Contra Randal Quarles

Donald Trump has nominated Randal Quarles as the Federal Reserve's Vice Chairman for Supervision. This is a position that really matters. As Ryan Tracy wrote in the July 28, 2017 Wall Street Journal article "Meet Randal Quarles, Trump’s Pick to Shake Up the Fed,"

Mr. Quarles, who would be President Donald Trump’s first appointee to the central bank, is expected to be confirmed in coming months for a four-year term as Fed vice chairman for supervision. That would make him the most influential U.S. financial regulator and give him a voice on monetary policy.

I urge the Senate not to confirm him.

If Randal does become the Federal Reserve's Vice Chairman for Supervison, I hope that Randal changes his views (or perhaps has already changed his views since the quotations below). Let me detail where I disagree with Randal to do my bit toward one of those more favorable outcomes. I will mostly follow the order of the article linked above: "Fed Nominee Randal Quarles in His Own Words." Most of the quotations below from Randal can be found in that article; some are in sources that article links to.

How Should Banks Be Funded?

Randal the 2016 op-ed "Focusing on Bank Size, Missing the Real Problem" with Lawrence Goodman. They write:

Focusing on bank size is politically appealing but diverts attention from the major source of systemic risk in the financial sector: a shortage of stable deposits. Banks are but one part of an interconnected financial sector providing over $40 trillion of credit to the economy, but that credit is supported by only about $11 trillion of bank deposits.

The gap must be closed largely with professionally managed, “wholesale” funding, such as short-term repurchase agreements. Wholesale funders are quick to pull their support by not rolling over short-term credit if they perceive those funds are at risk. This leads to periodic runs on financial institutions and the resulting demand for government intervention to prevent the failure of those institutions.

It is fair to say that "too big to fail" has been overhyped, since "too many to fail" can also lead to bailouts. And Randal and Lawrence are right that the way in which banks are funded is the key question for financial stability. But after saying correctly that the way banks are funded now is unsafe, without even trying to offer a better means of funding banks, they dismiss what they concede would be a much safer means of funding banks:

Mr. Kashkari’s alternative proposal, promoted by academics including most vocally Stanford economist Anat Admati, is to ramp up bank capital to such a degree that the possibility of failure would be remote to nonexistent. But the consequence of a dramatic increase in bank capital is an increase in the cost of bank credit, meaning higher interest rates across the board. Those who favor much higher bank capital argue this would not happen, because investors would accept lower returns if the banks they put their money in were safer.

In the real world of capital markets, however, there are not enough natural investors in bank equity seeking utility-like returns.

Note that Randal and Lawrence do not dispute that increasing bank capital would make banks safer. They concede that point. They object because they believe making banks safer in this way will increase the cost of bank credit so much that it outweighs the benefit of the extra safety.

Let me argue that the increase in the cost of bank credit would not be so great or so harmful as Randal and Lawrence believe. First, I think they are wrong when they say

... there are not enough natural investors in bank equity seeking utility-like returns.

If bank stock really were as safe as utilities, the same kind of people who invest in utilities and who invest in corporate bonds would invest in safe bank stock. The issue is that bank stock has to prove over time that it is, indeed, safe. Theory gives excellent reason to think that, other things equal, bank stock will be much safer when there is more of it for a bank of given size, since the risk will be shared across more stockholders. But one should not expect investors to instantly believe bank stock is safer than it used to be, especially so soon after a painful financial crisis. And so far the increase in the risk spreading by an increase in the total amount of stock has been modest enough that other factors could easily overwhelm the effects of greater equity finance. So the push towards banks being financed by stock instead of by "wholesale funding" needs to be sustained for long enough to make bank stock so much safer that investors can't help but see the added safety.

Second, of course the cost of bank credit would go up if banks were required to finance themselves more from stock rather than flightier funding ("more bank capital"). But that is as it should be. Because banks would be safer, they would lose the implicit bailout subsidy they now have. Without that government subsidy to lending, it is natural and appropriate for the cost of lending to go up. If we think that the government should be subsidizing lending (say to counteract a distortionary financial friction), let's at least subsidize lending in a way where banks don't have the incentive to design themselves as fragile in order to get the subsidy.

The bankruptcy of Randal and Lawrence's approach becomes clear in this passage from their op-op-ed:

Given these structural facts, the job of the regulatory system is clear. First, facilitate the reallocation of capital during the inevitable periodic crises through orderly liquidation of failing or failed banks.

That is, "Give up on trying to keep banks from failing. Give up on trying to have the cost of mistakes absorbed by stockholders. Depend on "orderly liquidation" to happen fast enough to keep a financial crisis from getting worse. This is not a plan for avoiding financial crises at all, it is a resignation to the fate of serious financial crises over and over again. If banks make bad bets, the one truly "orderly" way to have the system of losses is to have enough stockholders who have

- signed up to take the hit if things to south,

- in that worst case scenario take the hit very quickly, before they have had a chance to build up steam to ask for a bailout, and

- are reminded every day as the stock prices go up and down that they have accepted that risk, so that they have a hard time pretending they didn't know, and should be bailed out.

The Role of the Government in the Financial System

In a May 2015 Bloomberg television interview, Randal said

“The government should not be a player in the financial sector. It should be a referee. And both the practice and the policy and the legislation that resulted from the financial crisis tended to make the government a player. It put it on the field as opposed to simply reffing the game.”

The government is a player in the financial system as long as banks think they will be bailed out in in a crisis. In order to be less of a player through expected bailouts, the government has outlaw the kind of designed fragility that banks have the incentive to pursue given the bailout subsidy. To me, insisting on very high capital requirements is acting like a referee, since the whole game comes crashing down when bank mistakes cannot be absorbed by stockholders. But this is a type of getting out of the game and being a referee that Randal argued against.

One key way in which high equity requirements allow the government to get out of the game and be a referee is that if liability-side regulation for banks means that stockholders are set to absorb losses, the government doesn't need heavy-handed legislation on the asset side. For example, the Volcker rule that Randal said in the same Bloomberg TV interview he dislikes is only needed because capital requirements are too low. (See my post "The Volcker Rule.")

