So What If We Don't Change at All…and Something Magical Just Happens?

A tweet with this cartoon reminded me of my post “The Unavoidability of Faith.” I believe that one of the first decisions one must make before putting forth effort is whether efforts are likely to make one’s life better. Since thinking hard is itself effort, there is no way the decision of whether beginning to make an effort at life-improvement has a high enough marginal product to be worthwhile can be made in a fully rational way. It takes faith. If you believe that making an effort at life-improvement is worthwhile (and perhaps by the actions that result, get some confirmation), expressing that faith to others who are just starting out might make a big difference in their lives.

Of course, there are many other things one might have faith in, instead: for example, the idea that even without any effort, everything might work out well because of something magical. What a pleasant belief! But will it work?

Max Huppertz—The Decline in Labor Force Participation: Speed Bump, Hysteresis, or "I, Robot"?

Max Huppertz is a student in my “Monetary and Financial Theory” class and has his own Tumblr blog, Liberal Animation. Of all my current students, Max is the one whose writing reminds me most of Noah Smith’s style on Noahpinion. To get a full picture of Max’s sense of humor, you will have to go to his blog Liberal Animation, but the guest post below shows the depth of Max’s analysis. Max:

Evan Soltas had an interesting post about labor market tightness a couple of weeks ago. His main point is that, looking at the quits rate, you might think that labor markets are pretty tight right now. That might be a sign that, overall, there’s not a lot of unused economic capacity, or at least, not a lot of unused capacity that matters (more on that below). If you think that’s the case, you’d reach very different policy conclusions when it comes to monetary tightening than someone who thinks there’s still plenty of slack in the economy.

Quite a few people have given their 2 cents already. John Aziz makes a point about the potential benefits of overshooting: it might create jobs for some of the long-term unemployed.

Evan may have a good reason for disregarding the long-term unemployed. John’s proposal might be all we need. But if neither of the two is completely right, we may be in trouble.

Why does Evan think that the long-term unemployed don’t matter? He says that if they don’t compete with more active members of the labor force, they can’t hold back wage growth or interfere with employer/employee matching (because they won’t keep people from quitting a job they don’t like for one they enjoy). Which is a valid point.

But in the medium to long run, a drop in lower labor force participation seems like somewhat of an issue. And participation is down:

It seems to me that there are three possible reasons for this, and three scenarios how this could play out:

- The decrease in labor force participation is transitory. In that case Evan’s assessment is correct, although you could still argue that the possibility to overshoot is a risk worth taking, given its potential benefits.

- The decrease is more or less permanent, due to labor market hysteresis. In that case, overshooting alone might do the trick.

- The decrease is more or less permanent, and it’s a (labor!) demand trend. In that case, we might have a real issue on our hands.

1) Will it all be over soon?

Evan seems pretty convinced that the long-term unemployed “really can’t matter much in a macroeconomic sense”. I think that statement makes sense only if you assume that, in the long run, labor force participation will return to its pre-crisis level. Else, I would like to see an argument as to why we should ignore the fact that 3% of the total US labor force decided to take some time off. Changes of that magnitude are the ones that tend to matter little now, but a lot if they turn out to be persistent over several years’ time.

2) The UI forever (well, kinda…)

Just so we’re clear: economists have a somewhat peculiar interpretation of the word permanent. When I say that the drop in labor force participation might be permanent, I don’t really mean forever. I mean, “for around ten years or so”. Which is substantially longer than recovering from the recent crisis will take (hopefully, anyway), and thus covers a much longer time span than scenario one. So why might participation be depressed for a whole decade?

There are a few stories you could tell that might lead to scenario two. Maybe people lost a lot of human capital while they were unemployed, and have genuine trouble finding a job. Or maybe, employers regard long-term unemployment as a signal. Long-term unemployment might indicate that you’re not the kind of person people would want to employ. Granted, it might also mean you were just unlucky and got laid off at a time when it was really hard to find a new job. But so long as employers have plenty of ‘good’ applicants to choose from – people who aren’t sending out the long-term unemployment signal – they might be okay with rejecting you anyway.

I’m not sure how likely this scenario is, but if this is the one we’re in, definitely overshoot! Temporarily overheating the economy may raise inflation a little, but it would also mean more job openings and fewer people applying. Making job applicants scarce would provide an incentive for employers to take a closer look at the long-term unemployed, and to figure out whether what happened to them was just bad luck – or whether they’re actually bad apples.

What if the long run equilibrium level of employment is actually decreasing over time? Take a look at the bigger picture:

For a while now, there has been stagnation and quite a substantial drop in labor force participation, even before the dot-com bubble. If employers desperately needed these people, wouldn’t you expect them to raise wages and try to lure some of them back into the game?

I know this sounds a little like a sci-fi cliché, but if falling demand for labor due to increased mechanization were responsible for discouraging workers from even trying to find a job, overshooting will at best give a temporary boost to labor force participation. After that, we’re back to the downward trend.

The remedies for this kind of situation are very different from what we need to do in the other two cases. Increasing the general level of education would be a good idea (it generally is, but especially in this case).

Rethinking the social safety net would be another (this is probably worthy of a post of its own, but let me give you my intuition). Many of the labor-intensive industries of today might rethink their business model once robots become more cost-effective. What happens if mechanization puts us into a position where the vast majority of workers in classic manufacturing jobs (cars, steel) – and possibly also a fair few in the service sector (eventually, burger-flipping robots will be the norm) – are no longer needed? And when, at the same time, the new ‘employees’ – machines – won’t ever ask for pensions, or unemployment benefits? Well, it seems to me that indefinite unemployment insurance, or a guaranteed basic income, might not be so Utopian in this scenario.

