towards math arises in a discussion with my female friends - they talk about how poorly they performed especially in secondary school, to the point where it comes across like they’re actually proud of the grades they got (Cs and below). I cannot contribute to the self-mockery because I got As all the way to my final exam…and the same applies to Chemistry.

Reading about the criticism-to-work-harder approach employed by students in China reminded me of my mother’s toughness towards my performance in math. From the age of 8 she would literally slap my wrists if I worked sloppily at a sum, and it was worsened by my teachers’ constant comments in my report book about my propensity to make careless mistakes.

As I look back now I cannot help but be proud of my love for math (and the sciences in general), even though I ended up pursuing a different academic path - studied literature in my undergraduate, and currently work in web content management. I hope to find a way to help do away with that sexist attitude in schools in my country especially since, as it was indicated in the article, poor attitude toward math makes many people lose out on critical life skills and lucrative career paths.

Thanks once again for the wonderful article. Have a wonderful week!

Newpapers.com is a great resource for things like this.

I tell the story of our Provo High School Forensics Team at the 1977 National Speech Tournament starting on page 2 of the storified tweets in “A More Personal Bio: My Early Tweets.” Here is the relevant newspaper article from 1977 to back up my story.

In the newspaper article, you can see my name at the top of the second column.

I am delighted to host another guest religion post by Noah Smith. Don’t miss Noah’s other religion posts on supplysideliberal.com:

Here is Noah:

The Pew Research Center recently did an interesting survey asking Americans how they felt about various religious groups.Here are the findings in a single table, shown above.

I was actually surprised by the low numbers across the board - there was almost no category in which more than 70% of people of one religion felt warmly toward people of another religion. But I wouldn’t put too much stock in that, actually - answers to these surveys usually tend to change a lot depending on how you phrase the question. The relative ratings are more interesting. Some of the findings are easily explained–the low ratings given to Muslims, for example are obviously an unfortunate result of the current political troubles with jihadist terrorist groups. But other findings are more surprising and intriguing. Here are some thoughts I had, looking at the numbers.

As many have noticed, Jews received the most positive ratings of any religious group in America. This confirms that American society is not in any meaningful way anti-Semitic, which is good news. But why do people like Jews so much?

Hypothesis 1: Nobody knows what Jews even are. When I was in high school in a medium-sized Texas town, another kid asked me about my religion. He asked: “Are you…Hanukkah?” So maybe people just have no idea what Judaism is, and figure it must be a minor thing that is no threat to their own faith.

Hypothesis 2: Jews are no threat. Jewish culture has a strong stigma against proselytization. I’ve criticized that insularity, but maybe it’s paying dividends. People don’t like threats - that’s why Japan and Germany are such popular countries these days. Judaism is not going to knock on your door and ask you if you’ve heard about Yahweh.

Hypothesis 3: The entertainment industry. There are lots of Jewish actors, comedians, etc. If you ask the average American to name someone Jewish, she’ll probably think of a funny guy like Jerry Seinfeld or a cute girl like Natalie Portman, or maybe a musician like Bob Dylan. If people knew that Drake, Scarlett Johansson, and James Franco were Jewish, they’d probably like us even more!

In addition, the two main drivers of anti-Semitism–European conspiracy theories and Muslim anger about Palestine–are both notably absent in America.

Mormons get middling low ratings in the poll. I guess this shouldn’t be surprising, given the prevalence of anti-Mormon discrimination in America. But what is the cause of the discrimination? David Smith, a political scientist at the University of Sydney (and no relation to Yours Truly, though we have clinked a few glasses over the years), finds that many Americans consider Mormons as an “outsider” group, which is strange considering that Mormonism is the only major religion to begin on American soil. Why do people see Mormons as outsiders?

Hypothesis 1: Proselytizing. One possibility is that the rapid spread of Mormonism poses a threat to other, more established religions. In this respect, Mormonism is the polar opposite of Judaism–every Mormon man must go out and convert people. That’s threatening, no matter how politely it’s done.

Hypothesis 2: The perception of secrecy. There is a perception of secrecy and exclusivity surrounding Mormonism. Anyone can go participate in any Jewish prayer service. But not even all Mormons can enter “dedicated” Mormon temples! Some Mormon weddings exclude non-Mormons. And there’s a perception that many other aspects of the religion are secret. Secrecy seems alien, and exclusivity is suspicious.

I think anti-Mormonism is a bad thing, but I don’t know how to combat it.