Of course, some asset-side regulations are necessary, because extreme-enough derivatives on the asset-side could create a situation equivalent to excessive leverage, even if a very large share of funding came from equity. But with a very high equity requirement on the liability side of banks' balance sheets, the asset-side rules would only need to rule out practices that are quite far from what most banks currently do on the asset side.

There are other ways of getting out of the game and being a more neutral referee that I think Randal and I might agree on. Let's split up Fannie and Freddie and fully privatize the pieces. Let's equalize the taxation of debt and equity so that incentive towards high leverage isn't added on top of the bailout subsidy.

On Monetary Rules

Here I can just use duelling quotations. From the May 2015 Bloomberg TV interview:

Randal: I am all for transparency; I think the Fed has that part of it right. What it has wrong is that it continues to believe that it shouldn’t be following a rule. If you are going to be transparent in activity like the Fed’s, you have to be much more rule-based in what you are doing. The transparency has to involve, ‘This is the rule that we will follow.’ So that the markets can say, “OK, we now understand what is the Fed is going to do. We can see what its inputs are.”

From my paper "Next Generation Monetary Policy" (see "The Scientific Approach to Monetary Rules"):

Because optimal monetary policy is still a work in progress, legislation that tied monetary policy to a specific rule would be a bad idea. But legislation requiring a central bank to choose some rule and to explain actions that deviate from that rule could be useful. To be precise, being required to choose a rule and explain deviations from it would be very helpful if the central bank did not hesitate to depart from the rule. In such an approach, the emphasis is on the central bank explaining its actions. The point is not to directly constrain policy, but to force the central bank to approach monetary policy scientifically by noticing when it is departing from the rule it set itself and why.

Interest Rates and Speculation, Hawks and Doves

In "Focusing on Bank Size, Missing the Real Problem," Randal and his coauthor Lawrence write:

Years of near-zero interest rates have led to a rise in speculative positions across a wide range of asset classes, as all financial institutions find themselves under intense pressure to seek adequate returns.

Let me answer this in a roundabout way. At the Mercatus Center's "Monetary Rules for a Post-Crisis World" Conference" (video) where I first presented "Next Generation Monetary Policy," I made the point that being a monetary "hawk" or dove makes little sense if a "hawk" is someone who, whatever the circumstance, thinks interest rates should be higher and a "dove" is someone who, whatever the circumstance, thinks interest rates should be lower. In my view, as laid out in "Next Generation Monetary Policy," interest rates should be very high for brief periods in some circumstances and very low for brief periods in others, in order to quickly right the economy if it lists towards overheating or recession. The way to tell someone who is a hawk is the tendency to set out a motley grab bag of arguments that have no coherence except that they all favor higher interest rates. Despite his stated views in favor of monetary rules that have interest rates much higher in some circumstances than others, John Taylor is a good source for such a motley grab back of arguments. You can see this motley grab bag in my post "Contra John Taylor." The argument that low interest rates lead to excessive speculation is a particular favorite of hawks. Here is what John said together with my reply:

[John Taylor:] The Fed’s current zero interest-rate policy also creates incentives for otherwise risk-averse investors—retirees, pension funds—to take on questionable investments as they search for higher yields in an attempt to bolster their minuscule interest income.

[Miles:] I can’t make sense of this statement without interpreting it as a behavioral economics statement about some combination of investor ignorance and irrationality and fraudulent schemes that prey on that ignorance and irrationality. The often-repeated claim that low interest rates lead to speculation cries out for formal modeling. I don’t see how such a model can work without some combination of investor ignorance and irrationality and fraudulent schemes preying on that ignorance and irrationality. (That is, I don’t see how the claim could hold in a model with rational agents and no fraud.) Whatever combination of investor ignorance and irrationality and fraudulent schemes preying on that ignorance an irrationality a successful model uses are likely to have much more powerful implications for financial regulation than for monetary policy. It is cherry-picking to point to implications of a not-fully-specified model for monetary policy and ignore the implications of that not-fully-specified model for financial regulation.

To what I said back in January 2013, I should add two thoughts, in response to both John and Randal's concerns about what is often called "reaching for yield."

First, it is possible to have an "irrational firm" due to incentive structures within the firm, or an "irrational contract" due to incentive structures within the contract, even if given the structure of the firm or contract the individuals act rationally. This is sometimes called an "institutional" explanation of a phenomenon.

Second, remember that "risk-taking" has a positive side to it. Often, a recession persists because of too little risk-taking. When people aren't taking the risks the economy needs them to take to keep functioning well, it is important to make the alternative of playing it safe less attractive. That is exactly what low interest rates do.

The key to making risk-taking a good thing rather than a bad thing is to align the benefits and costs of the risk to the one making the risk-taking decision with the benefits and cost of the risk to society. Having high enough levels of equity—or equivalently, low enough leverage—so that there won't be bailouts helps a lot with that alignment. Otherwise it is "heads I win, tails the taxpayer loses."

In "Monetary Policy and Financial Stability" I argue:

- It is almost impossible for monetary policy to stimulate the economy except by (a) raising asset prices, (b) causing loans to be made to borrowers who were previously seen as too risky, or (c ) stealing aggregate demand from other countries by causing changes in the exchange rate.

- Quantitative easing is likely to have unprecedented effects on financial markets—effects that will look unfamiliar to those used to what the standard monetary policy tool of cutting short-term interest rates does.

- It is not risk-taking we should be worried about, but efforts to impose risks on others—including taxpayers—without fully paying for that privilege.

... nonstandard monetary policy in the form of purchases of long-term Treasury bonds and mortgage-backed securities and “forward guidance” on future short-term interest rates take the economy into uncharted territory. But uncharted territory brings not only the possibility of new monsters but also the near certainty of previously unseen creatures that might look like monsters, but are harmless.

Letting people get high interest rates from a central bank is OK when they would otherwise invest too much and overheat the economy. But when the economy desperately needs more risk-taking investment, tempting people away from that risk-taking investment by letting people get high interest rates from a central bank is folly.