Faced with this kind of affluence, society might well decide that the dangers of ‘paying people to be unemployed‘ are far outweighed by the benefits of getting much closer to what John Rawls would call a well-ordered society. And, especially in a highly educated society, I think we have reason to believe that people actually want to work, instead of being on the dole. As Jeffrey Smith nicely said (referring to Arno Duebel, a German who had been living off unemployment benefits for 36 years straight):

The actual mystery, though, is not the existence of someone like Arno, but rather, given the relative generosity of many European welfare states, their relative scarcity.

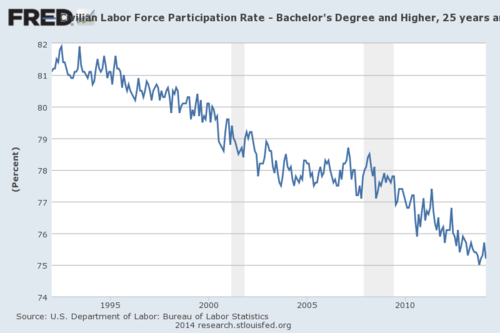

By the way, labor force participation isn’t just down for low-skill workers; this may be an issue that affects us all, even those with a college education (albeit to a lesser degree):

Like I said, this deserves a post of its own.

Humans good, robots bad?

I think that the third scenario is the one we want to be in. Any kind of job that a robot (or machine in general) can do better then a human – why not let it do it?

But it’s also the most difficult one to come to terms with, politically and ideologically. The left would need to give up part of its struggle for the ‘working class’, at least in the classical meaning of the word – factory workers, hard manual labor, that kind of thing. The right, on the other hand, might need to concede that in this kind of environment, maybe having a basic income won’t annihilate the US economy.

Issues like these would have to be dealt with during the next few years and decades. Or, who knows, maybe we are in scenario one, and Evan is right, or two, and John is right. But if not – and there are good reasons to believe this – we might want to start thinking about the implications.

Robert Flood and Miles Kimball on the Status of the Efficient Markets Theory

Robert Flood is an economist famous for his study of asset bubbles. Links to many of his papers can be found here.

My post “Robert Shiller: Against the Efficient Markets Theory” started a lively discussion on my Facebook wall (which is totally public). I added my discussion with Dennis Wolfe and a summing up by Richard Manning to “Robert Shiller: Against the Efficient Markets Theory” itself, but I thought the discussion with Robert Flood deserved its own post. See what you think:

Robert: This stuff is fun to talk about without a model, but finding one that works so you can use it for testing is harder. The stuff without a model says nothing about data so is nice for talk shows.

Miles: Any model we would write down at this point would be drastically wrong, so it would not be of much immediate practical value. What we need first is a suite of survey and experimental tools for measuring all the narrative forces that Bob Shiller is talking about.

Robert: As I have said, this is fun stuff. I just wish you’d get past the Efficient Markets thing. It’s undefined w/o a model and you do not want to talk about models - neither do I. The “stories organizing” notion is as good as anything else. I look forward to seeing where it goes. John Cochrane aside, the SDF approach looks like a dead end to me. It’s killing Macro and does not seem to do much for Finance.

Miles: There is no lack of efficient markets theory models that describe the way the world isn’t. Take your pick. In class today, I talked about the no-trade theorems, for example. In the real world, 95% of all trading volume cannot be explained if you insist that everyone has the same expectations.

Robert: Now you are talking. The issue you mention is a problem with Rep Agent - RA - not with EM. Indeed, having problems with RA gives an immediate research strategy - no RA - information dispersion, taste dispersion, life span dispersion, information discovery, transactions costs, rules of thumb….. In my view EM is not a hypothesis, it is an assumption about how people behave and not just in financial markets.

Miles: None of information dispersion, taste dispersion, life span dispersion, information discovery, transactions costs can possibly explain the volume we see. Only different people processing the available information differently can possibly yield the volume we see. Of your list, only “rules of thumb” is in this category, but in reality there are many people very actively processing the same information in different ways to come to different opinions. That is a failure of rational expectations. Without rational expectations, there is no efficient markets theory left, since the EMT logic runs from (approximately?) perfect competition in asset markets and (approximately?) rational expectations.

Robert: Agreed, volume is a real issue. I think it has something to do with the way we have structured compensation. Why is different processing of information a RE failure? People have very different experiences, different abilities and therefore different costs and therefore process things differently. The only failure is the failure by definition of RA. Forget econ for a moment. Look at politics. The dispersion of beliefs is, I think, much wider than the dispersion of information.

Miles: The assumption of rational expectations is the assumption of perfect information processing, given the information you have in front of you. There was a time half a century ago when economists thought that imperfect information and imperfect information processing were similar issues, but technical advances have made it clear that imperfect information can be dealt with by nice extensions of standard theory. Not so for imperfect information processing. Methodologically, that is a radical departure from standard theory, though a necessary one for many applications, since people in the real world are not infinitely intelligent and many real-world economic decisions are quite difficult computationally and conceptually–difficult enough to tax the abilities even of PhD economists, let alone people who don’t love solving optimization problems. I raised some of these issues in my post “The Unavoidability of Faith.”

Robert: Sure. The Muth model, Lucas, Sargent, Sharp etc had free relevant information - including full information about the model generating outcomes and costless processing. So what? Expand the framework to include all sorts of costs and you have a bigger model, but that does not make people behave stupidly. The guys in the model will use their history (goodby Markov) to process things until they think (Bayes comes in here) it’s not worth processing more. (Oddly, this is Peter Garber’s completely incomprehensible thesis written under Lucas)

Miles: I agree that people do not generally behave stupidly. My point is that to this day, our standard technical tools depend crucially on them being infinitely intelligent. There is a reason Peter Garber’s thesis was not easy to understand. Dealing with imperfect information *processing* is a *much* bigger technical leap than dealing with imperfect information. This is one of the themes of my paper “Cognitive Economics” that I am giving as the keynote speech at the Japanese Economic Review Conference in Tokyo in August.

