Instrumental Tools for Debt and Growth

A Joint Post by Miles Kimball and Yichuan Wang

Yichuan (see photo above) and I talked through the analysis and ideas for this post together, but the words and the particulars of the graphs are all his. I find what he has done here very impressive. On his blog, where this post first appeared on June 4, 2013, the last two graphs are dynamic and show more information when you hover over what you are interested in. This post is a good complement to our analysis in our second joint Quartz column: “Autopsy: Economists looked even closer at Reinhart and Rogoff’s data–and the results might surprise you,” which pushes a little further along the lines we laid out in “For Sussing Out Whether Debt Affects Future Growth, the Key is Carefully Taking Into Account Past Growth.”

In a recent Quartz column, we found that high levels of debt do not appear to affect future rates of growth. In the Reinhart and Rogoff (henceforth RR) data set on debt and growth for a group of 20 advanced economies in the post WW-II period, high levels of debt to GDP did not predict lower levels of growth 5 to 10 years in the future. Notably, after controlling for various intervals of past growth, we found that there was a mild positive correlation between debt to GDP and future GDP growth.

In a companion post, we address some of the time window issues with some plots how adjusting for past growth can reverse any observed negative correlation between debt and future growth. In this post, we want to address the possibility that future growth can lead to high debt, and explain our use of instrumental variables to control for this possibility.

One major possibility for this relationship is that policy makers are forward looking, and base their decisions on whether to have high or low debt based on their expectations of future events. For example, if policy makers know that a recession is coming, they may increase deficit spending to mitigate the upcoming negative shock to growth. Even though debt may have increased growth, this would have been observed as lower growth following high debt.On the other hand, perhaps expectations of high future growth make policy makers believe that the government can afford to increase debt right now. Even if debt had a negative effect on growth, the data would show a rapid rise in GDP growth following the increase in debt.

Apart from government tax and spending decisions informed by forecasts of future growth, there are other mechanical relationships between debt and growth that are not what one should be looking for when asking whether debt has a negative effect on growth. For example a war can increase debt, but the ramp of the war makes growth high then and predictably lower after the ramp up is done and predictably lower still when the war winds down. So there is an increase in debt coupled with predictions for GDP growth different from non-war situations. None of this has to do with debt itself causing a different growth rate, so we would like to abstract from it.

To do so, we need to extract the part of the debt to GDP statistic that is based on whether the country runs a long term high debt policy, and to ignore the high debt that arises because of changes in expected future outcomes or because of relatively mechanical short-run aggregate demand effects of government purchases as a component of GDP. Econometrically, this approach is called instrumental variables, and would involve using a set of variables, called instruments, that are uncorrelated with future outcomes to predict current debt.

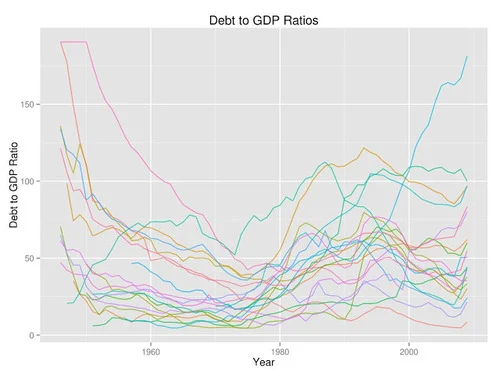

Since we are considering future outcomes, a natural choice for instrument would be the lagged value of the debt to GDP ratio. As can be seen below, debt to GDP does not jump around very much. If debt is high today, it likely will also be high tomorrow. Thus lagged debt can predict future debt. Also, since economic growth is notoriously difficult to forecast, the lagged debt variable should no longer reflect expectations about future economic growth.