To the extent that banks turn to forms of risk-taking other than loans when the interest rate they can earn from the government goes down, I think it has a lot to do with the faulty approach of cutting interest rates a modest amount for a long time (or making large-scale purchases of long-term bonds), instead of cutting short-term interest rates sharply for a briefer period of time. Here, it is important to remember that there is no lower bound on the interest rates that can be earned from the government—except as a result of policy.

Dodd-Frank

In the November 2015 Bloomberg TV interview, Randal said:

In some ways Dodd-Frank was not ambitious enough, and in other ways it was overly ambitious and I think there are lots of ways to refine Dodd-Frank and other forms of regulatory policy in ways that would be beneficial to the economy.

I have no doubt that there are many flaws in Dodd-Frank. But given where financial industry lobbyists and many in Congress and the Administration may want to go, I view Dodd-Frank now as an important bulwark against weakened capital requirements. I also see the Consumer Financial Protection Bureau it established as important. In "On the Consumer Financial Protection Bureau" I argue there are

... three principles that can justify consumer financial protection beyond simple contract enforcement:

Duping people is fraud even if they wouldn’t have been duped had they had infinite time and infinite intelligence. ...

Facilitating gain for oneself and harm to others by taking advantage of preexisting confusion is predation of those who are especially vulnerable. ...

It is legitimate to protect time-slices of people from serious injury by other time-slices of people.

I don't have any problem with tinkering with Dodd-Frank to improve it—on two conditions: that Anat Admati and the Consumer Financial Protection Bureau's former Chief Economist Chris Carroll both endorse the modification to Dodd-Frank.

Tying the Government's Hands in a Situation Calling for a Bailout

In 2011, at the Atlantic Council think tank, Randal said

I have come to believe that there is a fundamental problem with resolution mechanisms that allow substantial discretion for governments to act in particular cases, which Dodd-Frank…does. The consequence of that is that it multiplies uncertainty in a time of crisis because you’re not going to act until you know what the government is going to do…as opposed to the admittedly more difficult, and perhaps unattainable, but I think ultimately the only really workable solution, which is to sort of have something that is like a bankruptcy regime—a rules-based approach as opposed to something that says, ‘and then ‘Mr. Wizard will decide what to do.’

I worry that what Randal calls "a rules-based approach" would, in fact, be an approach that tried to tie the government's hands so it could not do a bailout. But some situations call for bailouts. And it is hard for people writing the rules to fully put themselves in the shoes of those in the dire situation that calls for bailouts. Moreover, I think banning bailouts that would have much different effects in practice than in theory, because banning bailouts is not really banning bailouts—it simply puts legal obstacles in the way of bailouts that would still probably happen, but with even more uncertainty because of those legal obstacles.

As I said in my talk "Restoring American Growth,"

The moment you let banks [have] high leverage, that is the moment you've decided to do a bailout.

Trying to tie the government's hands so that, ex post, it can't do a bailout is unlikely to actually succeed in stopping a bailout, but is likely to make the bailout more costly. The better course is to prevent a bailout from being necessary in the first place by requiring that banks fund themselves much more by stockholder equity and much less by debt.

Conclusion

Let me emphasize that my criticisms of Randal Quarles' views above are not criticisms directed at Randal personally. From what little I know of him, I think he is more likely to modify his views in response to cogent arguments than most prominent people are. In "Meet Randal Quarles, Trump's Pick to Shake Up the Fed," Ryan Tracy writes:

Friends and former colleagues said that if Mr. Quarles does try to change direction at the Fed, they expect him to move slowly and methodically, and to seek consensus. ...

Ravi Menon, a Singaporean official who engaged in last-minute talks with Mr. Quarles on a U.S.-Singapore trade deal, wrote in 2004, “Right from the start, we took a problem-solving approach aimed at finding middle ground rather than trying to convert each other on ideological arguments.”

In other words, Randal is not as dogmatic as many of those who are in positions of power, and is open to persuasion. Nevertheless, unless he reconsiders his views, I worry that a vote for Randal Quarles is a vote for another financial crisis, simply because as things stand, he is not committed to doing whatever is possible to continue to raise capital requirements on banks.

Further Reading: "Martin Wolf: Why Bankers are Intellectually Naked"

John Locke: Freedom is Life; Slavery Can Be Justified Only as a Reprieve from Deserved Death

Marketplace for selling innocent individuals who were enslaved. John Locke's account of the "Law of Nature" suggests that those who did the enslaving deserved death or slavery themselves. Image source

In section 23 of his 2d Treatise on Government: “On Civil Government” (in Chapter IV "Of Slavery"), John Locke makes what I consider two logical errors. Taking as given the religious condemnation of suicide in his cultural milieu, he argues:

Since I do not have the right to kill myself, I also cannot give someone else the right to kill me.

Since freedom is so crucial to the preservation of my life, I also cannot give away my own freedom.

However, John Locke also suggests

If I commit a crime worthy of death, that the individual or group I have harmed can choose to commute a sentence of death to a sentence of slavery.

Being enslaved is no worse a punishment than death because, as a practical matter, it is very difficult to prevent me from killing myself if I viewed slavery as worse.

Here is the exact text:

This freedom from absolute, arbitrary power, is so necessary to, and closely joined with a man’s preservation, that he cannot part with it, but by what forfeits his preservation and life together: for a man, not having the power of his own life, cannot, by compact, or his own consent, enslave himself to any one, nor put himself under the absolute, arbitrary power of another, to take away his life, when he pleases. No body can give more power than he has himself; and he that cannot take away his own life, cannot give another power over it. Indeed, having by his fault forfeited his own life, by some act that deserves death; he, to whom he has forfeited it, may (when he has him in his power) delay to take it, and make use of him to his service, and he does him no injury by it: for, whenever he finds the hardship of his slavery outweigh the value of his life, it is in his power, by resisting the will of his master, to draw on himself the death he desires.