Robert:Ok. I am happy to agree on the NSS way of thinking ( NSS = Not So Stupid). In my view, that’s all EM or RE says. Remember where we came from - no expectations, static expectations, adaptive expectations.

Update:Willem Buiter writes on the Facebook version of this post:

Willem H. Buiter:Efficient Markets Theory is an obvious empirical failure. Unfortunately, the alternative is a swamp of mutually contradictory but non-refutable (i.e non-scientific - long live Popper) anecdotes.

John Cochrane: Gene Fama's Efficient Markets Theory and Empirical Methods Thread Through All of Empirical Finance →

John Cochrane’s post “Gene Fama’s Nobel” is a wonderful summary of Efficient Markets Theory and of empirical results in finance.

Pranav Krishnan: Fighting European Deflation with Negative Interest Rates

Pranav Krishnan is a student in my my “Monetary and Financial Theory” class. Pranav also has a blog that focuses on the finances of European football. Here is what Pranav has to say about eurozone monetary policy:

There were some positive signs around Europe, where it appeared that Spain’s unemployment rate had bottomed out in late 2013.

Perhaps talk of Europe’s recovery has come a little too early. While there were signs of positive growth in countries like Spain and Italy over the past few months, inflation was very low, and even more so inflation expectations. David Roman of the Wall Street Journal wrote about a significant deflationary risk in Europe and how officials are expecting the European Central Bank to take the appropriate measures necessary to stem the tide. Josef Makuch, Slovenian Central Bank governor-rightly-feels that deflation could cause even more problems in the long term.

“Several [ECB] policy makers are ready to adopt nonstandard measures to prevent slipping into a deflationary environment,”

It appears that there might be more to this issue, than simply highlighting the risk of deflation. The article was largely skimming the surface of what could become a wider problem later on. Demosthenes Tambakis, a professor at the University of Cambridge, wrote for The Economist, outlining his opinion on why the Eurozone is at risk for deflation in further detail, He points to very low inflation expectations across Europe and that alone increases a risk in deflation. While he admitted that this risk shouldn’t rise so dramatically based on expectations alone, he does point out a few other institutional design elements that could contribute; Most notably, the European Central bank’s mandate, and the Zero Lower Bound.

The European Central Bank mandate is a bit pedantic in terms of legislature but it can play a role in the eyes of most economists. The ECB, cites Tambakis, is committed to just below 2%, in contrast to say the Fed who wants to maintain a 2% average over time. Tambakis believes that this causes an asymmetry which assures everyone that while they do not have to fear runaway inflation, they should worry when prices are too low because the ECB by design would be more reluctant to embark on expansionary monetary policy (increasing the money supply) than they are to contract. While this point could make some sense in that the ECB might be unintentionally ‘guiding’ people to expecting less inflation in the medium-run and long-run, I would be surprised if this had a serious impact on inflation expectations. Given the low levels of inflation in Europe, most economists and investors would likely expect lower levels to continue especially with the reduction in German growth rates.

The more likely argument seems to be the one about the Zero Lower Bound. These risks are determined by the Shiller Index which predicts the long-run frequency of international stock market crashes. Europe has faced two issues, in that they’ve suffered from the original financial crisis of 2008 and then the individual debt issues that each country faces. So, the natural reaction would be to cut interest rates to stimulate demand, but the Zero Lower Bound in Europe threatens to create a liquidity trap for the Eurozone. In tandem with the dual mandate language set by the ECB, everyone already has very low expectations of inflation and the inability for countries to set monetary policy and stimulate demand individually threatens to worsen the situation for the Eurozone as a whole.

While there could be some legislation to create a more unified Europe fiscally and financially, the best thing the ECB can hope to do now is if they are going to be rigid about keeping inflation below 2% they should be more flexible about the Zero Lower Bound and allow the interest rate to hover in a broader range of negative interest rates. The process will be rather painful because inflation expectations could plummet but in the long term, Europe could be better for it and escape the dangers of a long-term liquidity trap.

Robert Shiller: Against the Efficient Markets Theory

On March 26, David Wessel published a very interesting interview with Bob Shiller, “Robert Shiller’s Nobel Knowledge.” This interview gives a reasoned critique of the Efficient Markets Theory.

Ideal Informavores or Lovers of a Good Yarn? To begin with, Bob questions whether it is a reasonable approximation to assume that people acquire information avidly and process that information perfectly:

The story about bubbles was that the markets appear random, but that’s only because markets respond to new information and new information is always unpredictable. It seemed to be almost like a mythology to me. The idea that people are so optimizing, so calculating and so ready to update their information, that’s true of maybe a tiny fraction of 1 percent of people. It’s not going to explain the whole market.

Instead, Bob argues that human beings are avid consumers and tellers of stories:

Psychologists have argued there is a narrative basis for much of the human thought process, that the human mind can store facts around narratives, stories with a beginning and an end that have an emotional resonance. You can still memorize numbers, of course, but you need stories. For example, the financial markets generate tons of numbers—dividends, prices, etc.—but they don’t mean anything to us. We need either a story or a theory, but stories come first.

Can You Earn Supernormal Returns? A failure of Efficient Markets Theory suggests that there should be some way to obtain above-normal returns. But Bob cautions that believing that you personally can earn above-normal returns in the stock market is a little like believing one can win American Idol: definitely true for someone, not likely to be true for you:

The question is often whether it’s possible for anyone to pick stocks, and I think it is. It’s a competitive game. It’s like some people can play in a chess tournament really well, but I’m not recommending you go into a chess tournament if you are not trained in that, or you will lose. So for most people, trying to pick among major investments might be a mistake because it’s an overpopulated market. It’s hard. You have to be realistic about how savvy you are.

