Academic Medical Centers Get An F In Sharing Research Results →

via Joseph Kimball

A Partisan Nonpartisan Blog: Cutting Through Confusion Since 2012

via Joseph Kimball

Like me, Peter Sands and Larry Summers are not currently advocating negative interest rates for the United States. But they make a remarkable statement about the technical feasibility of the deep negative rates–not just the mild negative rates now seen in the eurozone, Japan, Switzerland, Sweden and Denmark. They write:

We take no position on the desirability of negative interest rates but are convinced by the arguments of JPMorgan, Miles Kimball and others that significantly negative rates can, if desired, be maintained without any limitation on currency through bank withdrawal fees. And we believe that for the foreseeable future there will be a role for cash in modern economies, though we would not be surprised if in many contexts its transactions costs come to exceed those of various electronic payment schemes.

Larry Summers was one of my professors as a graduate student at Harvard, so I take great pleasure in this affirmation. I sent him the link to my bibliographic post “How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide” not long ago, and am pleased that he has read some of what I have written on negative interest rate policy. Larry would not have agreed to have the op-ed say what it says unless he had thought carefully about my proposal from a technical point of view, within whatever time constraints he faced.

I should note, though, that Peter and Larry’s emphasis on withdrawal fees is based on a desire to talk about JPMorgan and me in the same sentence. I have primarily talked about withdrawal fees in order to argue that time-varying deposit fees at the cash window of the central bank are better. On pages 6 and 7 of “Breaking Through the Zero Lower Bound,” Ruchir Agarwal and I write:

Short of stamped currency or the abolition of paper currency, the government can discourage paper currency storage in essentially three ways, corresponding to the three steps needed to earn an interest rate of zero minus storage costs from paper currency: it can attack withdrawal of paper currency, storage of paper currency, or redeposit of paper currency.

To attack withdrawal of paper currency, the government could implement a restriction or fee on paper currency withdrawals from bank accounts (or in the extreme, end the printing of new paper currency, forcing people to make do with the existing stock). There are several disadvantages to this approach. First, it prevents withdrawal for spending as well as withdrawal for storage. Second, the ability to withdraw paper currency has great option value for people, which restrictions or fees on withdrawal would damage. Third, whether a withdrawal fee of a given size is adequate to prevent massive paper currency storage depends crucially not only on how negative interest rates are, but for how long they will be negative, which is difficult to know in advance. Fourth, with quantity restrictions on withdrawals—or fees high enough that the corner solution of withdrawing zero is often attractive—the effective price of paper currency would likely follow a jagged diffusion process as information and expectations evolved. Finally, people would still have an incentive to hoard the paper currency already in their possession, and to withdraw as much as possible in advance of the imposition of a withdrawal fee. This makes it more difficult to openly discuss and debate the imposition of a withdrawal fee.

To attack storage, the government could attempt to make storage of paper currency costly by taxing or prohibiting storage. There is a limit to how effective this can be, since storage of paper currency can be done in low-tech ways by anyone. Moreover, criminals already have experience in secret storage of paper currency. Thus, while storage of paper currency can be driven underground, it is hard to fully prevent. The ease of small-scale storage of paper currency by households, in particular, could lead to fewer funds left in demand deposits or savings accounts and hence to significant disintermediation even if commercial-scale paper currency storage could be successfully blocked.

The third option for the government is to implement a temporary fee on deposit or re-deposit of paper currency at the cash window of the central bank. Such a fee, when implemented in a time-varying manner on net deposits, creates an effective exchange rate between paper currency and electronic money, and allows the government to avoid the disadvantages of the first two options discussed above. The next section describes this mechanism in further detail.

In the next version of the paper, we will also need to talk about the Bank of Japan’s inadequately detailed but fascinating potential policy of using the interest on reserves policy to charge interest on paper currency that I discussed in “The Bank of Japan’s New Tool to Block Massive Paper Currency Storage.”

One other thing I should mention is that, unfortunately, Peter and Larry link to website for “Negative Interest Rate Policy as Conventional Monetary Policy” where readers will hit a paywall if they try to download the paper itself. Here is a link to the paper itself, which, as part of my deal with the National Institute Economic Review, I have full permission to post in full on my own websites.

In “Going Off the Paper Standard” I wrote that the first of 18 steps toward a smooth implementation of an electronic money policy was

Progress on this first step has been considerably faster than I expected.

Because the Economist doesn’t appreciate the power of deep negative interest rates to revive an economy and return quickly to positive interest rates–in a way mild negative rates cannot guarantee–it has turned to many other questionable proposals instead in February 20, 2016 cover story “The World Economy: Out of ammo? Central bankers are running down their arsenal. But other options exist to stimulate the economy” and the related article “Fighting the next recession: Unfamiliar ways forward–Policymakers in rich economies need to consider some radical approaches to tackling the next downturn.” Yesterday, I argued that “Helicopter Drops of Money Are Not the Answer.” Today, let me argue that higher inflation is not the answer. I gave the long version of the argument in “The Costs and Benefits of Repealing the Zero Lower Bound … and Then Lowering the Long-Run Inflation Target.” Today, let me try to give the short version.

Inflation has many costs. Among those costs, some of the most important are messing up microeconomic price signals and confusing people. This is a cost of the unit of account that people use to think about prices changing its value. Unless we want to confuse people, we should avoid changes in the value of the unit of account. As Greg Mankiw points out in his textbooks, the idea that the unit of account should have a constant value–or as constant a value as we can reasonably make it have–is akin to the idea that we want a meter to stay the same length and a kilogram to stay the same weight from one year to the next. To alter our weights and measures every year would have many costs stemming from the confusion it would cause.

Similarly, having the unit of account change value has many costs stemming from the confusion it causes–not all of which are captured in the usual models of the costs of inflation. I worry, for example, that people saving for retirement will think they are on track to be better prepared for retirement than they really are because they are tempted to think in terms of asset returns that are unadjusted for inflation. I am sure this confusion doesn’t affect everyone, just as I am sure that it does affect some people–and I think, unfortunately many people. I know that inflation confuses the US Congress, since large parts of the tax code are unadjusted for inflation. Inflation even confuses aspects of the economic debate where one might have thought it wouldn’t matter. The income of the top 1% of the income distribution is a remarkably high fraction of the total however the calculation is made. But that fraction is somewhat overstated whenever the asset returns used in those income calculations are not adjusted for inflation–a mistake that is all too common. And as Thomas Piketty points out in Capital in the Twenty-First Century, inflation makes it hard for us to understand novels like those of Jane Austen, as monetary values that had a very clear meaning for people back then have no clear meaning for modern readers.

The bottom line is that we should avoid inflation in the unit of account. The interesting thing to realize is that those who are calling for higher inflation (Such as Paul Krugman, Larry Ball, Brad DeLong and the Economist) are not really calling for higher inflation in the unit of account. They are calling for higher inflation relative to paper currency. It is only if the paper dollar, or paper euro or paper yen is the unit of account that inflation relative to the unit of account and inflation relative to paper currency are the same thing. Once a central bank takes a nation off the paper standard, it is possible to have the good inflation relative to paper currency without any of the bad inflation. That is, it is possible to have “inflation” relative to paper currency without any inflation relative to an electronic unit of account. In other words, once the electronic dollar, or electronic euro or electronic yen is the unit of account, the value of that unit of account can be kept the same, while the value of a paper dollar, paper euro or paper yen is made to decline whenever necessary in order to allow negative interest rates. See “An Underappreciated Power of a Central Bank: Determining the Relative Prices between the Various Forms of Money Under Its Jurisdiction” for how this works.

Indeed, under the kind of electronic money system I recommend, even inflation relative to paper currency would normally be a temporary thing. Thus, whatever minor costs it had (minor because the paper dollar or euro or yen would not be the unit of account), would be borne only during economic emergencies and for a time thereafterward. By contrast, those who advocate a higher inflation target without realizing it is possible to go off the paper standard are advocating paying the costs of the much more serious inflation relative to the unit of account every year, on and on indefinitely.