The lesser of the two logical problems is that John Locke effectively allows me to give away my freedom by committing a serious crime. So I can give away my freedom by committing a serious crime. John Locke could answer that since I do not have the right to commit the crime, I also do not have the right to give away my freedom in this way. And few people are eager to give away their freedom, so allowing such a loophole for giving away one's freedom is unlikely to be a practical problem. The usual temptations to give away one's freedom involve selling one's freedom in some way for something else one wants. And the usual temptations for crime are the hope of getting something one wants from the crime without losing one's freedom or suffering any other penalty.

The bigger logical disjunction here is that for some reason, John Locke regards suicide as an alternative to slavery as a legitimate choice, while suicide under other circumstances is not. But if suicide as an alternative to slavery is legitimate, why wouldn't suicide as an alternative to an extraordinarily painful and lingering terminal disease be legitimate? (Suppose everyone agreed that enduring the extraordinarily painful and lingering terminal disease was worse than enduring slavery.) Or if it is illegitimate to commit suicide as an alternative to suffering under an extraordinarily painful and lingering terminal disease, shouldn't suicide as an alternative to a situation of bondage more bearable than that disease also be illegitimate?

For links to other John Locke posts, see these John Locke aggregator posts:

John Locke's State of Nature and State of War (Chapters I–III)

On the Achilles Heel of John Locke's Second Treatise: Slavery and Land Ownership (Chapters IV–V)

John Locke Against Natural Hierarchy (Chapters VI–VII)

John Locke's Argument for Limited Government (Chapters VIII–XI)

John Locke Against Tyranny (Chapters XII–XIX)

Why GDP Can Grow Forever

Robert Gordon's argument that economic growth will slow down in the future made a big splash in 2012. He laid out his views in the Wall Street Journal op-ed shown above, as well is in other venues. His book The Rise and Fall of American Growth will come out on September 5, 2017.

A key part of Robert Gordon's argument is that dramatic changes in people's lives from past economic growth are unlikely to be repeated. He writes in his 2012 op-ed:

The growth of the past century wasn't built on manna from heaven. It resulted in large part from a remarkable set of inventions between 1875 and 1900. These started with Edison's electric light bulb (1879) and power station (1882), making possible everything from elevator buildings to consumer appliances. Karl Benz invented the first workable internal-combustion engine the same year as Edison's light bulb.

his narrow time frame saw the introduction of running water and indoor plumbing, the greatest event in the history of female liberation, as women were freed from carrying literally tons of water each year. The telephone, phonograph, motion picture and radio also sprang into existence. The period after World War II saw another great spurt of invention, with the development of television, air conditioning, the jet plane and the interstate highway system.

The profound boost that these innovations gave to economic growth would be difficult to repeat. Only once could transport speed be increased from the horse (6 miles per hour) to the Boeing 707 (550 mph). Only once could outhouses be replaced by running water and indoor plumbing. Only once could indoor temperatures, thanks to central heating and air conditioning, be converted from cold in winter and hot in summer to a uniform year-round climate of 68 to 72 degrees Fahrenheit.

The main claim a typical reader would take from this passage that it will be hard to make as big a difference to people's lives with the next 150 years of technological progress as with the last 150 years of technological progress. Robert Gordon may turn out to be wrong on all counts. Some believe a technological "singularity" will come within the next 150 years that will dramatically change human existence to something "transhuman."

But even if Robert Gordon is right that the next 150 years of technological progress will not make anywhere near as big a difference to people's lives as the last 150 years of technological progress, I have a highly technical criticism to his transition from that claim to his statement

The profound boost that these innovations gave to economic growth would be difficult to repeat.

Based on other things Robert Gordon has written, I interpret that as a statement about the effect of technological progress on real GDP growth. So interpreted, the statement "The profound boost that these innovations gave to economic growth would be difficult to repeat." may be true, but it does not follow logically from the difference technological progress has made to people's lives being hard to repeat.

The gap between "it is hard to repeat that improvement in people's lives" to "it is hard to repeat that boost to real GDP growth" has to do with what a weak reed real GDP growth is for understanding economic improvements. Let me leave aside all the many ways in which GDP can go up even if people's lives worsen. (See "Restoring American Growth: The Video" for a discussion of that.) If all non-market goods and parameters of income distribution stay the same and real GDP increases, people are indeed better off. But "How much better off?" What does it mean to say that GDP is 1% higher?

GDP was conceived with increases in quantity in mind. If people get more goods and services it is clear what an x% increase in GDP means. But more of exactly the same good or service becomes less useful very fast. If more people are getting goods that others already had, what is going on is also relatively clear. But what if enough people have all the want of exactly the same good or service they already have that entrepreneurs introduce a good that is in some respect new. It may be an entirely new good or something easy to see as an improvement in the quality of an existing good. In either case, the way government agencies factor this into GDP is that the value of the new good is measured by how much of more of the same people are willing to give up to get something new. Given how boring more of the same might be to at least some people, the amount some fraction of people are willing to give up of more of the same to get something new might be substantial. Therefore, the production of something wholly new or something seen as a higher quality modification of something old can count as a substantial addition to GDP growth.

In the extreme, if people became bored enough with more of the same, a set of truly tiny quality improvements could be counted as 3% growth in GDP, because a marginal 3% of boring products one doesn't need that much of is hardly any sacrifice at all.

My technical point is relevant not only to Robert Gordon's argument, but also to Tom Murphy's arguments in his posts "Can Economic Growth Last?" and "Exponential Economist Meets Finite Physicist." To his statement "economic growth cannot continue indefinitely," I say,

It depends what you mean by economic growth. If you mean GDP growth, all it takes for it to grow forever at a rate always above a positive x% per year is for tiny quality improvements or novelties to be valued extremely highly relative to a higher quantity of the same old things.

And it is not clear that what are seen as tiny quality improvements require any violations of the laws of physics, since quality improvements are all in the eye of the beholder.