By contrast, if you want to try your hand at investing in a market where you have less competition as an investor, you have a better chance, with a lot of hard work:

But if you are thinking about buying real estate and renting it out, fixing it up and selling it, that’s the kind of market that’s less populated by experts. And for someone who knows the town, that’s doing business, I’m not going to tell someone not to do that.

Can Bob Shiller Earn Supernormal Returns? Bob does think that he can pick stocks. The key for him is to pick boring stocks:

Well, I actually think I’m smart enough to pick winners. I’ve always believed in value investing. Some stocks just get talked about, and people pay all sorts of attention to them, and everyone wants to invest in them, and they bid the price up and they are no longer a good buy. Other stocks, they are boring. There is no news about them—they are making toilet paper or something like that—and their price gets too low. So as a matter of routine, you buy low-priced stocks and sell high-priced stocks.

I think of “pick boring stocks that have a present value that can be easily calculated” (and of course only those that are undervalued according to that calculation) as Warren Buffett’s strategy as well.

Can You Succeed at Contrarian Market Timing? The one thing I would add here to what Bob says is this about market timing. Some of Bob’s work, some of it joint with John Campbell, suggests that contrarian market-timing can be a good idea. In particular, their work suggests increasing one’s stock holdings when the price/dividend ratio is low and reducing one’s stock holdings when the price/dividend ratio is high. (Bob has also used the ratio of price to cyclically adjusted earnings or smoothed earnings as a way of gauging if the market is high and likely to fall or low and likely to rise.) I believe this works and try to do it myself. But it is hard to do without a contrarian personality. What makes the market too high is that some story is making people optimistic about the market–a story that is likely to infect you as well; what makes the market too low is that some story is making people pessimistic about the market–again a story likely to infect you as well. So doing any market timing subjects you to the danger of succumbing to the stories out there that, because most other people are succumbing to them at the same time, will make you likely to buy high and sell low. It is only if you naturally like stories other people don’t like and dislike stories that they like that you can be a contrarian investor without great intellectual and emotional self-discipline.

Update: There were many great comments on the Facebook version of this post. The discussion with Robert Flood I am making into the post for Friday, April 18. Let me put the key elements of my discussion with Dennis Wolfe and Richard Manning here:

Dennis Wolfe: Miles – enjoyed both your post on Saturday and this one – and I tend to believe both, especially Shiller’s points. Have you seen the whitepaper “Capital Idea: The active advantage can help investors pursue better outcomes”? The paper was published late last year by The American Funds to make a their case for active investing over passive investing. Their paper presents strong evidence that some investment managers have a proven model and track record of persistent above average results over rolling periods of time. John Rekenthaler (The Rekenthaler Report), a researcher at Morningstar, published results of a similar study last summer comparing American Funds with Vanguard index funds (The Wrong Side of History; The Horse Race) with similar conclusions. After considering Shiller’s thoughts and the evidence outlined by American Funds and Rekenthaler, I am much more persuaded against the efficient markets theory. I’d be interested in your thoughts.

Miles: The theory is pretty clear that if there is any departure from the efficient markets theory, most people (or people holding a majority of the risk-tolerance weighted money) have to be getting it wrong. Thus, believing that the efficient markets theory is not right makes me *more* skeptical of active investing. When most investors are getting it wrong, one would have to be doing something unusual to be getting it right.

Dennis:

Thank you, Miles. Active management, the argument goes, is unable to outpace a respective index because of the efficient-market hypothesis.

From the Capital Group whitepaper:

Those who adhere to that theory contend, in brief, that all information is reflected in a firm’s share price, making it impossible to beat the market consistently. But much of the literature in favor of index investing uses “the average active manager” to make the point. And indeed, in aggregate, U.S. equity active managers have not consistently outpaced the Standard & Poor’s 500 Composite Index. …

We believe this is a flawed way to frame the issue, akin to concluding that because the

average person cannot dunk a basketball, no one can dunk a basketball. Obviously,

some are playing at a higher level, and using the average to characterize an entire

industry obscures the fact that there are investment managers that have consistently

added value over a variety of market cycles,

Both studies I referred to in my earlier post demonstrate there are investment managers that have consistently added value over a variety of rolling time periods and market cycles - that is more than talk show chatter. I think it’s important to focus on the qualities associated with success like the contrarian and fundamental value points discussed by Robert Shiller but also including low fees, experience and global research.

While I certainly believe someone like you or Robert Shiller are capable of consistent success, I am skeptical the average person can consistently produce above average results on their own, especially since the average professional investment manager apparently does not (at least after fees). However, I don’t believe that proves the efficient market theory. When there is evidence investment managers that focus on disciplined qualities of success do consistently produce above average results after taxes and fees, then I believe the efficient market theory is hollow. And, If they do it, an average investor can still indirectly succeed by adopting their model by using their funds.

Miles: I am more drawn to the fact that since so many people invest so much money through professionally managed funds, most people putting their money in the hands of professionals must also be doing it wrong, so letting a professional handle one’s funds is no panacea. And that is before paying significant fees, which makes the mistake much worse. The advantage of putting money in low-fee index funds (my Fidelity Spartan accounts have a 0.1% annual fee) is that there is a bound on how far wrong one can go if one comes as close as possibility to holding the universe of accessible risky paper assets in proportion to market capitalizations. The only way to do better than holding a broad set of low-fee index funds is to do things that most investors don’t do when they try to go beyond that. And most investors are more like most investors than they think.