With all of this in mind, consider how unpleasant the Economist’s recommendation is compared to brief periods of going off the paper standard coupled with deep negative interest rates. “The World Economy: Out of ammo? Central bankers are running down their arsenal. But other options exist to stimulate the economy” sets out this idea:

Another set of ideas seek to influence wage- and price-setting by using a government-mandated incomes policy to pull economies from the quicksand. The idea here is to generate across-the-board wage increases, perhaps by using tax incentives, to induce a wage-price spiral of the sort that, in the 1970s, policymakers struggled to escape.

Moreover, the economist doesn’t seem to realize that this is at cross-purposes with a much better set of proposals to improve the supply-side of the economy:

Deregulation is another priority—and no less potent for being familiar. The Council of Economic Advisors says that the share of America’s workforce covered by state-licensing laws has risen to 25%, from 5% in the 1950s. Much of this red tape is unnecessary. Zoning laws are a barrier to new infrastructure. Tax codes remain Byzantine and stuffed with carve-outs that shelter the income of the better-off, who tend to save more.

Wonderful areas for improvement! But they need to be coupled with negative interest rates. Here is why: most supply-side improvements tend to reduce prices. As long as one can use deep negative interest rates, a reduction in prices is no problem. But if a central bank insists on staying on the paper standard, a lower growth rate of prices makes it harder to stimulate the economy.

I would choose supply-side improvements coupled with negative interest rates to ensure enough aggregate demand for all of the extra output any day before I would choose a higher inflation target our unit of account as a ham-handed way to do the work that should be done by going off the paper standard.

See links to everything I have written on negative interest rate policy organized in my bibliographic post “How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide.”

Links to “The World Economy: Out of ammo? Central bankers are running down their arsenal. But other options exist to stimulate the economy” and “Fighting the next recession: Unfamiliar ways forward–Policymakers in rich economies need to consider some radical approaches to tackling the next downturn”

Among major news outlets with a print component, I am happy to say I have had occasion to praise negative interest rate reporting in the Wall Street Journal and in the Globe and Mail:

The Wall Street Journal Gets It Right On Negative Interest Rate Policy, Thanks to Tommy Stubbington

The Globe and Mail Gets It Right on Negative Interest Rate Policy, Thanks to Ian McGugan.

The subtitle for the cover story for the February 20-26, 2016 Economist states their overall take quite clearly:

To give a further sense of that take on things, here are some key passages from that article:

One fear above all stalks the markets: that the rich world’s weapon against economic weakness no longer works. Ever since the crisis of 2007-08, the task of stimulating demand has fallen to central bankers. …

… Despite central banks’ efforts, recoveries are still weak and inflation is low. Faith in monetary policy is wavering.

In this article, negative interest rates are dismissed with this one sentence:

Negative interest rates in Europe and Japan make investors worry about bank earnings, sending share prices lower.

(On negative interest rates and bank earnings, see my posts “How to Handle Worries about the Effect of Negative Interest Rates on Bank Profits with Two-Tiered Interest-on-Reserves Policies” and “If a Central Bank Cuts All of Its Interest Rates, Including the Paper Currency Interest Rate, Negative Interest Rates are a Much Fiercer Animal.”)

The one other appearance of the word “negative” is in simply remarking

Borrowing has never been cheaper. Yields on more than $7 trillion of government bonds worldwide are now negative.

The Economist is wrong to dismiss negative interest rates. Indeed, I think the Economist will be unlikely to continue to dismiss negative interest rates as a powerful policy tool once one of their reporters takes the time to interview me, as they may sometime soon.

In the related article in the same issue, “Fighting the next recession: Unfamiliar ways forward–Policymakers in rich economies need to consider some radical approaches to tackling the next downturn,”the Economist says several negative things about negative rates without a change in paper currency policy, ignores the now well-heralded possibility of a negative paper currency interest rate (see how to deftly achieve a negative paper currency interest rate at the links in “How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide”) and has this to say about negative interest rates with the alternative paper currency of abolishing paper currency:

Since the existence of cash is a limit on how low interest rates can go, Andy Haldane, the chief economist of the Bank of England, and Ken Rogoff of Harvard University have proposed abolishing it altogether. But even if such radicalism were to prove feasible in a few countries, its effects might be limited. Savers would find alternative stores of value, such as precious metals or foreign banknotes, or pass on the cost of having money in the bank to others by making payments early.

The Economist, like John Cochrane (1, 2), is totally wrong about this. As my brother Chris and I point out in “However Low Interest Rates Might Go, the IRS Will Never Act Like a Bank,” it is almost impossible for anything but an unlimited opportunity to lend to the government at a zero interest rate to create a zero lower bound either or both because

most possible assets have a fluctuating price and therefore cannot provide a safe return, nor is there anything to prevent the price being big up high enough to generate a negative expected return, and

all other opportunities to earn a zero interest rate in a negative interest rate environment would be exhausted long before investors had found a home for all of the assets they wanted a safe zero interest rate for.

And as for foreign assets, as I discuss in “Could the UK Be the First Country to Adopt Electronic Money?” the desire to purchase foreign assets when domestic assets are earning a negative return is part of the transmission mechanism, since it induces capital flows that in turn generate additional net exports. This is a feature of negative interest rate policy, not a bug. And in any case, it is not a concern for the world as a whole, to the extent the world as a whole turns to negative interest rates.

Instead of monetary policy, the Economist looks in important measure to some form of fiscal policy to provide economic stimulus, writing

The good news is that more can be done to jolt economies from their low-growth, low-inflation torpor (see Briefing). Plenty of policies are left, and all can pack a punch. The bad news is that central banks will need help from governments. Until now, central bankers have had to do the heavy lifting because politicians have been shamefully reluctant to share the burden. At least some of them have failed to grasp the need to have fiscal and monetary policy operating in concert. Indeed, many governments actively worked against monetary stimulus by embracing austerity.

I am not so positive about fiscal policy. In “Narayana Kocherlakota Advocates Negative Rates and Criticizes the Conduct of US Fiscal Policy,” conscious of the power of deep negative interest rates to stimulate the economy, I write:

I tend to think that monetary policy should be used to stabilize the economy, not fiscal policy. Once monetary policy does its job, if the medium-run natural rate of interest is still low, then we should undertake more government investment. (See “The Medium-Run Natural Interest Rate and the Short-Run Natural Interest Rate.”) And we should undertake crucial government investments even if interest rates are high after the economy recovers. But it is just too hard to time government investment effectively in order to stabilize the economy.

Monetary policy has a lag of 6 to 12 months in its effects. Even so, it is much nimbler than government investment. Private investment and imports and exports can’t turn on a dime; hence the 6 to 12 month delay in the effect of monetary policy. But government investment typical takes even longer than that to turn around.

Using monetary policy as it should be used, aggregate demand is no longer scarce. Monetary policy can provide all the firepower needed.

The Economist has a long list of policy prescriptions, among which using deep negative interest rates (combined with an appropriate paper currency policy) is conspicuously missing. But among all of the policy prescriptions, a helicopter drop of money takes pride of place as the first to get a full paragraph treatment:

The time has come for politicians to join the fight alongside central bankers. The most radical policy ideas fuse fiscal and monetary policy. One such option is to finance public spending (or tax cuts) directly by printing money—known as a “helicopter drop”. Unlike QE, a helicopter drop bypasses banks and financial markets, and puts freshly printed cash straight into people’s pockets. The sheer recklessness of this would, in theory, encourage people to spend the windfall, not save it.