One interesting finding from the poll is that although 69% of Evangelical Christians expressed positive feelings toward Jews (one of the highest ratings given), only 28% of Jews expressed positive feelings toward Evangelical Christians (one of the lowest ratings given). This is weird, since Evangelical Christian sects - unlike, say, the Catholic Church - have no history of anti-Semitism or persecution of Jews. Also, the asymmetry itself is strange. Why don’t Jews like Evangelicals more?

What’s going on?

Hypothesis 1: Instinctive fear of dominant religion. Jews in Europe and the Mideast had a long history of being persecuted by whatever the dominant religious sect in the area happened to be - the Catholic Church, Islam, or the Eastern Orthodox Church. Jewish culture may have simply inherited an instinctive distrust of whatever the most powerful religious group seems to be.

Hypothesis 2: Politics. American Jews are generally liberal, while Evangelicals are generally conservative. In America, politics is often a stronger religion than actual religion. In addition, some Jews may be afraid that Evangelicals only like them because of a millenarian desire to see Israel recreated and then destroyed (in accordance with Biblical prophecy), or perhaps a cynical desire to use Israelis as expendable shock troops against the Muslims. This is probably not a motivating factor for most Evangelicals, but it does get some play in the media.

Hypothesis 3: Anxiety about the end of Judaism. Non-Orthodox Judaism is a dying religion. In America (and Britain), Jews are marrying non-Jews and ditching their ancestral religion at an astounding rate. It turns out that integration and assimilation destroys Judaism, while pogroms, ostracism, and oppression keep it going (someone might have bothered to mention this to Hitler!). Many Jews are naturally anxious about the end of their distinctive culture, and may tend to displace this anxiety by feeling bad about America’s “dominant” religion - Evangelical Christianity.

I think this attitude is a bad one. Evangelical Christianity is far more pro-Jewish than any other branch of Christianity has ever been. Furthermore, Evangelical Christianity has been an important factor in the creation of American society, the most philo-Semitic Western society in history. Jews should have a more positive view of Evangelicals.

Ökonomen wie Kenneth Rogoff oder Miles Kimball wollen das Bargeld abschaffen.

I made it into the German press for wanting to demote–not abolish–cash, along with Ken Rogoff, who does indeed want to get rid of cash. (i wrote about Ken Rogoff’s views here.) Google Translate works fine on this article. Thanks to Rudi Bachmann for letting me know about this article.

See what I have to say about breaking through the zero lower bound with electronic money in “How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide.” The article in the Süddeutsche Zeitung should have mentioned that I visited the European Central Bank and three of its associated national banks (France, Germany and Italy) to talk about how to keep paper currency from creating a zero lower bound.

The link above is to the Japanese version. “Will the ECB Go Negative?” in English can be found here.

Note: This post was the lead-up to my post “On the Great Recession.” After reading this one, I strongly recommend you take a look at that post.

Online, both in the blogs and on Twitter, I see a lot of confusion about the natural interest rate. I think the main source of confusion is that there is both a medium-run natural interest rate and a short-run natural interest rate. Let me define them:

Both the short-run and medium-run natural interest rates are distinct from actual interest rate, but in the short run, the short-run natural interest rate is much more closely linked to the actual interest rate than the medium-run natural interest rate is.

Introductory macroeconomics classes make heavy use of the concepts of the "short run” and the “long run.” To think clearly about economic fluctuations at a somewhat more advanced level, I find I need to use these four different time scales:

Obviously, this hierarchy of different time scales reflects my own views in many ways. And it is missing some crucial pieces of the puzzle. Most notably, I have left out entry and exit of firms from the adjustment processes I listed. I don’t know have fast that process takes place. It could be an important short-run adjustment process, or it could be primarily a medium-run adjustment process. Or it could be somewhere in between.

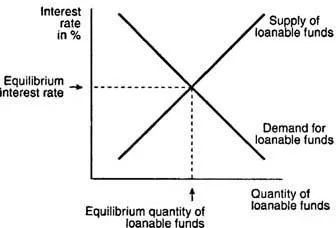

The importance of the medium-run natural interest rate is this: it is the place the economy will tend to once prices and wages have had a chance to adjust–as long as those prices and wages adjust fast enough that the capital stock won’t have changed much by the time that adjustment is basically complete. (I called that last assumption the “fast-price adjustment approximation” in my paper “The Quantitative Analytics of the Basic Neomonetarist Model”–the one paper where I had a chance to use the name of my brand of macroeconomics: Neomonetarism. See my post “The Neomonetarist Perspective” for more on Neomonetarism. The fast-price adjustment approximation is what makes good math out of the distinction between the short run and the medium run.) The medium-run natural interest rate is not a constant. Indeed, at the introductory macroeconomics level, the standard model of the market for loanable funds is a model of how the medium-run natural interest rate is determined. Here is the key graph for the market for loanable funds, from the Cliffsnotes article on “Capital, Loanable Funds, Interest Rate”:

A common mistake students make is to try to use the market for loanable funds graph to try to figure out what the interest rate will be in the short run. That doesn’t work well. Although technically possible, it would be confusing, since how far the economy is above or below the natural level of output has a big effect on both the supply and the demand for loanable funds that using the market for loan. To understand the short-run natural interest rate, it is much better to use a graph designed for that purpose–a graph that focuses on how the short-run natural interest rate is determined by the demand for capital to use in production and by monetary policy.

Above, I defined the short-run natural interest rate as the "rental rate of capital, net of depreciation,“ or "net rental rate,” for short. What does this mean?

Renting Capital. First, to understand what it means to rent capital, think of those ubiquitous office parks. If the capital a company or other firm needs is an office to work in, it can rent one in an office park like this:

In retail, the capital a firm needs to rent might be retail space in a strip mall:

If a firm is in construction or landscaping, the capital it needs might be a bulldozer, which it can rent from the Cat Rental Store, among other places.

Of course, sometimes a firm needs specialized machine that it has to buy, because those machines are hard to rent. In that case, let me treat it as two different firms: one that buys the specialized machine and puts it out for rent, and another firm that rents the machine. The same trick works for a specialized building that is hard to rent, such as a factory designed for a particular type of manufacturing. When firms that own buildings or machinery are short of cash, sometimes they separate themselves into exactly these two pieces, and sell the piece that owns the specialized buildings or machines so the other piece of the firm can get the cash from the sale of those buildings or machines, while still being able to use those buildings and machines by paying to rent them.

The (Gross) Rental Rate. I will call the gross rental rate simply “the rental rate." The rental rate is equal to the rent paid on a building or piece of equipment divided by the purchase price of that building or piece of equipment. Because this is one price (expressed for example in dollars per year) divided by another price (dollars per machine), the rental rate is a real rate–that is, it does not need to be adjusted for inflation. The rental rate is usually expressed in percent per year, meaning the percent of the purchase price that has to be paid every year in order to rent the machine.

The Net Rental Rate. It is useful to adjust the rental rate for depreciation, however. The paradigmatic case of depreciation is physical depreciation: a machine or building wearing out. More generally, a machine or building might become obsolete or start to look worse in comparison with newer machines. I am going to treat obsolescence as a form of depreciation. Obsolescence shows up in the price of new machines or buildings of that type falling relative to the prices of other goods in the economy. There are other things that can affect the prices of machines and buildings that will matter for the story below, but the rate of physical depreciation and the rate of obsolescence measured by declines in the real price of new machines and buildings of given types at the long-run trend rate are the two to subtract from the rental rate to get the net rental rate.

Physical investment is the creation of new capital–such as machines, buildings, software, etc.–that can be used as factors of production to help produce goods and services. Notice that I am using the phrase "physical investment” to distinguish what I am talking about from “financial investment.” So in this case, at some violence to the English language, I include writing new software in “physical investment."

The amount of physical investment is determined by the costs and benefits of creating new machines, buildings, software, etc. now instead of later. Say we are talking about whether to create or purchase a building or machine now, or a year from now. The benefit of creating a new building or machine a year earlier is the rent that building or machine could earn in that year. In the absence of capital and investment adjustment costs (to which I return below), the cost of creating a new building or machine a year earlier is

Dividing all of the costs and benefits by the amount paid to create or purchase the building or machine, the costs and benefits per dollar spent on the machine are

benefit relative to amount spent = rental rate

cost relative to amount spent = real interest rate + physical depreciation rate + obsolescence rate

The reason it is the real interest rate in the cost relative to amount spent is because the obsolescence rate is being measured in terms of a real price decline.

In the absence of capital and investment adjustment costs, the rule for physical investment is:

If I move the physical depreciation rate and the obsolescence rate to the other side of the comparison, I can say the same thing this way:

Or more concisely:

Finally, using the definition of the short-run natural interest rate as the net rental rate and flipping the order, I can describe the rule for investment this way:

Susanto Basu and I have a rough working paper on the determination of the short-run natural interest rate and about very-short-run movements of the actual interest rate in relation to the short-run natural interest rate:

"Investment Planning Costs and the Effects of Fiscal and Monetary Policy” by Susanto Basu and Miles Kimball.