Dennis:Miles, thank you, again, I appreciate your honest, objective thinking on this and the comments of Robert Flood. I must admit It is more difficult for me to completely understand this issue from economist’s point of view without that background. As a practicing CPA and now CFP, I often think about this practical issue for my clients and want to learn as much as I can, including how to sort through the intense marketing claims from both sides that cloud it. Since moving to the full time practice of financial planning about 14 years ago, I have been most influenced by the principles and work of Benjamin Graham, Burton Malkiel and Charles Ellis. My experience is few investment firms put clients’ interests central to their process and approach. I believe most are simply “commercial” and this is the main reason people are attracted to low cost index funds - not because of the efficient markets theory. In other words, I believe some people will (perhaps should) accept a C rather than seek an A or B when doubt or lack of trust exists. Despite the trust issues that exist in the financial services industry, I believe we should not ignore those firms whose processes consistently produce above average results, after fees and taxes, over rolling periods of time and market cycles. They do exist. However, where doubt exists and as a hedge, I am also also inclined to sometimes use low cost index funds or ETFs for myself and for clients.

A few other thoughts: I generally believe equity markets are more efficient in the U.S. than outside the U.S. - and the evidence is appears overwhelming in that space by objectively examining results. I also believe markets are more efficient for large companies over small and mid-size companies where quality proprietary research seems to yield comparatively better results. And finally, to Shiller’s point, I also believe inefficiency exists because most of us are attracted to interesting stories over “boring” stories. In summary, I continue to be persuaded there is room (given the right process that also puts an investor’s interest central) to produce consistent above average results over time. At the same time, I agree with you that most investors (including me) are more like most investors than we want to admit.

Richard Manning Whether Schiller or others believe the market is technically efficient or not on a moment by moment basis the practical advice for the vast majority is the same: buy and hold a diversified portfolio. No? So why the fuss?

John Stuart Mill: Strong Feelings Strongly Controlled by a Conscientious Will

Although I have been Associate Chair for Administration and Director of our Master of Applied Economics Program, I am saved from some of the more onerous leadership and decision-making roles within my department because I am considered a bit unpredictable and a bit too much outside valued boxes. (There is also a tendency to consider someone who has a generally has a positive outlook on people and situations as a less serious person.) In On Liberty, Chapter III: “Of Individuality, as One of the Elements of Well-Being,” paragraph 16, John Stuart Mill extols the virtues of being, in modern slang, a bit of a “loose cannon” and a bit of an “Energizer Bunny”:

As is usually the case with ideals which exclude one-half of what is desirable, the present standard of approbation produces only an inferior imitation of the other half. Instead of great energies guided by vigorous reason, and strong feelings strongly controlled by a conscientious will, its result is weak feelings and weak energies, which therefore can be kept in outward conformity to rule without any strength either of will or of reason. Already energetic characters on any large scale are becoming merely traditional. There is now scarcely any outlet for energy in this country except business. The energy expended in this may still be regarded as considerable. What little is left from that employment, is expended on some hobby; which may be a useful, even a philanthropic hobby, but is always some one thing, and generally a thing of small dimensions. The greatness of England is now all collective: individually small, we only appear capable of anything great by our habit of combining; and with this our moral and religious philanthropists are perfectly contented. But it was men of another stamp than this that made England what it has been; and men of another stamp will be needed to prevent its decline.

Update: On the Facebook version of this post, David Yves offers this comment:

“Do not fear to be eccentric in opinion, for every opinion now accepted was once eccentric.” -Bertrand Russell. If only we didn’t have to fear.

Dimitry Slavin: U.S. Stocks Are Not in a Bubble and Here’s Why

I am quite skeptical of attempts to predict where the stock market overall will go, beyond looking at something like the price/dividend ratio or cyclically adjusted price/earnings ratio a la John Campbell and Robert Shiller, and recognizing moments of market overreaction to geopolitical events. But among those who nevertheless attempt (perhaps foolhardily) to predict, I want to put my “Monetary and Financial Theory” student Dimitriy Slavin in contention. (You can see his Flickr page here, and his LinkedIn page here.) What Dmitriy says sounds at least as sensible to me as others who claim to be able to predict what the market will do–including those with outsized reputations. I’d be interested to hear what people think of his analysis:

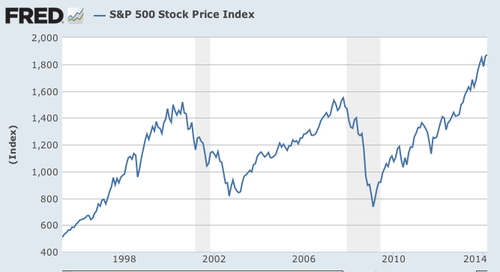

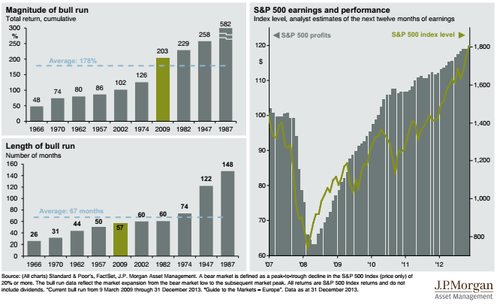

If you take a look at the S&P 500 Stock Index for the past twenty years, you will notice a clear cyclical nature to it- it seems to undergo a cycle about every seven years, with a roughly 5 year period of growth and then a two year period of decline. Five and a half years out of the Great Financial Crisis with the Fed rolling back QE and the S&P index reaching an all time high, some investors are worried that U.S. stocks may be in yet another bubble. In my next two posts, I am going to argue that this is not the case…at least for now.

This weekend I read two interesting documents that have convinced me that it is unlikely we will see a dramatic fall in the S&P anytime soon: JP Morgan’s latest edition ofQuarterly Perspectives and BlackRock’s 2014 Investment Outlook. I will split up my argument into three pieces: (1) Peaks in Stock Prices Vs. Peaks in the Output Gap, (2) Correlation Between the Rise in Stock Prices and the Rise in Corporate Profits, (3) The EV/EBITDA to VIX ratio.