The Economist discusses a helicopter drop further in the related article “Fighting the next recession: Unfamiliar ways forward–Policymakers in rich economies need to consider some radical approaches to tackling the next downturn”:

One way to raise expectations of inflation and boost aggregate demand is for a central bank and its finance ministry to collude in printing money to pay for public spending (or tax cuts). Such shenanigans are not possible in the euro zone, where the ECB is forbidden by treaty from buying government bonds directly. Elsewhere they might work as follows: the government announces a tax rebate and issues bonds to finance it, but instead of selling them to private investors swaps them for a deposit with the central bank. The central bank proceeds to cancel the bonds, and the government withdraws the money it has on deposit and gives it to citizens. “Helicopter money” of this sort—named in honour of a parable told by Milton Friedman, a famous economist—is as close as you can get to raining cash from a clear blue sky like manna from heaven, untouched by banks and financial markets.

Such largesse is, in effect, fiscal policy financed by money instead of bonds. It is conceivable that a bond-financed fiscal tax cut might in fact be cheaper to finance: although cash has a zero yield, medium-term bonds in Japan and in much of Europe have negative yields. But the unaccustomed drama—indeed, the apparent recklessness—of helicopter money could increase the expected inflation rate, encouraging taxpayers to spend rather than save. It is not something to rush into, or to try prophylactically; but in the midst of a global financial crisis, or a deep recession, it would have much to recommend it. If it were co-ordinated by a group of rich countries, all the better.

A related idea is to cancel a portion of the sovereign bonds purchased by central banks, ostensibly cutting public debt at a stroke. It would have the drawback, as would helicopter money, of leaving the central bank technically bankrupt, since its liabilities (money) would exceed its assets (bonds). But since most central banks are backed by national treasuries, this ought not to matter much. A bigger worry is that it is hard to know in advance what effect monetisation would have. Bond markets could panic about an inflationary surge, driving yields through the roof. Or they might just shrug the whole thing off. After all, the central bank could issue fresh bonds to soak up the excess money if things eventually got out of hand.

The Economist points clearly to the one case in which a massive helicopter drop might be called for: if it became necessary to have the government give away so much money that people would be convinced there was no way the government could ever sell enough bonds to soak that money up. But this is clearly a drastic measure. Convincing the markets that the government will surely go bankrupt and have to explicitly default on its debt unless their is massive inflation is a counsel of desperation. By contrast, despite all of the hyperventilating reporting, once it is coupled with an appropriate paper currency policy, negative interest rate policy is, in its main effects, simply conventional monetary policy continued into the negative region. (See my National Institute Economic Review paper “Negative Interest Rate Policy as Conventional Monetary Policy” and “If a Central Bank Cuts All of Its Interest Rates, Including the Paper Currency Interest Rate, Negative Interest Rates are a Much Fiercer Animal.”)

Why Helicopter Drops the Government Can Afford are Not the Answer

What about helicopter drops that won’t lead to government bankruptcy or runaway inflation? Here the Economist also provides a clue to why such helicopter drops are an inferior policy. Printing money and sending it to people is equivalent to printing money to buy Treasury bills and then selling those Treasury bills to raise funds to send to people. Written as an equation:

printing money and sending it to people =

printing money to buy Treasury bills

+ selling Treasury bills to get funds that are sent to people

This is an interest equation, because each of the terms in the equation has a name. Here is the same equation, with the usual policy names attached:

helicopter drop = standard open market operation + tax rebate

This equation takes some of the mystique out of helicopter drops. Let’s see what it means. First, this equation is consistent with the discussion above. If the aim is to create doubts about the government’s ability to pay its debts without massive inflation, then the easiest way to sell enough Treasury bills to get funds for a big enough tax rebate to do so is by printing money and having the central bank buy those Treasury bills.

On the other hand, if the size of the tax rebates is an amount the government could borrow enough for even without central bank financing, then adding standard open market operation of printing money to buy Treasury bills may or may not add much. If printing money to buy 3-month Treasury bills stimulates the economy, then the central bank can simply do this as what everyone considers totally standard monetary policy, without the tax rebate. If at any point printing money to buy 3-month Treasury bills ceases to do much of anything, then the extra stimulus beyond that totally standard monetary policy action is the effect of a tax rebate.

To the extent a helicopter drop has the same effect as a tax rebate because (a) the amount at issue is affordable and (b) open market purchases of Treasury bills have little stimulative effect, the question then is how attractive tax rebates are. The answer is: not attractive at all. I have argued at length that tax rebates are strictly inferior a policy I call “National Lines of Credit.” I introduced this policy in a working paper heralded by a blog post of the same name:

Here is the abstract for that paper:

Abstract: In ranking fiscal stimulus programs, it is useful to focus on the ratio of extra aggregate demand to extra national debt that results. This note argues that (because of repayment after the end of a recession) “national lines of credit”–that is, government-issued credit cards with countercyclical credit limits and favorable interest rates—would generate a higher ratio of extra aggregate demand to extra national debt than tax rebates. Because it involves government loans that are anticipated in advance to involve some losses and therefore involve a fiscal cost even after efforts to minimize losses, such a policy lies between traditional monetary policy and traditional fiscal policy.

Here are some other blog posts (with the most important at the top) on “National Lines of Credit” (which in the US context I also call “Federal Lines of Credit”):

More Muscle than QE: With an Extra $2000 in Their Pockets, Could Americans Restart the US Economy?

Why George Osborne Should Give Everyone in Britain a New Credit Card

Joshua Hausman on Historical Evidence for What Federal Lines of Credit Would Do

Joshua Hausman: More Historical Evidence for What Federal Lines of Credit Would Do

Monetary vs. Fiscal Policy: Expansionary Monetary Policy Does Not Raise the Budget Deficit

Preventing Recession-Fighting from Becoming a Political Football

How Italy and the UK Can Stimulate Their Economies Without Further Damaging Their Credit Ratings

About Paul Krugman: Having the Right Diagnosis Does Not Mean He Has the Right Cure

Noah Smith Joins My Debate with Paul Krugman: Debt, National Lines of Credit, and Politics

The Deep Magic of Money and the Deeper Magic of the Supply Side

Bill Greider on Federal Lines of Credit: “A New Way to Recharge the Economy”

Miles on HuffPost Live: The Wrong Debate and How to Change It

Reply to Mike Sax’s Question “But What About the Demand Side, as a Source of Revenue and of Jobs?”

What to Do When the World Desperately Wants to Lend Us Money

Link to Ian McGugan’s author page at the Globe and Mail

Ian McGugan of Canada’s premier newspaper, the Globe and Mail, interviewed me last Tuesday evening, February 16, 2016. That interview is reflected in his article “Negative Rates: Recipe for Growth or Desperate Gimmick” (paywalled). Ian gives an excellent treatment of the issues surrounding negative interest rate policies, quite appropriately emphasizing the current controversy as a “brawl.” On my side, which views negative interest rates as a crucial part of the monetary policy toolkit, he first quotes Narayana Kocherlakota’s blog post that I discuss in “Narayana Kocherlakota Argues That Negative Interest Rates Should Be Seen as Part of Conventional Monetary Policy. ” Ian McGugan sets up the quotation from Narayana thus:

Defenders of NIRP insist the program simply needs time to take hold. The real problem, they maintain, is the timid way that subzero policies have been rolled out.

Central banks, according to these proponents, should trumpet negative rates. Policy makers should vow – loudly and aggressively – to stick with NIRP until expectations have been reshaped and the economy is booming once again.

“Here’s the wrong way [for central banks] to communicate: Keep saying that negative is a purely emergency setting that will be abandoned shortly,” writes Narayana Kocherlakota, a former president of the Minneapolis Federal Reserve Bank who now teaches economics at the University of Rochester. “Here’s the right way to communicate: Keep saying that all available tools, including negative interest rates, will be used as is needed to return employment and inflation to desirable levels as rapidly as possible.”

Later, on the pro side, Ian quotes Nick Rowe:

“There has never been anything wrong in theory with charging negative rates,” says Nick Rowe, a professor of economics at Carleton University and an authority on monetary policy. “The objection was always this notion that people would just withdraw their money from the bank and go to cash, which pays zero interest but at least doesn’t impose a negative rate.”