Despite my framing of this post as a correction to Robert Gordon's and Tom Murphy's arguments, the real moral of this post is the imperfections of real GDP growth as a measure of "economic growth" in the broader sense of people getting more of what they want. GDP is a quantity-metric measure of economic welfare. If quantity is no longer very valuable, a quantity-metric measure shows small improvements in quality or novelty as equivalent to large increases in quantity.

Another way to look things is that Robert Gordon implicitly brings into his argument declining marginal utility. It is quite possible for economic growth to continue to be rapid by the conventional measure of GDP growth without it making as big a difference in people's lives as that rate of GDP growth made in the past.

Note: People's intuitions about declining marginal utility have other potential implications as well. See "Inequality Aversion Utility Functions: Would $1000 Mean More to a Poorer Family than $4000 to One Twice as Rich?"

Noah Smith: Seeking the Cure for American Economic Sclerosis →

I recommend the Bloomberg View article at the link above. These are tough issues. You can see my attempt to begin addressing them in "Restoring American Growth: The Video."

Let's Set Half a Percent as the Standard for Statistical Significance

My many-times-over coauthor Dan Benjamin is the lead author on a very interesting short paper "Redefine Statistical Significance." He gathered luminaries from many disciplines to jointly advocate a tightening of the standards for using the words "statistically significant" to results that have less than a half a percent probability of occurring by chance when nothing is really there, rather than all results that—on their face—have less than a 5% probability of occurring by chance. Results with more than a 1/2% probability of occurring by chance could only be called "statistically suggestive" at most.

In my view, this is a marvelous idea. It could (a) help enormously and (b) can really happen. It can really happen because it is at heart a linguistic rule. Even if rigorously enforced, it just means that editors would force people in papers to say "statistically suggestive” for a p of a little less than .05, and only allow the phrase "statistically significant" in a paper if the p value is .005 or less. As a well-defined policy, it is nothing more than that. Everything else is general equilibrium effects.

I previewed the paper and some of why tightening the standards for statistical significance could help enormously in "Does the Journal System Distort Scientific Research?" In the last few years, discipline after discipline has faced a "replication crisis" as results that were considered important could not be backed up by independent researchers. For example, here are links about the replication crisis in five disciplines:

Here is a key part of the argument in "Redefine Statistical Significance":

Multiple hypothesis testing, P-hacking, and publication bias all reduce the credibility of evidence. Some of these practices reduce the prior odds of [the alternative hypothesis] relative to [the null hypothesis] by changing the population of hypothesis tests that are reported. Prediction markets and analyses of replication results both suggest that for psychology experiments, the prior odds of [the alternative hypothesis] relative to [the null hypothesis] may be only about 1:10. A similar number has been suggested in cancer clinical trials, and the number is likely to be much lower in preclinical biomedical research. ...

A two-sided P-value of 0.05 corresponds to Bayes factors in favor of [the alternative hypothesis] that range from about 2.5 to 3.4 under reasonable assumptions about [the alternative hypothesis] (Fig. 1). This is weak evidence from at least three perspectives. First, conventional Bayes factor categorizations characterize this range as “weak” or “very weak.” Second, we suspect many scientists would guess that P ≈ 0.05 implies stronger support for [the alternative hypothesis] than a Bayes factor of 2.5 to 3.4. Third, using equation (1) and prior odds of 1:10, a P-value of 0.05 corresponds to at least 3:1 odds (i.e., the reciprocal of the product 1/10 × 3.4) in favor of the null hypothesis!

... In biomedical research, 96% of a sample of recent papers claim statistically significant results with the P < 0.05 threshold. However, replication rates were very low for these studies, suggesting a potential for gains by adopting this new standard in these fields as well.

In other words, as things are now, something declared "statistically significant" at the 5% level is much more likely to be false than to be true.

By contrast, the authors argue, results declared significant at the 1/2 % level are at least as likely to be true as false, in the sense of being replicable about 50% of the time in psychology and about 85% of the time in experimental economics:

Empirical evidence from recent replication projects in psychology and experimental economics provide insights into the prior odds in favor of [the alternative hypothesis]. In both projects, the rate of replication (i.e., significance at P < 0.05 in the replication in a consistent direction) was roughly double for initial studies with P < 0.005 relative to initial studies with 0.005 < P < 0.05: 50% versus 24% for psychology, and 85% versus 44% for experimental economics.

What about the costs of a stricter standard for declaring statistical significance? The authors of "Redefine Statistical Significance" write:

For a wide range of common statistical tests, transitioning from a P-value threshold of [0.05] to [0.005] while maintaining 80% power would require an increase in sample sizes of about 70%. Such an increase means that fewer studies can be conducted using current experimental designs and budgets. But Figure 2 shows the benefit: false positive rates would typically fall by factors greater than two. Hence, considerable resources would be saved by not performing future studies based on false premises. Increasing sample sizes is also desirable because studies with small sample sizes tend to yield inflated effect size estimates, and publication and other biases may be more likely in an environment of small studies. We believe that efficiency gains would far outweigh losses.

They are careful to say that in some disciplines, even the half-percent standard for statistical significance is not strict enough:

For exploratory research with very low prior odds (well outside the range in Figure 2), even lower significance thresholds than 0.005 are needed. Recognition of this issue led the genetics research community to move to a “genome-wide significance threshold” of 5×10^{-8} over a decade ago. And in high-energy physics, the tradition has long been to define significance by a “5-sigma” rule (roughly a P-value threshold of 3×10^{-7} ). We are essentially suggesting a move from a 2-sigma rule to a 3-sigma rule.

Our recommendation applies to disciplines with prior odds broadly in the range depicted in Figure 2, where use of P < 0.05 as a default is widespread. Within those disciplines, it is helpful for consumers of research to have a consistent benchmark. We feel the default should be shifted.