We also have a set of slides to go along with the paper:

Slides for “Investment Planning Costs and the Effects of Fiscal and Monetary Policy” by Susanto Basu and Miles Kimball.

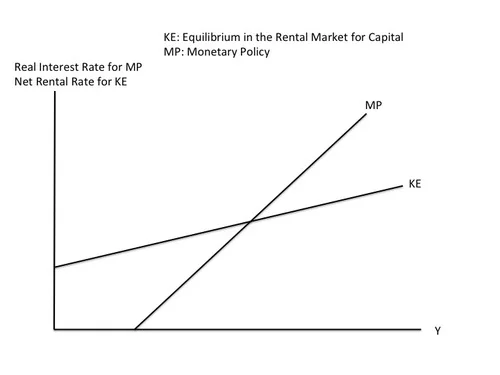

The short-run natural interest rate is determined by (a) equilibrium in the rental market for capital and (b) monetary policy.

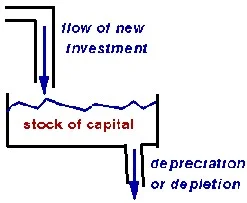

The Supply of Capital to Rent: The supply of capital to rent cannot change very fast. It takes time to create enough new machines, buildings, software, etc. through physical investment to affect the total amount of capital available to rent in any significant way. Wikipedia has an excellent article “Stock and flow” about this relationship between capital and physical investment. The canonical illustration is this picture of a bathtub:

Turning the tap on full blast might double the flow of water, but it will still take time for that flow to significantly affect the overall level of water in the tub. Similarly, turning investment on full blast may double the rate of physical investment creating new machines, buildings, software, etc., but it will still take time to significantly affect the overall amount of capital that exists in the form of machines, buildings, software, etc.

The Demand for Capital to Rent: The most important thing to understand about the demand for capital to rent is that it is higher in booms than in recessions. The more goods and services people want to buy, the more capital firms will want to rent at any given rental price in order to produce those goods and services. Ask any business person who has been involved in a decision to buy capital and they will tell you that they are more eager to get hold of capital to use when business is good than when business is bad.

The way I think of why the demand for capital to rent is higher in a boom than in a recession is this:

The math behind this story is in the Basu-Kimball paper “Investment Planning Costs and the Effects of Fiscal and Monetary Policy.” There, although it is not needed to get these results, for simplicity we use the fact that for Cobb-Douglas production functions, the ratio of how much a cost-minimizing firm spends on labor and on capital is fixed. (See the relatively hardcore post “The Shape of Production: Charles Cobb’s and Paul Douglas’s Boon to Economics.”) Using the letters

that means

RK = constant * WL.

Dividing both sides of this equation gives an equation for the rental rate:

R = constant * WL/K.

Since the total amount of capital K in the economy can’t change very fast, the total amount of capital in the typical firm also can’t change fast, so increases in wages W and total worker hours will push up the rental rate. And the net rental rate will parallel the overall gross rental rate very closely.

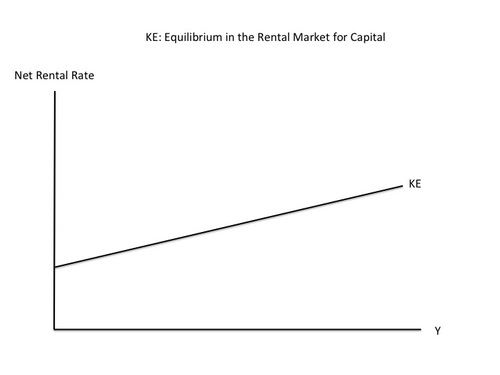

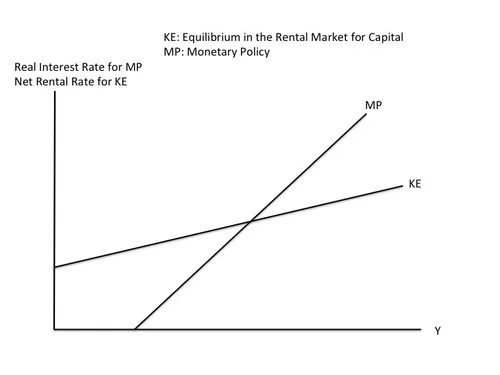

The KE Curve. With the supply of capital relatively fixed (or technically “quasi-fixed”) at any moment in time, a higher demand for capital means a higher equilibrium rental rate in the market for renting capital. How much a typical firm chooses to produce is closely related to how much output the economy as a whole produces. (Indeed, the amount firms produce must add up to the amount of output in the economy as a whole.) So the overall gross rental rate–and the net rental rate–will be increasing in the amount of output the economy as a whole produces. And of course, the amount of output the economy as a whole produces is GDP, for which we will use the single letter y. Thus, the graph below, which has GDP on the horizontal axis, and like the graph at the top of this post, shows an upward slope for the KE curve:

The KE Curve vs. the IS Curve. The IS curve has no microfoundations. The KE curve does. That is, I just explained where the KE curve comes from. The explanations of where the IS curve comes from are either incoherent, or really imply something very different from the IS curve taught in introductory and intermediate macroeconomics classes. Let me critique several ways people convince themselves the IS curve is OK. (Don’t worry if you haven’t heard of some of the interpretations I am critiquing.)

The MP Curve. Central banks periodically meet to determine the interest rate they will set. The rate they set is a nominal interest rate, where “nominal” just means it is the interest rate that non-economists think of. The real interest rate is the nominal interest rate minus expected inflation. Inflation expectations tend to change quite slowly and sluggishly, so the nominal interest rate the central bank chooses determines the real interest rate in the short run and the very short run. Central banks ordinarily raise their interest rate target when the economy is booming and lower it when the economy is in recession, so the interest rate (both nominal and real) will be upward sloping in output. Indeed, in order to make the economy stable, the central bank should make sure that the real interest rate goes up faster with output than the net rental rate does, so that, going from left to right, the MP curve showing how the central banks target interest rate depends on output cuts the KE curve from below, as shown in the complete KE-MP diagram:

In the KE-MP model, the intersection of the KE and MP curves is the short-run equilibrium of the economy. In short-run equilibrium, the real interest rate equals the net rental rate, or equivalently, the real interest rate equals the short-run natural interest rate.

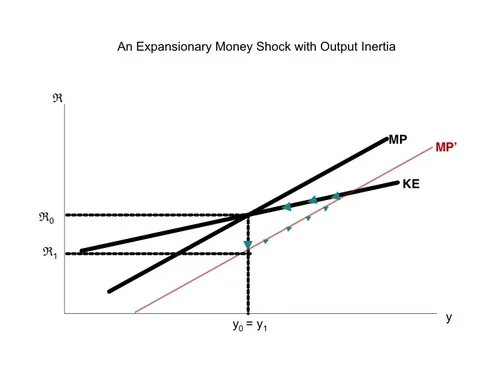

What brings the economy to short-run equilibrium is the adjustment of investment based on the gap between the net rental rate determined by the KE (capital rental market equilibrium) curve and the real interest rate determined by the MP (monetary policy) curve. But it takes time for firms to adjust their investment plans. Indeed, the level of investment is unlikely to adjust much faster than existing investment projects are completed and a new round of investment projects is started, as Susanto Basu and I discuss in “Investment Planning Costs and the Effects of Fiscal and Monetary Policy.” In the meanwhile, before investment has had time to full adjust, output can be away from its short-run equilibrium level, and the interest rate determined by the MP curve can be different from the net rental rate determined by the KE curve.

For example, suppose that the economy starts out in short-run equilibrium, but then the central bank decides to make a change in the interest rate change for some reason other than a change in the level of output. Since output is unchanged, the change in the interest rate corresponds in the KE-MP model to a shift in the MP curve. The graph below, taken from Slides for “Investment Planning Costs and the Effects of Fiscal and Monetary Policy,” shows the effects of a monetary expansion.

The movement up along the MP’ curve reflects the ultra-short-run adjustment of investment to get to the new short-run equilibrium–a process that might take about 9 months. The movement back along the unchanging KE curve reflects the short-run adjustment of prices to get back to the original (and almost unchanged) medium-run equilibrium. Since the real interest rate is on the axis, the point representing first ultra-short-run equilibrium, and then short-run equilibrium, is always on the MP curve. (The graph does not show the gradual shift of the MP curve back to return the economy to the medium-run equilibrium. One way for that adjustment of the MP curve to happen is if there is some nominal anchor in the monetary policy rule so that the level of prices matters for monetary policy, not just the rate of change of prices.)

I was interested in the news about the US Math Team (of high school students) this year because I was asked to be an alternate to the US Math Team in 1977, the end of my senior year in high school. I tell that story here, in a set of storified tweets that I link at my sidebar:

{kind=link}