1. Peaks in Stock Prices Vs. Peaks in the Output Gap

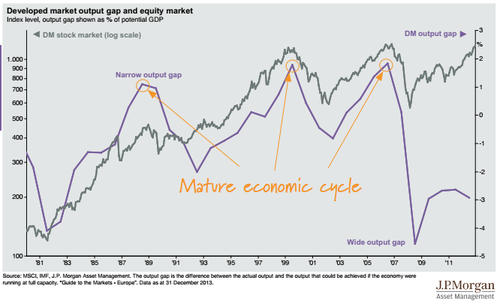

One thing that has characterized past asset bubbles is that they generally tend to coincide with peaks in the economic cycle. As we’ve discussed in class, an economy can’t operate above full capacity for long periods of time, so at some point output must fall. In the past, these falls in economic output have occurred at roughly the same time when the stock market fell:

But as you can see by the graph above, the present case is quite different from the past. The output gap is nowhere near a peak right now, and most would agree that the U.S. economy is still in recovery mode from the financial crisis. This recovery has taken much longer than past recoveries from recessions, and has been characterized by slow initial growth, rising incomes, and slowly falling debt burdens. This slow growth coupled with the current negative output gap is a good sign that the U.S. stock market is not on the cusp of another asset bubble.

2. Correlation Between the Rise in Stock Prices and the Rise in Corporate Profits

One thing that characterizes practically all asset bubbles is an unjustified surge in stock prices. What I mean by ‘unjustified’ is that people begin to ignore fundamental analysis and start buying up stocks simply because their price is rising, much like what happened during the Tulip-Bulb Craze we read about in Malkiel’s Random Walk Down Wall Street. In contrast, the recent rise in stock price has not been unjustified because stock prices have been rising along with corporate profits:

This positive trend gives credence to the argument that investors are not simply building ‘Castles In the Air,’ and rather are basing their investments in sound fundamental analysis. Something to watch out for though is the growth rate of corporate profits versus that of stock prices. I would argue that it is somewhat worrisome that the growth rate in profits for the past three years has been smaller than that of stock prices, and could potentially be a sign that the U.S. stock market will be overvalued in the future. For now though, the difference in growth rates is both tolerable and reasonable.

Taking a look at the left side of the graphic above, we also see that the length of the current bull run is just below the average of past bull runs, yet its return has been slightly higher than average. Roughly average returns + a typical duration time further justify the point that the current bull run on U.S. stocks is not forming an asset bubble.

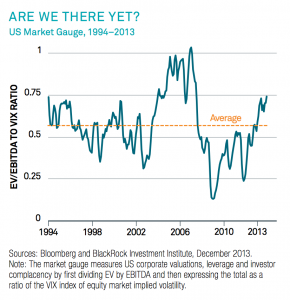

3. The EV/EBITDA to VIX ratio

The final part of my argument has to do with a common market indicator- the EV/EBITDA ratio- a tool that gives a measures of US corporate valuations, leverage, and investor complacency by dividing enterprise value (EV) by earnings before interest, taxes, depreciation, and amortization (EBITDA). This ratio is then divided by the stock market volatility index in order to measure investor complacency.

BlackRock’s 2014 Investment Outlook provides a solid interpretation of the above graph:

“The ratio of the [the EV/EBITDA and the volatility index] is the key. High valuations combined with low volatility can make for a lethal mix. This market gauge sounded the alarm well before the financial crisis…[Today,] valuations are roughly in line with their two-decade average (and leverage is lower). Yet volatility is hovering just above two-decade lows. The result: The market gauge stands well above its long-term average,but is far short of its pre-crisis highs.”

The main point the above graph and discussion make is that although we may be seeing early signs of the formation of an asset bubble, it is not expected to form in the imminent future. It also gives further weight to the argument that corporate earnings need to start rising faster if the economy is to avoid a bubble in the future because a rise in earnings would drive the EV/EBITDA to VIX ratio down (assuming volatility stays low).

In summary, I have laid out a three-pronged argument for why I think the U.S. stock market is not experiencing an asset bubble. A wide output gap, a close correlation between earnings growth and stock price growth, and a reasonably small EV/EBITDA ratio tells me that the U.S. economy is not on the cusp of another bubble. Furthermore, I am generally in agreement with Ray Dalio’s claims (mentioned in some of my previous posts, here and here; the first post examines the long term debt cycle and the second elaborates on the last stage of the cycle- the reflationary period) when he asserts that we are currently in the reflationary period of the long-term debt cycle. Consequently, I expect the economy to make a full recovery in the next couple of years: QE tapering will continue, interest rates will rise slowly but steadily, and both corporate earnings and income growth rates will rise, further dispelling doubts of a possible bubble. With all this in mind though, I think it’s important to keep a close watch on the indicators I discussed throughout this post because they provide a good summary for the state of the U.S. stock market.

Update: Robert Flood notes on Facebook:

Just for the record, the Tulip Bulb Craze (1636) was for fixed-date forward bulb prices not spot. I’m not sure what bubbles you are talking about here - no definition - but I’m real sure you are not studying one in some fixed-date forward/futures price.

Christina Romer: After A Financial Crisis, Economic Disaster Is Not Inevitable—Bonnie Kavoussi Reports →

Bonnie Kavoussi worked for Huffington Post before coming to the Master of Applied Economics program at the University of Michigan that I wrote about last week. Bonnie now has her own blog, where Bonnie reports on Christina Romer’s very interesting talk at the University of Michigan on Tuesday (including an embedded video of the talk). The bottom line is that both of Carmen Reinhart and Ken Rogoff’s big claims in the last few years have been called into serious question:

- Along with many others (many of whom we link to in our follow-up column here), Yichuan Wang and I found no evidence in Reinhart and Rogoff’s data to support their claim that higher national debt lowers the rate of economic growth.