However, a rush to paper money hasn’t materialized in the countries that have imposed negative rates, perhaps because the rates have been only mildly negative. …

Economists acknowledge that it’s administratively tricky to impose negative rates, but they don’t see the problems as insurmountable. Prof. Rowe argues that the important factor for any lender is the spread between its deposit rates and its lending rates, not whether those rates happen to be negative or positive.

Finally, on the pro side, Ian quote me:

“It’s relatively simple for a bank to adjust its business model to still make money with negative rates,” agrees Miles Kimball, a professor of economics at the University of Michigan. A long-time advocate for negative rates, he argues that policy makers should be far more aggressive in pushing down lending costs.

He says banks should realize their real enemy is the current new normal of anemic growth. The failure of the global economy to revive after years of zero-rate therapy is conclusive evidence that stronger medicine is necessary, he argues. “If you don’t take the right dosage of a drug, it doesn’t work.”

Both Europe and Japan should immediately push rates even lower, he says. While negative rates of, say, minus 2 per cent or even lower might shock observers at first, they would be in keeping with what history tells us is necessary.

In the past, central banks have often dropped rates by six percentage points or more to bring about recoveries. The only way to achieve a similar effect in today’s low-rate environment would be to take rates strongly negative.

Wouldn’t that unfairly punish ordinary mom-and-pop savers? Not at all, he says. “Savers would be far better off if we had brief periods of deep negative rates that would quickly restore growth, rather than long periods – like now – of near-zero rates, where nobody makes any real return for years.”

To be sure, not everyone might welcome the details of how Prof. Kimball plans to lower interest rates far below zero. To avoid the possibility that savers would flock to cash rather than take a beating on the “electronic” currency in their bank account, he would impose a discount on folding money.

“Paper currency could still continue to exist, but prices would be set in terms of electronic dollars (or abroad, electronic euros or yen), with paper dollars potentially being exchanged at a discount compared to electronic dollars,” he writes.

A situation where paper money might not be worth its face value would be disturbing for most people and it’s not the only disquieting aspect of a subzero strategy. …

Prof. Kimball acknowledges that there are big psychological barriers to negative rates, and suggests there would be ways to get around the worst side effects. Ideally, he says, negative rates would apply mostly to institutional and business accounts while leaving most ordinary savers and borrowers untouched. “Our monetary system does change every 50 years or so, so change is possible,” he says. “People never thought we would go off the gold standard, but we did.” As disruptive as negative rates might seem, he argues they are vital to restart growth. Most of Bay Street would bitterly disagree. Whichever side wins this argument is likely to shape the course of monetary policy for years to come.

(Bay Street is Canada’s counterpart to Wall Street.)

Ian’s article is a great source for many of the arguments against negative rates as well. Ian does not stint in reporting those con arguments. I should deal with those arguments more on another occasion. For now, let me emphasize that I have responded to the worry that negative interest rates will hurt bank profits in my “How to Handle Worries about the Effect of Negative Interest Rates on Bank Profits with Two-Tiered Interest-on-Reserves Policies” and again in “If a Central Bank Cuts All of Its Interest Rates, Including the Paper Currency Interest Rate, Negative Interest Rates are a Much Fiercer Animal.”

Finally, for those of us who get remarkably little Canadian news because our reading focuses on news outlets in Canada’s neighbor, the United States of America, let me note this from Ian’s article:

Stephen Poloz, Governor of the Bank of Canada, delivered a speech in December in which he mulled the potential for taking Canada’s key rate to minus 0.5 per cent, although he emphasized such a move wasn’t imminent.

Ian covers a lot of ground in his article. It sets a very positive example for negative interest rate journalism.

I owe a great debt to Makoto Shimizu. Without any compensation, he has maintained the Japanese language version of this blog–including arranging for translations and doing the bulk of the translation himself. I know that Makoto does this because he believes as I do that appropriate negative interest rate policy is the way for Japan to escape its version of secular stagnation and for other nations to avoid falling into secular stagnation.

With Makoto’s permission, I want to bring you in on an email he sent me giving an important perspective on the Bank of Japan’s new paper currency policy of effectively giving a negative interest rate to cumulative net cash withdrawals by private banks from the Bank Of Japan’s cash window. I posted “The Bank of Japan’s New Tool to Block Massive Paper Currency Storage” on that paper currency policy on February 8, 2016. I strongly recommend that you read “The Bank of Japan’s New Tool to Block Massive Paper Currency Storage” before trying to understand what is below in today’s post. You will need the background. In an update to “The Bank of Japan’s New Tool to Block Massive Paper Currency Storage,” I wrote:

Update 1: A reader points out that the Bank of Japan’s statement of its policy above can easily be interpreted as applying only to a bank’s own holdings of paper currency, which would not include paper currency it passed on to customers. (Many people have, in fact, interpreted it that way.) In that case, this would be a charge for storage of paper currency rather than a charge for cumulative net withdrawals of paper currency by banks. If that is the right interpretation, I am glad I misunderstood the statement so I could see the interesting possibility of a charge on cumulative net withdrawals. But I am also glad to be corrected about what the actual current policy is.

In the event, if a bank made large paper currency withdrawals to pass paper currency on to customers, I suspect the Bank of Japan would try to do something to discourage that flow. Since the Bank of Japan is making the policy itself (and there is a tradition in Japan of administrative discretion) a private bank should worry about what the Bank of Japan would do if the private bank became a conduit for a large amount of paper currency to customers.

But Makoto gives an account more in line with my first interpretation. Here is what he wrote to me, very lightly edited:

Hi, Miles. Most of the responses in the Japanese media to BOJ’s negative interest rate policy including from academic economists were negative as I anticipated (and I guess somewhat you may, too).

Soon after the BOJ’s announcement and before reading your post “The Bank of Japan’s New Tool to Block Massive Paper Currency Storage,” I had a meeting with the former Deputy Governor of BOJ (2003-2008), Kazumasa Iwata at the Japan Center for Economic and Research. Now he is the president of the center, and the most active supporter for the negative interest policy in Japan as far as I know.

http://www.jcer.or.jp/eng/about/index.html

In the meeting, I talked about negative interest rate policy with him and other staff members at the center. One thing I pointed out related to the effective negative rate on cumulative cash withdrawals that you wrote about was that it would promote negative interest rates on private deposits since the private banks would try to influence any cash withdrawals their depositors made.

At the time, took the BOJ statement to refer to “cash holdings.” Then, Ikuko Samikawa, a staff member pointed out that it is hard for the BOJ to know the exact cash holdings in the private bank since there is no distinction between cash and other cash equivalents in the financial statement. So it will be difficult for the negative interest rate to “apply only to a bank’s own holdings of paper currency.” Kazumasa Iwata said what the BOJ does would be to monitor the net cash withdrawal at the cash window. I think this was similar to what you argue in the post.

After the meeting, I made an inquiry through the Bank of Japan’s website BOJ about this paper currency policy. Takuto Ninomiya of BOJ answered me. He said something like: “There are no exact figures in the scheme so far.” He also attached a file giving an official statement saying the same thing. So it does not sound like a policy “rule.” The Bank of Japan seems to be making a vague statement–maybe even a bluff–to discourage private banks from withdrawing too much paper currency.

On reflection, I think the effective negative interest rate on cumulative net paper currency withdrawals from the cash window is similar to a withdrawal fee at cash window since the banks face a negative interest rate for cash that would prevent a profitable arbitrage of borrowing to stock up on paper currency. However, an effective negative interest rate on cumulative net cash withdrawals is better than a withdrawal fee since the payment is more appropriate. Although the scheme is similar to the deposit fee you propose in having an appropriate payment for additional cash withdrawals, it doesn’t cover cash already in circulation.