To me, one of the biggest benefits of this shift might be a greater ability for people to publish results that do not reject the null hypothesis at conventional levels. These results too, are an important part of the evidence base. The authors of "Redefine Statistical Significance" are careful to say that people should be able to publish papers that have no statistically significant results:

We emphasize that this proposal is about standards of evidence, not standards for policy action nor standards for publication. Results that do not reach the threshold for statistical significance (whatever it is) can still be important and merit publication in leading journals if they address important research questions with rigorous methods. This proposal should not be used to reject publications of novel findings with 0.005 < P < 0.05 properly labeled as suggestive evidence. We should reward quality and transparency of research as we impose these more stringent standards, and we should monitor how researchers’ behaviors are affected by this change. Otherwise, science runs the risk that the more demanding threshold for statistical significance will be met to the detriment of quality and transparency.

I myself was shocked when I read my own words above on the screen:

... people should be able to publish papers that have no statistically significant results: ...

That it seems shocking to say a paper should be publishable with no statistically significant results is a symptom of how corrupt the system has become. A stronger standard of statistical significance is needed in order to fight that corruption, both by making results that are declared statistically significant more likely to be true and by making results that are not declared statistically significant more publishable.

Update: Also useful is this article by Valentin Amrhei, Fränzi Korner-Nievergelt and Tobias Roth on "significance thresholds and the crisis of unreplicable research."

Western Values, According to Stephen Miller and Donald Trump

Toward the end of the period when I attended the Mormon Church (late 1999 and early 2000), I was still occasionally teaching Sunday School classes and more frequently teaching "Priesthood Meeting Elder's Quorum" classes. Despite views that varied significantly from Mormon orthodoxy at that point, I had no trouble teaching lessons in good faith. Assigned to teach from the text of a top Mormon leader's sermon, I would simply cross out the parts I disagreed with and teach the lesson based on what remained. And there was always something important that remained. I suppose some people might think what was remaining was trite, but I never did. The basics that people with diverging views agree on are often the deepest and meatiest truths of all.

My reaction to Donald Trumps speech in Poland on July 6, 2017 is similar. My disagreements with Donald Trump are profound—particularly on immigration: see for example

- "The Hunger Games" Is Hardly Our Future--It's Already Here

- Benjamin Franklin's Strategy to Make the US a Superpower Worked Once, Why Not Try It Again?

- Us and Them

- You Didn't Build That: America Edition

- Nationalists vs. Cosmopolitans: Social Scientists Need to Learn from Their Brexit Blunder

But I agree that what Donald Trump called "The West," deserves to be protected and defended, once one insists that anyone who accepts the values and principles of "The West" thereby becomes part of "The West," regardless of their national origin. (See my evocation of the principle of openness to newcomers in "'Keep the Riffraff Out!'")

And what are those values? Donald Trump's chief speechwriter Stephen Miller wrote a beautiful passage that were delivered in the Remarks by President Trump to the People of Poland | July 6, 2017:

We write symphonies. We pursue innovation. We celebrate our ancient heroes, embrace our timeless traditions and customs, and always seek to explore and discover brand-new frontiers.

We reward brilliance. We strive for excellence, and cherish inspiring works of art that honor God. We treasure the rule of law and protect the right to free speech and free expression.

We empower women as pillars of our society and of our success. We put faith and family, not government and bureaucracy, at the center of our lives. And we debate everything. We challenge everything. We seek to know everything so that we can better know ourselves.

And above all, we value the dignity of every human life, protect the rights of every person, and share the hope of every soul to live in freedom. That is who we are. Those are the priceless ties that bind us together as nations, as allies, and as a civilization.

Where "God" is mentioned, I need to interpret the passage according to my own view of God. (See "Teleotheism and the Purpose of Life.") And those with Western values are much more divided about the role of government than this passage recognizes. But otherwise I agree. And I hope you do, too, whatever your view of the man who wrote those words and the man who spoke them.

See also John O'Sullivan's thoughtful National Review article "Trump Defends the West in Warsaw"

Japan Shows How to Do Interest Rate Targets for Long-Term Bonds Instead of Quantity Targets

When the Fed began making large purchases of long-term Treasury bonds and mortgage-backed bonds—"QE"—I wondered why the Fed didn't announce an interest rate target for these bonds instead of a quantity target. An interest rate target for long-term bonds is the same thing as a price target, since there is a mechanical one-to-one relationship between prices and reported interest rates for bonds: by the present-value formula, higher prices are lower interest rates and lower prices are higher interest rates. One advantage of a interest rate target rather than quantity target for long-term bonds is that it would have given a better sense of the modest magnitude of stimulus provided by QE.