- As Bonnie reports, and as I can verify from my own attendance at the talk, Christina Romer and David Romer question, on solid grounds, Reinhart and Rogoff’s claim that financial crises lead with high probability to a relatively intractable, long-lasting economic downturn.

Mormon Hell Tweets →

Yesterday I posted my favorite song from the musical “The Book of Mormon”: the very moving “Sal Tlay Ka Siti.” The title of the storified tweets linked from the title above is inspired by another, much campier, song from “The Book of Mormon”: “Spooky Mormon Hell Dreams.” The tweets themselves are about Noah Smith’s guest post “Mom in Hell.”

By the way, it is worth listening to the song “Sal Tlay Ka Siti” here and then reading “Mom in Hell” again with “Hell” replaced with “desperate poverty abroad” and “Heaven” replaced by “America.”

The Message of ‘Sal Tlay Ka Siti’

To folks in desperate poverty around the world, America is heaven on earth. Maybe we should let people into heaven.

I saw the musical “The Book of Mormon” in London with my family during the week I went to the Bank of England to talk about eliminating the zero lower bound (and wrote A Minimalist Implementation of Electronic Money and How to Set the Exchange Rate Between Paper Currency and Electronic Money).

To me, the most moving and powerful song was the one above: “Sal Tlay Ka Siti.” Though Salt Lake City is a very nice city, the song is really about America and what America means to people in other countries much poorer than ours. I hope you take time to listen to the song and think about its message. Here is the link to the video above that has the lyrics and audio for the song Sal Tlay Ka Siti from the play. But you can watch it right here. (The music starts about 15 seconds in.)

Note: my column “The Hunger Games is Hardly Our Future: It’s Already Here” has the same message. I think you will like it. I also put out a couple of tweets about immigration on Monday morning while reading the Wall Street Journal article “Jeb Bush to Decide by Year-End Whether to Run for President”:

“Maybe it wasn’t talent the Lord gave me, maybe it was the passion.”

– Wayne Gretzky, as quoted in The Sports Gene by David Epstein

Big Banks' Shadow Dance by Simon Johnson →

One of the great myths propagated by large financial institutions is that proper regulation would drive many investors to shadow banks. In reality, there are three kinds of shadow activities, all of which are obvious, operate in plain sight, and could be controlled in a straightforward and responsible fashion.

Noah Smith: Mom in Hell

This is a guest post by Noah Smith.

How can you be happy in Heaven while your mom is in Hell?

In his famous 1741 sermon, “Sinners in the Hands of an Angry God”, Jonathan Edwards said:

There will be no end to this exquisite horrible misery. When you look forward, you shall see a long for ever, a boundless duration before you, which will swallow up your thoughts, and amaze your soul; and you will absolutely despair of ever having any deliverance, any end, any mitigation, any rest at all. You will know certainly that you must wear out long ages, millions of millions of ages, in wrestling and conflicting with this almighty merciless vengeance; and then when you have so done, when so many ages have actually been spent by you in this manner, you will know that all is but a point to what remains. So that your punishment will indeed be infinite.

Now, in a time when most people still lived lives of poverty and hardship, florid language like that was probably necessary just to get people to pay attention in church. But the sermon illustrates something that I’ve never really understood about Christianity - the idea of Hell.

In the Christian concept of Hell, if you believe in Jesus (and in some denominations, maybe satisfy a few other requirements), you go to Heaven, and if you don’t believe in Jesus, you go to Hell. So in Christianity, it’s perfectly possible for you to be in Heaven while your mom is in Hell, experiencing all the nasty stuff that Jonathan Edwards describes.

Now, a Christian will tell you, we don’t know who will go to Heaven and who will go to Hell. But after you die, you must surely be able to know. If you’re in Heaven, and you want to say hi to your mom, you can just look her up. If she’s in Heaven with you, you should be able to easily find her, using whatever version of the white pages exists in Heaven. If you can’t find her, you will know by process of elimination that she must be in Hell.

So, you’re supposed to be happy in Heaven, right? But suppose your mom goes to Hell. How can you be eternally happy, knowing that your mom is experiencing eternal torment?

Maybe Heaven changes you. Maybe once you go to Heaven, you don’t mind if your mom is in Hell. But that would be a really big personality change, right? I think that if I became someone who didn’t mind my mom suffering eternal torment, I wouldn’t really be me anymore. It would be someone else in Heaven, and I’d just be gone.

Now, a Christian believer in Hell might respond, “What’s to understand? If you go to Heaven and your mom goes to Hell, then you’re just going to have to deal with it.” But in that case, the idea that Heaven is a place where you’re happy forever has got to be tossed out the window.

So I just don’t understand how the Heaven/Hell system works. If people only cared about themselves, then it would make sense, but we care about other people too. And it’s just flat-out impossible for most people to be totally happy while knowing that someone they love is being tortured eternally in the most horrific concentration camp in the cosmos. But according to Christianity, that situation is perfectly capable of happening.

I just don’t get it.

Don’t miss Noah’s other guest religion posts:

For other religion posts, see my Religion, Philosophy, Humanities, Science Fiction and Science sub-blog.

Update: David Beckworth tweets this very interesting video from a Christian ministry making trenchant arguments from within the Christian tradition against the picture of hell that Noah is attacking.

Yuan Tian: Will the Real Estate Bubble Burst in China?