Link to the Wikipedia article for “Restoring the Lost Constitution: The Presumption of Liberty”

In “How and Why to Expand the Nonprofit Sector as a Partial Alternative to Government: A Reader’s Guide” I organize links about my proposal to expand the nonprofit sector instead of government. When I tweet and blog about this proposal, a common reaction from some readers–as you can see in my Twitter discussions with Daniel Altman (1, 2)–is that this gets in the way of the community’s right to determine collectively what it priorities should be. John Stuart Mill, in the 3d paragraph of the “Introductory” to On Liberty, expresses this idea memorably, in order to take it down in later paragraphs.

A time, however, came, in the progress of human affairs, when men ceased to think it a necessity of nature that their governors should be an independent power, opposed in interest to themselves. It appeared to them much better that the various magistrates of the State should be their tenants or delegates, revocable at their pleasure. In that way alone, it seemed, could they have complete security that the powers of government would never be abused to their disadvantage. By degrees this new demand for elective and temporary rulers became the prominent object of the exertions of the popular party, wherever any such party existed; and superseded, to a considerable extent, the previous efforts to limit the power of rulers. As the struggle proceeded for making the ruling power emanate from the periodical choice of the ruled, some persons began to think that too much importance had been attached to the limitation of the power itself. That (it might seem) was a resource against rulers whose interests were habitually opposed to those of the people. What was now wanted was, that the rulers should be identified with the people; that their interest and will should be the interest and will of the nation. The nation did not need to be protected against its own will. There was no fear of its tyrannizing over itself. Let the rulers be effectually responsible to it, promptly removable by it, and it could afford to trust them with power of which it could itself dictate the use to be made. Their power was but the nation’s own power, concentrated, and in a form convenient for exercise. This mode of thought, or rather perhaps of feeling, was common among the last generation of European liberalism, in the Continental section of which it still apparently predominates. Those who admit any limit to what a government may do, except in the case of such governments as they think ought not to exist, stand out as brilliant exceptions among the political thinkers of the Continent. A similar tone of sentiment might by this time have been prevalent in our own country, if the circumstances which for a time encouraged it, had continued unaltered.

The trouble with such a concept of “the will of the people” is that each individual is different. Let me give a simple example from Randy Barnett’s discussion in Restoring the Lost Constitution: The Presumption of Liberty of the idea of the “consent of the people” in the ratification of the US Constitution. An important minority who had no opportunity to consent to the US Constitution were the enslaved people of African descent who might well have had objections to certain provisions of the US Constitution. If they had been allowed to vote on the US Constitution’s ratification, but had been outvoted by the majority, would that really have made the US Constitution’s provisions accommodating the continuation of slavery OK? If, like me, you answer no, then the opportunity to vote alone is not enough to make it OK for the government to do whatever the “will of the people” that comes from majority voting suggests.

What kinds of constraints on democracy should be made in the interests of justice? There are two primary competing notions. The first is the idea of freedom. The second is the idea of equality. The place where these two principles pull in the same direction is whenever the rich and powerful use the government to restrict the freedom of the poor and weak. The excuse is often to disenfranchise the poor and the weak by saying that they are outside the community and don’t deserve to have their interests represented in policy. But sometimes the interests of the poor and the weak are trampled despite their having the opportunity to vote on those issues. I discuss several issues in this category in “Keep the Riffraff Out!”

One area where otherwise decent people often have no qualms about oppressing the poor and the weak is in prevent the building of housing in their neighborhood that is affordable by the poor (whether it is affordable by being subsidized or affordable simply because it is built in a high-density way). Restrictions on the construction of affordable housing in one’s neighborhood may in some sense be “the will of the people” who happen to live there already but is it just?

(As an aside, let me say that simply being poor does not mean that one should be able to get away with bad behavior. To the extent that some people are poor precisely because they have behavioral problems–a common fear of those who object to affordable housing in their neighborhood–it is appropriate to plan for and commit to additional law enforcement and social services resources to dealing with those behavioral problems when affordable housing is built.)

In Japan, the Bank of Japan failed to prepare the public adequately for negative interest rates. They would have had more public understanding if they had already begun referring journalists and the Japanese public to the translations of my key posts into Japanese that Makoto Shimizu has posted on supplyideliberaljp.tumblr.com. The Bank of Japan should begin pointing Japanese language readers to supplyideliberaljp.tumblr.com immediately.

By contrast, in the US, the famed investment bank JP Morgan is already helping to prepare the American public for negative interest rates that may still be years off in the future. JP Morgan analysts Malcolm Barr, Bruce Kasman and David Mackie of JP Morgan wrote a remarkable report I would love to get in my hands but so far only know from news accounts. And JP Morgan’s Chief Economist Michael Feroli gave a fascinating interview on camera with Bloomberg Business about negative rates that you can see at the top of the piece linked here, and immediately below:

Link to “How Low Can Central Banks Go? JPMorgan Reckons Way, Way Lower” by Simon Kennedy

Here are some key quotations from the JP Morgan report that are drawn from Mark Melin’s ValueWalk article “Negative Interest Rates Could Go as Low as 4.5%: JPMorgan Shocker” showing how bullish JP Morgan now seems to be about negative rates:

… the incentive to move into cash will be influenced not only by the level of the policy rate but also by how long negative rates are expected to persist. This suggests that the lower nominal bound is below zero, with the exact level determined by the perceived costs and benefits of moving into cash. …

There has been no sign of banks or others starting to hoard physical cash in order to avoid a negative interest charge. …

… [there] has not been a huge asymmetry in the pass through of lower policy rates to retail deposit and lending rates. …

[negative interest rates] could open up a powerful new tool for monetary policy.

Malcolm Barr, Bruce Kasman and David Mackie’s read on the substantial success of European banks in passing through lower interest rates to both deposit and lending rates is important in the light of recent controversies about the effect of negative interest rates on bank profits. In addition, any serious reporting on the effect of negative interest rates on bank profits needs to mention my proposal in

that central banks use the details of their formulas for interest on reserves to effectively subsidize banks for continuing to keep zero interest rates for small household accounts while encouraging banks to pass on negative rates to commercial accounts and large personal accounts. Because most households have relative small bank balances, it is easy to have 80 to 90% of all households shielded from negative rates, while 80 to 90% of all funds are subject to negative rates.

The aggregate demand effects of negative interest rates do not depend in any important way on regular households seeing negative interest rates on their deposits. The oomph from negative interest rates comes from bring down interest rates for auto loans, mortgages, and business loans, and from encouraging businesses that are sitting on large piles of cash to pursue new business projects with that cash on pain of seeing those piles of cash sitting around doing nothing shrink if they don’t. I wrote a children’s story a while back on how it works:

Gather ’round, Children, Here’s How to Heal a Wounded Economy.

Without a big staff to help me crunch numbers, in monetary policy recommendations, I have been trying to stick to easy judgments, like my recommendation that the ECB immediately cut its target rate to -2%, making the necessary adjustments in paper currency policy.

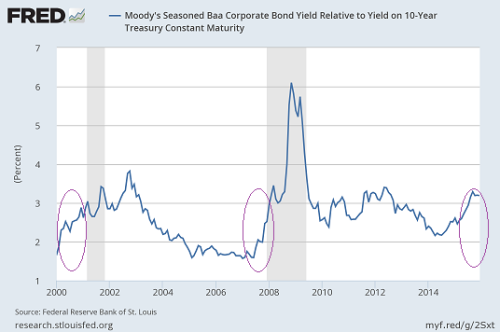

One other easy judgment is to say that a central bank’s target rate should routinely–and fairly mechanically–respond to risk premia in the bond market. To be more specific, the Fed should offset something like 80% of any rise in credit spreads like the one shown above between the 10-year corporate Baa rate relative to the 10-year Treasury bond rate. The basic reason is that the rate at which companies can borrow is crucial to the levels of investment that drive the business cycle. So it makes sense to keep corporate borrowing rates and wholesale commercial rates in a good range. To spell out what I mean by saying the adjustment for risk premia should be done “fairly mechanically,” I recommend that central banks state their target short-term safe rates (such as the Fed funds rate or the repo rate) not as a number, but as a number minus .8 times a suitable credit spread so that the adjustment would take place automatically even in between meetings of the monetary policy committee.