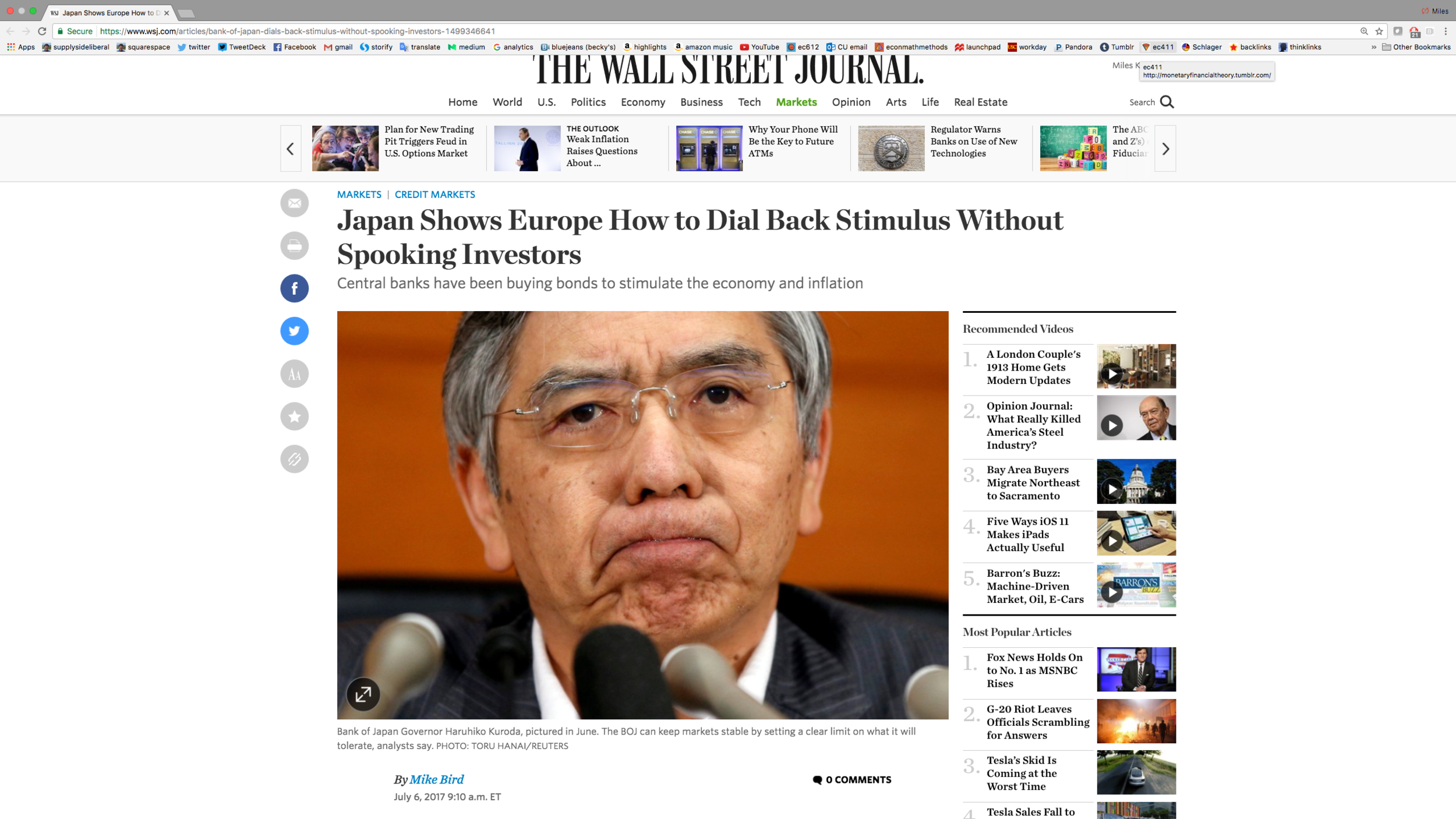

In his July 6, 2017 Wall Street Journal article, Mike Bird points out in his title another possible benefit of a price target for long-term bonds rather than a quantity target: "Japan Shows Europe How to Dial Back Stimulus Without Spooking Investors." The Bank of Japan calls these price/interest rate targets for long-term bonds "yield curve control." Mike's argument is to point to the 2013 US "Taper Tantrum" and to the European Central Bank's current communications difficulties:

“Draghi is discovering that narratives contrary to the one you want to get across can take hold in the market,” said Grant Lewis, head of research at Daiwa Capital Markets Europe. ...

Germany’s 10-year bund yields rose by 0.2 of a percentage point in five days, the largest jump since 2015’s “bund tantrum” when investors dumped bonds as they also anticipated less stimulus. ...

The BOJ can keep its markets stable by setting a clear limit on what it will tolerate, analysts say. In early February, when 10-year yields rose as high as 0.15%, the central bank offered to buy an unlimited volume of bonds at a yield of 0.11%, pushing yields back down.

“It’s clearly been easier for (BOJ chief Haruhiko) Kuroda. He’s stood up and said yields will be held at these levels. Try and beat me, I’ve got infinite resources,” Mr. Lewis added. “That’s actually allowed them to start purchasing less.”

One important consideration for an interest rate target for long-term bonds is that, along with the target for safe short-term rates that all major central banks continue to set, this would have effectively set a target for the spread between long-term bonds and the safe short rate. Unlike the short-term safe rate, which can be set in a very wide range (that in fact should be wider than current custom: see my paper "Next Generation Monetary Policy"), there are likely to be real limits on what the spread between short-term and long-term rates can be set at before the central bank ended up with zero or all of a category of long-term bonds. (It would be interesting if a central bank ever chose to do a big short on long-term government bonds.) Thus, an interest-rate target for long-term bonds needs to be kept in a range that implies a reasonable spread between safe short-term rates and long-term interest rates of a given category. But even if a central bank explicitly said it would revise its interest rate target if it ended up with zero or above 90% of a category of bonds, that target would still be quite powerful in its effects on markets.

The Scientific Approach to Monetary Rules

Nick Timiraos reported in the July 7, 2017 Wall Street Journal article shown above:

The Federal Reserve defended having the flexibility to set interest rates without new scrutiny from Capitol Hill in its semiannual report to Congress on Friday, warning of potential hazards if it were required to adopt a rule to guide monetary policy.

I think there is another approach that the Fed could take to a stress on monetary policy rules by Congress. Here is what I wrote in my new paper "Next Generation Monetary Policy," in the Journal of Macroeconomics:

Because optimal monetary policy is still a work in progress, legislation that tied monetary policy to a specific rule would be a bad idea. But legislation requiring a central bank to choose some rule and to explain actions that deviate from that rule could be useful. To be precise, being required to choose a rule and explain deviations from it would be very helpful if the central bank did not hesitate to depart from the rule. In such an approach, the emphasis is on the central bank explaining its actions. The point is not to directly constrain policy, but to force the central bank to approach monetary policy scientifically by noticing when it is departing from the rule it set itself and why.

I earnestly hope that any of you interested in monetary policy will read "Next Generation Monetary Policy." It distills all of my thoughts about monetary policy aside from my thoughts about negative interest rate policy (for which you should read the papers linked in my bibliographic post "How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide"), relating them where appropriate to the potential for negative interest rate policy. To whet your appetite, here is the abstract:

Abstract: This paper argues there is still a great deal of room for improvement in monetary policy. Sticking to interest rate rules, potential improvements include (1) eliminating any effective lower bound on interest rates, (2) tripling the coefficients in the Taylor rule, (3) reducing the penalty for changing directions, (4) reducing interest rate smoothing, (5) more attention to the output gap relative to the inflation gap, (6) more attention to durables prices, (7) mechanically adjusting for risk premia, (8) strengthening macroprudential measures to reduce the financial stability burden on interest rate policy, (9) providing more of a nominal anchor.