In this guest post, Yuan Tian, a student in my “Monetary and Financial Theory” class, discusses one of the most important dangers the world economy now faces: a possible collapse of housing prices in China, with unknown effects on China’s banking system. Here is what Yuan has to say:

It’s always a hot topic among Chinese people to talk about real estate prices. The bubble has become bigger and bigger since the 1990s. Of coruse, a bubble is an unsustainable rise in the price of an asset, well above the market price given fundamentals. A bubble is indicated by three signs: a gap between disposable income and home prices, rising inventory, and a rising number of properties per person.

In a way that would be hard to imagine for Americans, in the current real estate situation the majority of Chinese people still can’t afford a house after working hard for a lifetime. China’s real estate prices have been changing in dramatic ways: prices soaring in the past, and now perhaps an environment of declining prices. That is the question: will the real estate bubble really burst in China?

Optimists insist that the prices won’t decrease a lot due to the large population and demand in China. They also mentioned that right now in the bubble, China’s residential mortgage debt is only 15% while in the U.S. borrowing 80% of a house’s value is considered conservative.

Pessimists don’t think so. They are arguing that as China’s financial market matures, people might be less likely to purchase houses because they will have more other investment options.

As for population growth, statistics show that the population will reach the peak in 2018 and labor force will shrink starting in 2015. Thus people predict that the property prices will start to fall between 2017 and 2018 thanks to the “one child policy” and China’s aging population composition. According to this information, pessimists predict a 40% decrease in the next five years since there will be fewer people willing to purchase a house but the supply is still large. Anther great concern, that I take very seriously, is the possibility of falling dominoes. Once the supply is bigger than the demand, real estate companies will face a money chain rupture. They will have to decrease the price to attract more buyers and save the company.

If there is a crash, it could cause a financial crisis like the United States faced in 2008. In the US, housing prices declined steeply after peaking in mid-2006, and it became difficult for many borrowers to refinance their loans. As adjustable-rate mortgages began to reset at higher interest rates (causing higher monthly payments), mortgage delinquencies soared. Securities backed by mortgages, including subprime mortgages, which were widely held by financial firms globally, lost most of their value. Global investors tried to drastically reduce their holdings of mortgage-backed debt and other securities, and there was a decline in the capacity and willingness of the private financial system to support lending. Concerns about the soundness of U.S. credit and financial markets led to tightening credit around the world and slowing economic growth in the U.S. and Europe.

To save the market, right now Chinese government is trying hard to come up with policy interventions. Let’s have a brief look at China’s housing industry changes and government policy responses in recent years.

Before 2003, as part of fostering economic growth in China’s, the Chinese government regulated and supported the under-developed housing market. From 2000 on, there was no more government housing allocation in China and people had to purchase houses through housing companies. After that, the government enacted a series new rules and regulations such as lower mortgage rates, reduced down payments, and lower transaction fees to further stimulate the housing industry.

Then in 2002, the Public Land Building System was enacted. Following in 2004, all lands started to be put up for auction. It was around that time that housing prices began to rise. From 2004 to 2006, with Chinese government encouraging housing sales and offered many benefits to the housing industry as well as fostering economic growth more generally. Prices of houses rose a lot not only in big cities but also in small inland cities. Construction boomed rapidly during this period.

In 2005, in response to the increasing prices, “Eight Rules,” “New Eight Rules” and “Opinion of Such Departments as the Ministry of Construction on Effectively Stabilizing House Prices” were enacted, marking the central government’s first efforts to rein in home prices. But the trend was hard to stop. For example, over the course of the one year, 2005, average housing prices in Beijing increased by 20%, while the price had increased only 0.78% from 2000 to 2004. The bubble has only gotten worse since then, despite the government’s efforts to stop it.

Later in 2010, China posted the “Notice of the State Council on Resolutely Curbing the Soaring of Housing Prices in Some Cities” to require a down payment on second homes from 40% to 50%. In addition, banks must charge a minimum mortgage rate on second homes of 1.1 times the benchmark interest rate, and increased down payments on first home larger than 90 square meters from 20% to 30%. Then in 2011, China had “National Eight” real estate market regulations. On the other hand, Chinese government has started the property tax pilot program–a program I think is pretty useful. The program asks for higher property taxes for those who own more houses in China. It has been in place in Shanghai and Chongqing since 2011.

Prices might be controllable in the future by government policies. So far, recent policies have not been given deadlines. In the short run, there may be volatility due to uncertainty.

Though we can’t know when the bubble will burst, the recent situation in China gives some ominous portents. According to the Securities Times newspaper, housing developers in the industrial city of Hangzhou cut prices this week by an average 19% in a scramble to sell about 120,000 newly-built apartments. The current inventory of new, unsold units now exceeds the total number of housing units offered for sale in Beijing and Shanghai combined. A study by Shanghai’s Tongji University said real estate has been especially shaky in the northeastern city of Wenzhou, where new-home prices have fallen every month for the last two years.

My view is that the housing bubble will burst in near future–or may now be in the process of bursting.

Yuan Tian

Matt Ridley, Michelle Klein and Rob Boyd on Population Size and Technology: Why Some Islanders Build Better Crab Traps →

In this ungated Wall Street Journal article, Matt Ridley gives a nice report on research by Michelle Klein and Rob Boyd on the idea that higher effective population size leads to better technology. The important idea that higher effective population size leads to better technology is also reflected in

- powerhouse economist Michael Kremer’s paper “Population Growth and Technological Change: One Million B.C. to 1990,”

- Jared Diamond’s Pulitzer Prize winning book Guns, Germs and Steel and

- Alex Tabarrok’s TED talk “How Ideas Trump Crises.”

Miles on #econchat, March 30, 2014 →

#econchat organizes Twitter discussions about economics and the teaching of economics. I was the guest last night. I answered a wide variety of questions. I think you will find it interesting because of the high quality of the questions that I tried to answer.