I wrote about this issue before in my column “Meet the Fed’s New Intellectual Powerhouse”:

Too much discussion of monetary policy has proceeded under the fiction that there is only one interest rate. As soon as one recognizes that there are as many different interest rates as there are types of assets, an obvious question arises: “Which interest rates give the best idea of the cost of borrowing for the home-building, consumer spending, and business investment that drive aggregate demand for the economy?” The obvious—and correct—answer is that it is rates for mortgages, consumer loans, and loans to businesses (of which the lending represented by corporate bonds is an important part) that best represent the borrowing costs that matter for aggregate demand.

So even when the Fed states its policy in terms of the safe fed funds rate, it should be looking past that safe rate to the mortgage rates, consumer-loan rates, and corporate borrowing rates that result. Even before considering the risk of a financial crisis, the Fed should react to an increase in bond risk premiums almost one-for-one by a reduction in the safe rate, and should react to a narrowing of bond risk premiums almost one-for-one by an increase in the safe rate. (The reason I write “almost” one-for-one is that the risk premium has an effect on savers as well as on borrowers, but evidence suggests that savers are not very sensitive to interest rates, so it is the effect of the key rates on borrowers that is of greatest concern.)

This principle is one that shows up in formal models and simulations of optimal monetary policy. See for example Vasco Curdia and Michael Woodford’s, “Credit Spreads and Monetary Policy.” As I said as a conference discussant of their related paper, I think Vasco Curdia and Michael Woodford understate the extent to which a central bank should offset credit spreads, since they do not adequately account for how much more sensitive borrowing is to interest rates than lending is. (You can see the Powerpoint file for my discussion here.) In any case, it would be a significant mistake for a central bank not to offset more than half of a measure of credit spreads by cutting the safe government rate when the spread between safe government rates and corporate rates goes up. Above I suggested offsetting 80% of any rise in credit spreads by a fall in the target rate, but this number should be carefully studied in formal models of optimal monetary policy. The right number may easily be closer to 90%. When I say “studied in formal models of optimal monetary policy” it should be obvious that a quantitative answer worth taking seriously can only come out of a model that explicitly models investment, not from a model with only nondurable consumption.

From the graph at the top, you can see that this point is one highly relevant to the current situation. To the extent the Fed and other central banks don’t have credit spreads fully built into the rules of thumb they use for monetary policy–or into more formal models of optimal monetary policy used for practical purposes, their interest rate decisions may be off target.

Although it is not 100% clear to me that the Fed has the wrong interest rate at the moment, I worry a lot that if news comes in that makes a lower interest rate the right thing to do that the members of the FOMC making decisions on interest rates will be slow to respond to that news by cutting rates. One of the more dangerous notions about monetary policy is that a central bank must by all accounts avoid losing face by reversing course on interest rate changes. (See my more detailed discussion here.) Following that twisted logic, the fact that the Fed raised rates once a few months ago would mean that it would not allow itself to cut rates again until the situation became truly dire–with all the costs to the economy that would ensue from not acting more promptly. It is crucial that the policy-makers at the Fed begin putting to rest the idea that reversing course is a terrible thing. Which makes more sense: responding promptly to news, or not responding promptly to news?

Link to “The Trouble With CoCos” on Bloomberg View

Let me reprise part of what I wrote in the preface to “Cetier the First: Convertible Capital Hurdles” and augment it with the wise words of the Bloomberg View editorial board on the topic of debt that are converted into equity (stock) upon a certain trigger (“contingent convertibles” or “CoCos”).

Here is what I wrote back in August 2013:

…the basic problem with convertible capital, bail-ins, and so on is that they all require a decision–either drawn out an painful, or sudden and painful–to force those who have theoretically accepted a risk to actually take a loss. By contrast, equity holders take losses and make gains continually, without everything hingeing on a decision to make some group take the loss. The automatic nature of taking equity losses and getting equity gains is both an advantage in itself and tends to make these capital gains and losses more continuous and less sudden than for convertible capital and “debt” in bail-ins.

Another way of putting the problem is that the moment when conversion threatens is typically seen as a crisis, even if the approach to that moment was gradual, while a simple decline in the price of common stock is seldom seen as a crisis unless it is a very large and sudden decline. This crisis atmosphere is both damaging to confidence in and of itself and a temptation for government to do a bailout–a bailout they would be much less tempted to do after a simple decline in stock price.

And here is the Bloomberg View Editorial Board on February 12, 2016:

The incident serves to reinforce concerns, expressed by various financial economists, that CoCo bonds may make investors in banks and their debt more apt to take flight when trouble looms. After all, if CoCos protect taxpayers, they do so at the expense of bank shareholders and bondholders. Moreover, CoCos are complicated instruments. In a time of stress, uncertainty over the conditions that trigger conversions may add to the sense of alarm.

Paradoxically, a panic of that kind might eventually call forth a government bailout – the very thing that CoCos are intended to prevent. …

These flaws underscore the case for simply requiring banks to finance themselves with more equity, which has the advantage of absorbing losses without any special triggers or added anxiety.

The problem with debt is that it is a bit of a pretense that there is not risk for the debt-holder. Given this pretense, debt-holders get alarmed when they are forced to face the reality of risk. Convertible debt does not escape this problem. The great virtue of common stock equity is that every day it goes up and down in price in a way that reminds its holders of the risk they face. Moreover, there is no obvious angle from which one can view common stock equity as risk-free. So stock-holders are made to face the reality of risk every day. They still may freak out at very large movements in price, but they become accustomed to substantial movements on a regular basis. Although in principle, one can think of bonds as just one more type of risky asset–one that is a bit more complex than stocks because of the complexity of default (and economists in their models often do imagine bonds in exactly that way), this is not always the way bond-holders view it. It is not good to set up a large group of asset-holders for freaking out because of a mismatch between the safety they think they are getting and the risk they are actually bearing.

It is much better to have truth in labeling by requiring that half of all the liabilities of a firm be labeled and treated as common stock, and only pretending (now a more nearly accurate pretense) that the other half of the liabilities are safe. That is what a 50% common stock equity does. That is the single most important policy to avoid financial crises.

As far the convertible bonds that are already in place, government authorities should act very much as if these convertible bonds were already converted in equity. It is no crisis for them to convert into common stock equity–that is what they should have been from the beginning. And anyone who thought their CoCo’s would be bailed out should be taught the reality of risk.

Not how different this is from sending a bank into bankruptcy–the bank’s operations are fine and continue to function. It is only those who made a bet that the bank was safer than it really was that pay the price, not the customers and commercial counterparties of the bank.

And if CoCo conversion makes it harder for banks to sell CoCo’s in the future, so much the better–it will make them more likely satisfy existing regulatory requirements by selling common stock equity, even if the regulators are sadly slow to insist on that as the way to satisfy capital requirements.

Update, October 27, 2019. Here is a link to an online article by Dennis Shirshikov: “Convertible Debt: The Ultimate Guide” that gives some context.

Link to pbs.org page for “Wolverine: Chasing the Phantom”

In “The Swiss National Bank Means Business with Its Negative Rates,” I wrote

There is a world of difference between a central bank that cuts some of its interest rates, but keeps its paper currency interest rate at zero and a central bank that cuts all of its interest rates, including the paper currency interest rate. If a central bank cuts all of its interest rates, including that paper rate, negative interest rates are a much fiercer animal.

At the top, I have tried to make this metaphor even more vivid with a still from a wonderful PBS documentary “Wolverine: Chasing the Phantom.” Wolverines, the mascot of the University of Michigan, are animals designed for snow and ice, and as tough as they come. The economic winter the world is struggling to get out of calls for an economic policy as tough as the wolverine.