Freedom Under Law Means All Are Subject to the Same Laws

What does it mean to be free? If it means to have no legal restraints at all, then only one person at the apex of society can be free. If, instead, "freedom under law" is possible, it means to have the maximum amount of freedom that anyone in society has. That is, one can think of "freedom under law" as like a "most-favored-nation" clause: "freedom under law" is facing only the restrictions on one's behavior that everyone faces.

Interestingly, this definition "freedom under law" works for both "freedom under natural law" and "freedom under civil law." Here is John Locke's explanation of freedom under law in section 22 of his 2d Treatise on Government: “On Civil Government” (in Chapter IV "Of Slavery"):

THE natural liberty of man is to be free from any superior power on earth, and not to be under the will or legislative authority of man, but to have only the law of nature for his rule. The liberty of man, in society, is to be under no other legislative power, but that established, by consent, in the commonwealth; nor under the dominion of any will, or restraint of any law, but what that legislative shall enact, according to the trust put in it. Freedom then is not what Sir Robert Filmer tells us, Observations, A. 55. “a liberty for every one to do what he lists, to live as he pleases, and not to be tied by any laws:” but freedom of men under government is, to have a standing rule to live by, common to every one of that society, and made by the legislative power erected in it; a liberty to follow my own will in all things, where the rule prescribes not; and not to be subject to the inconstant, uncertain, unknown, arbitrary will of another man: as freedom of nature is, to be under no other restraint but the law of nature.

For freedom under civil law, the key clause is Robert Filmer's: "to have a standing rule to live by, common to every one of that society ...". This idea of everyone being subjected to the same laws was taken seriously in late 19th century, early 20th century US constitutional law as the prohibition against "class legislation." A prohibition against "class legislation" has the potential to put a barrier in the way of special interests lobbying for laws that will inhibit competitors.

Among US Supreme Court decisions, Lochner v. New York is one of the most famous, and one of the most criticized. Going into why would take this post too far afield, but I want to quote the discussion of "class legislation" in David Bernstein's book "Rehabilitating Lochner." The principle against class legislation came up in that litigation because the limitation on bakers' hours at the heart of the case was in important measure an attempt to benefit other bakers by disadvantaging newly immigrant bakers. Here is David:

The liberty of contract doctrine arose from two ideas prominent in late-nineteenth-century jurisprudence. First, courts stated that so-called "class legislation"-legislation that arbitrarily singled out a particular class for unfavorable treatment or regulation-was unconstitutional. Courts used both the Due Process and the Equal Protection clauses as textual hooks for reviewing class legislation claims. Indeed, the opinions were often unclear as to whether the operative constitutional provision was due process, equal protection, both, or neither. Second, courts used the Due Process Clause to enforce natural rights against the states. Judicially enforceable natural rights were not defined by reference to abstract philosophic constructs. Rather, they were the rights that history had shown were crucial to the development of Anglo-American liberty.

CLASS LEGISLATION ANALYSIS AND THE DUE PROCESS CLAUSE

Opposition to class legislation had deep roots in pre-Civil War American thought. After the Civil War and through the end of the Gilded Age, leading jurists believed that the ban on class legislation was the crux of the Fourteenth Amendment, including both the Equal Protection and Due Process clauses. Justice Stephen Field wrote in 1883 that the Fourteenth Amendment was "designed to prevent all discriminating legislation for the benefit of some to the disparagement of others." Each American, Field continued, had the right to "pursue his [or her] happiness unrestrained, except by just, equal, and impartial laws." Justice Joseph Bradley, writing for the Court the same year, declared that "what is called class legislation" is "obnoxious to the prohibitions of the Fourteenth Amendment." In Dent v. West Virginia, the Court even declared that no equal protection or due process claim could succeed absent an arbitrary classification.--' Influential dictum from Leeper v. Texas suggested that the Fourteenth Amendment's due process guarantee is secured "by laws operating on all alike."

The Supreme Court, however, interpreted the prohibition on class legislation quite narrowly. In 1884 it unanimously rejected a challenge to a San Francisco ordinance that prohibited night work only in laundries.-' Justice Field explained that the law seemed like a reasonable fire prevention measure, and that it applied equally to all laundries. The following year, a Chinese plaintiff challenged the same laundry ordinance, alleging that its purpose was to force Chinese-owned laundries out of business. Field, writing again for a unanimous Court, announced that-consistent with centuries of Anglo-American judicial tradition and prior Supreme Court cases-the Court would not "inquire into the motives of the legislators in passing [legislation], except as they may be disclosed on the face of the acts, or inferable from their operation. ..."' The Court's refusal to consider legislative motive severely limited its ability to police class legislation.

To my mind, the unwillingness to inquire into the motives of the legislators was a mistake. Looking for the motive to help one group even at the expense of another seems one of the easiest common-sense ways to figure out if something is class legislation. Nowadays, we recognize laws that are designed with the motive of disadvantaging African Americans as unconstitutional. This is that same principle applied to many classes of people. And even if the prohibition against class legislation were limited to a prohibition on legislation that would disadvantage the poorest of the poor, in line with John Rawls's recommendations in A Theory of Justice, it would be an extremely valuable principle. (For more thoughts on that score, see "Inequality Is About the Poor, Not About the Rich.")

Though defining "equality before the law" in particular cases is difficult, it seems to me that one way or another in all countries that believe in freedom and the rule of law, these ideas have a proper role in constitutional law:

"to have a standing rule to live by, common to every one of that society"

"the right to 'pursue his [or her] happiness unrestrained, except by just, equal, and impartial laws'"

"laws operating on all alike"

Addendum, August 4, 2019: As John L. Davidson points out, in general, inquiring into legislators’ motives is unworkable. The only time I think legislators’ motives should come into play in jurisprudence is when legislators’ motives were to do something constitutionally impermissible.

For links to John Locke posts on the previous 3 chapters of the 2d Treatise, see "John Locke's State of Nature and State of War."