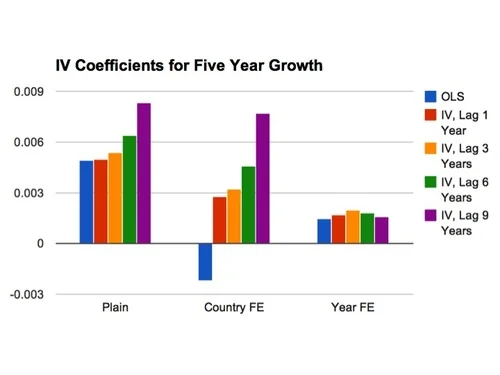

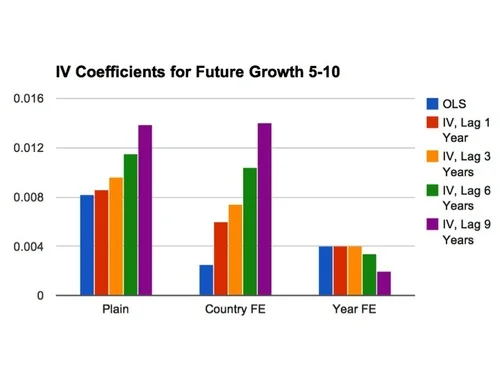

By using lagged debt and growth as instruments, we isolate the part of current debt that reflects debt from a long term high debt policy, and not by short run forecasts or other mechanical pressures. We plot the resulting slopes on debt to GDP in the charts below, for both future growth in years 0-5 and for future years 5-10. For the raw data and computations, consult the public dropbox folder.

From these graphs, we can make some observations.

First, almost all the coefficients, across all the different lags and fixed effects, are positive. Since these results are small, we should not put too much weight on statistical significance. However, it should be noted that the plain results, OLS and IV, for both growth periods are all statistically significant at at least the 95% confidence level, and the IV estimates for the 5-10 year period in particular are significant at the 99% confidence level.

The one negative estimate, OLS estimate with country fixed effects, has a standard error with absolute size twice as large as the actual slope estimate.Moreover, country fixed effects are difficult to interpret because they pivot the analysis from looking at high debt versus low debt countries towards analyzing a country’s indebtedness relative to its long run average.

These results are striking considering therobustness with which Reinhart and Rogoff present the argument thatdebt causes low growth in their 2012 JEP article. Yet instead of finding a weaker negative correlation, after controlling for past growth, we find that the estimated relationship between current debt and future growth is weakly positive instead.

Second, when taking out year fixed effects, there is almost no effect of debt and future . Econometrically, year fixed effects takes out the average debt level in every year, which leaves us analyzing whether being more heavily indebted relative to a country’s peers in that year has an additional effect on growth. Because this component is consistently smaller than the regular IV coefficient, this suggests,for the advanced countries in the sample, it’s absolute, not relative, debt that matters.

This should be no surprise. As most recently articulated in RR’s open letter to Paul Krugman, much of the argument against high debt levels relies on a fear that a heavily indebted country becomes “suddenly unable to borrow from international capital markets because its public and/or private debts that are a contingent public liability are deemed unsustainable.” The credit crunch stifles growth and governments are forced to engage in self-destructive cutbacks just in order to pay the bills. At its core, this is a story about whether the government can pay back the liabilities. But whether or not liabilities are sustainable should depend on the absolute size of the liabilities, not just whether the liabilities are large relative to their peers.

Now,our conclusion is not without limitations. As Paul Andrew notes, the RR data set used focuses on “20 or so of the most healthy economies the world has ever seen,” thus potentially adding a high level of selection bias.

Additionally, we have restricted ourselves to the RR data set of advanced countries in the post WW-II period. The 2012 Reinhart and Rogoff paper considered episodes of debt overhangs from the 1800’s, and thus the results are likely very different. However, it is likely that prewar government policies, such the gold standard and the lack of independent monetary authorities, contributed to the pain of debt crises. Thus our timescale does not detract from the implication that debt has a limited effect on future growth in modern advanced economies.

In their New York Times response to Herndon et. al., Reinhart and Rogoff “reiterate that the frontier question for research is the issue of causality”. And at this frontier, our Quartz column, Dube’s work on varying regression time frames, and these companion posts all suggest that causality from debt to growth is much smaller than previously thought.