Current negative interest rate policies lower other electronic interest rates while keeping the paper currency interest rate constant at zero. This incomplete policy of lowering some short-term interest rates under the central banks control while leaving another–the paper currency interest rate–fixed, causes predictable problems. In particular, not lowering the paper currency interest rate is hard on banks, since banks then have to worry that customers will pull money out of the bank as cash if the bank imposes a negative deposit rate. Storing large amounts of cash may be difficult and costly, but households can easily store modest amounts of cash at home instead of leaving that money in the bank. This strain on banks can be avoided by lowering the paper currency interest rate as well. For the mechanics of how to lower the paper currency interest rate, see “How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide.”

That said, the current worries about the effect of negative interest rates on bank profits seem to be overblown. As an example of those worried, consider this from Jon Hilsenrath’s February 11, 2016 Wall Street Journal article “Yellen Says Fed Should Be Prepared to Use Negative Rates if Needed”:

Ms. Yellen was greeted with widespread skepticism, particularly among Republicans. Negative rates would “crush net interest margins for banks,” said Sen. Pat Toomey (R-Pa.) “It would put the us deep in the midst of a global currency war.”

“The Fed really has no real ammunition left,” said Sen. Bob Corker, (R-Tenn.)

Let me deal with each point in turn.

Will Negative Rates Crush Bank Profits? The first is Pat Toomey’s claim that negative rates will “crush net interest margins for banks.” In addition to what I said above about cutting the paper currency interest rate in tandem with other rates to help preserve bank margins, let me say:

Will Negative Rates Put Us Deep in the Midst of a Global Currency War? Interest rate cuts do indeed have an effect on exchanges rates, but that doesn’t make it a “global currency war.” The essence of a “war” is that it is zero-sum or negative sum: what I get, you lose, with some extra destruction along the way. That is not the way interest rate cuts work. If all countries cut their interest rates, that is a global monetary expansion and stimulates the whole world economy. If the world economy needs stimulus, that is a good thing–hardly what the phrase “global currency war” seems to suggest. So this is a very misleading phrase–totally inappropriate to the reality of what is happening.

It is possible to have a global currency war. Cutting rates just isn’t it. The way to have a global currency war is for each country to sell its own Treasury bills to get funds to buy other countries’ Treasury bills. This is often called a currency intervention. If all countries do this, it is easy to see that everything cancels out and nothing is accomplished. You sell yours to buy mine, I sell mine to buy yours, and we are back at the starting block.

So selling one’s own Treasury bills to buy the Treasury bills of other countries is a zero sum endeavor and qualifies as an opening shot in a currency war. The way to avoid a global currency war of this type is to insist that central banks actually cut interest rates if they want to stimulate their economies, instead of just buying safe short-term foreign assets.

Have Central Banks Run Out of Ammunition? No. Not if they stand ready to cut the paper currency interest rate as well as other interest rates.

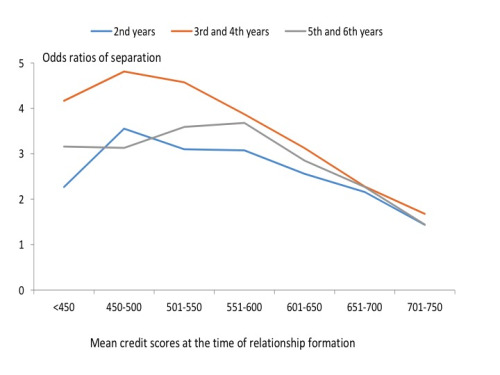

From Figure 3 in “Credit Scores and Committed Relationships.” The Odds ratio shows how many times more likely it is for a relationship to dissolve given a lower average credit score compared to the odds a relationship will dissolve when the couple has an average credit score above 800.

My former student Geng Li, another University of Michigan PhD, Jane Dokko, and Jessica Hayes identified some interesting facts about how well credit scores predict the longevity of a romantic relationship. Here is the abstract to their paper “Credit Scores and Committed Relationships”:

This paper presents novel evidence on the role of credit scores in the dynamics of committed relationships. We document substantial positive assortative matching with respect to credit scores, even when controlling for other socioeconomic and demographic characteristics. As a result, individual-level differences in access to credit are largely preserved at the household level. Moreover, we find that the couples’ average level of and the match quality in credit scores, measured at the time of relationship formation, are highly predictive of subsequent separations. This result arises, in part, because initial credit scores and match quality predict subsequent credit usage and financial distress, which in turn are correlated with relationship dissolution. Credit scores and match quality appear predictive of subsequent separations even beyond these credit channels, suggesting that credit scores reveal an individual’s relationship skill and level of commitment. We present ancillary evidence supporting the interpretation of this skill as trustworthiness.

Jo Craven McGinty had a nice article in the Wall Street Journal reporting on this paper.

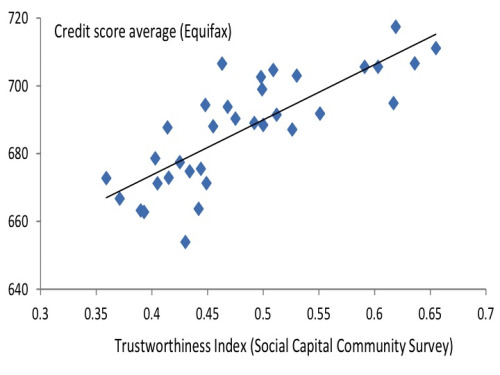

As Jane, Geng and Jessica’s abstract suggests, the most obvious reason high credit scores might predict how long a relationship lasts is that high credit scores tend to go along with experiencing less financial stress that might threaten the relationship. But they argue that high credit scores also tend to go along with higher character. They present the following graph showing how communities in which people say other people can be trusted tend to have higher average credit scores:

Whether or not credit scores can adequately measure character, I am struck by the importance for relationships of telling the truth and following through on tasks one has committed to do. As long as you and your partner tell the truth and follows through on tasks he or she has committed to do, there is some chance that you and your can identify and work through disagreements before truly bad things happen or truly important things get left undone. On the other hand, those who don’t tell the truth and don’t follow through on things they said they would do turn all of the squawks coming out of their mouths into cheap talk. Then it is as if the relationship is on a patch of frictionless, infinitely slippery ice: the relationship can’t go anywhere because there is no traction.

The same issue arises at the level of society. If a society ever gets to the stage in which such a large fraction of people lie when it is convenient that it is almost impossible to determine what is true even when it really matters, that society is in deep trouble.

I particularly worry about the danger of creeping politicization of social science, with social scientists suppressing results they think will be used to further the agenda of the political party they don’t like, and going to easy on claimed results they think support the agenda of the party they hold to. This is a form of deception, and can get a democracy in trouble just as lying within a relationship can get a relationship in trouble.

Don’t miss this fascinating graphic at the link above to a post on howmuch.net via the World Economic Forum.

My first economic journal article on negative interest rate policy is entitled “Negative Interest Rate Policy as Conventional Monetary Policy.” So it is delightful to see Narayana Kocherlakota arguing that negative interest rate policy should be treated as conventional monetary policy in his post “The Potential Power of Negative Nominal Interest Rates.” Here is the heart of Narayana’s argument:

Here’s the wrong way to communicate: keep saying that negative is a purely emergency setting that will be abandoned shortly. The impact of policy depends on the expected path of interest rates over the medium and longer term. The central bank’s communication means that its expanded policy space will have little influence on those medium and longer term expectations. Note that even if the central bank actually keeps rates negative for many years, this ongoing communication will systematically rob the policy of its effectiveness (as well as hurting central bank credibility).

Here’s the right way to communicate: keep saying that all available tools, including negative interest rates, will be used as is needed to return employment and inflation to desirable levels as rapidly as possible. This communication means that the public and markets know that the new policy space can be used to buffer the economy against any adverse shock.

I agree with everything above. But part of the reason Narayana argues this way is that he thinks there is some limit below which interest rates cannot go, because of paper currency. But the paper currency problem is well on its way to being solved. (See How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide.”) For any central bank that knows what it is doing, there is no lower bound to interest rates other than the risk of overheating the economy by too much monetary stimulus.And increasingly, central banks do know how to break through any lower bound created by paper currency. In particular, I have personally explained how to deal with the paper currency problem in the following presentations (a list copied over from “Electronic Money: The Powerpoint File” as of today):

That won’t be the end of my itinerary.

Link to Narayana Kocherlakota’s Wikipedia page

On March 25, 2015, Narayana Kocherlakota sat in my office at the University of Michigan; we talked especially about negative interest rate policy. (See my preface to “Yichuan Wang on Narayana Kocherlakota and coauthors’ “Market-Based Probabilities: A Tool for Policymakers.”) He has since emerged as a major presence on Twitter; you can get a sense of this from my storified Twitter discussion with him: “Narayana Kocherlakota and Miles Kimball Debate the Size of the US Output Gap in January, 2016.” But don’t miss the chance to go to Narayana’s Twitter homepage as well.

Yesterday, February 9, 2016, Narayana posted: “Negative Rates: A Gigantic Fiscal Policy Failure,” arguing quite explicitly for negative interest rates. Narayana writes about moving to negative interest rates. In his words:

So, going negative is daring but appropriate monetary policy.

Narayana then goes on to criticize low levels of government investment given very low interest rates. This is an issue I have written about more than once, in a way generally sympathetic to Narayana’s point:

I don’t come down in exactly the same place as Narayana, though. As I noted to John Conlin, who pointed me to Narayana’s post, I tend to think that monetary policy should be used to stabilize the economy, not fiscal policy. Once monetary policy does its job, if the medium-run natural rate of interest is still low, then we should undertake more government investment. (See “The Medium-Run Natural Interest Rate and the Short-Run Natural Interest Rate.”) And we should undertake crucial government investments even if interest rates are high after the economy recovers. But it is just too hard to time government investment effectively in order to stabilize the economy.

Monetary policy has a lag of 6 to 12 months in its effects. Even so, it is much nimbler than government investment. Private investment and imports and exports can’t turn on a dime; hence the 6 to 12 month delay in the effect of monetary policy. But government investment typical takes even longer than that to turn around.

Using monetary policy as it should be used, aggregate demand is no longer scarce. Monetary policy can provide all the firepower needed. But fiscal policy can still play a role. Fiscal policy is most helpful in economic stabilization under two circumstances:

1. When (as is not the case for government investment) it can move faster and act faster in its effects than monetary policy, or

2. When monetary policy is somehow constrained.

Other than automatic stabilizers, which are extremely helpful, but not enough by themselves, the one type of fiscal policy that acts fast is fiscal policy that affects household consumption which can realistically change within a matter of days. Some might think of tax rebates in this regard, but I have argued at some length that tax rebates are a strictly dominated policy in “Getting the Biggest Bang for the Buck in Fiscal Policy.” In brief, I argue that the ratio of stimulus to ultimate addition to the national debt is much more favorable for lines of credit from the government than tax rebates. For example, it is not unreasonable to think that, since much of it would be repaid, a $2000 line of credit from the government would ultimately cost the government about as much as a $200 tax rebate. But a $2000 line of credit is likely to provide a much stronger impetus to consumption than a $200 tax rebate.

As for constraints on monetary policy, the zero lower bound is crumbling all around us. After that the most important constraint on monetary policy is the fact that so many European countries share their monetary policy in the euro zone. For these countries, fiscal policy–or if you want to call it that, credit policy of the sort I talk about in “Getting the Biggest Bang for the Buck in Fiscal Policy”–can be very helpful in adjusting the overall level of macroeconomic stimulus to different needs from one country to another in the euro zone. There may also be a place for government investment as a countercyclical tool in the euro zone. But given vigorous monetary policy, it might well be that government investment, even in the euro zone, might best be directed at medium to long-run considerations rather than short-run considerations. My posts bulleted above address some aspects of those medium- to long-run considerations.

Note: Also, don’t miss my contribution to long-run fiscal policy as laid out in “How and Why to Expand the Nonprofit Sector as a Partial Alternative to Government: A Reader’s Guide.”

This is of great interest to me as someone who does research in the economics of happiness. It would be great to have an extra way of measuring people’s happiness that do not depend on interrupting them to ask them to make a self report.

Note: If you hit the paywall, google the title to go around it.

The Bank of Japan surprised the world by going to negative interest rates on January 29, 2016. You can read more about that move in Reporting on Japan’s Move to Negative Interest Rates and in these 3 news articles (1, 2, 3). But there are important aspects of the Bank of Japan’s new policy that are only now being appreciated.

I have written a great deal about negative interest rate policy. (I have organized relevant links here.) But, thanks to Noah Smith pointing me to Martin Sandbu’s February 4, 2016 article in the Economics “Free Lunch: There is no lower bound on interest rates,” I realize that the Swiss National Bank–with the Bank of Japan following in its footsteps–has hit upon an additional tool for blocking massive paper currency storage that I hadn’t thought of. Here is how Martin Sandbu describes it:

But the Bank of Japan’s set-up for negative rates, which apparently follows the Swiss National Bank’s, casts doubt on the premise that the nominal cost of holding cash is zero. As we have explained, if a private Japanese bank wishes to exchange its central bank reserves for cash, the BoJ will adjust the portion of its reserves to which negative rates apply by the same amount. That means any extra cash that a bank wishes to hold will cost it as much as if it kept it on deposit at the central bank.

And here is the description from the Bank of Japan’s official statement about its new negative interest rate policy:

2. Adjustment concerning a significant increase in financial institutions’ cash holdings

In order to prevent a decrease in the effects of a negative interest rate due to financial institutions’ cash holdings, if their cash holdings increase significantly from those during the benchmark reserve maintenance periods, the increased amount will be deducted from the macro add-on balance in (2). In cases where the increased amount is larger than the macro add-on balance, the amount in excess of the macro add-on balance will be further deducted from the basic balance in (1).

What is fascinating is this: a central bank can effectively impose a negative interest rate on additions to cash holdings by saying that any bank with access to the cash window is on the hook for whatever paper currency interest rate the central bank decides to charge on cumulative net withdrawals of paper currency by that bank after a certain date regardless of who actually ends up with that paper currency. Then it is up to the bank to figure out how and whether to pass on to its customers the negative paper currency interest rate it faces on that extra paper currency. Martin Sandbu’s article has a nice discussion of how pass-through might work.

One chink in the armor of this mechanism for imposing negative interest rates on cumulative net withdrawals of paper currency would be if a bank went bankrupt after withdrawing a huge amount of cash at the cash window and handing off that cash to favored individuals. But that doesn’t seem like a big issue. Surely the number of banks that have access to the cash window willing to intentionally go bankrupt to help favored individuals get paper currency not subject to the negative interest rate is limited, and there may be some way for the government to prosecute the individuals who organized this scheme of using bankruptcy to circumvent the negative interest rate on additional paper currency.

One thing that the Bank of Japan may not yet have realized is that banks can be charged for net cash withdrawals even beyond an amount equal to the bank’s initial reserves. As it is now, the policy is represented as a policy about how much of reserves is exempted from the negative interest rates, or even receives a +.1% interest rate, but that need not be the case. Banks can be charged interest on cumulative net cash withdrawals quite apart from how their reserve accounts are handled. For now, the Bank of Japan has made a good choice to charge the negative paper currency interest rate through the formula for interest on reserves, but it should not stop there if very large amounts of paper currency are withdrawn.

Speaking of the possibility of cash withdrawals exceed initial reserves, another additional tool that I will mention only briefly is that if negative interest rates are adequate to get velocity up on a given monetary base, limits on the monetary base may limit the total amount of paper currency that can be withdrawn. This is a point I take from Martin Sandbu, who wrote in “Free Lunch: There is no lower bound on interest rates”: