Quartz #21—>Optimal Monetary Policy: Could the Next Big Idea Come from the Blogosphere?

Here is the full text of my 21st Quartz column, “This economic theory was born in the blogosphere and could save markets from collapse,” now brought home to supplysideliberal.com and given my preferred title. (I am now up-to-date bringing home to supplysideliberal.com all of my columns that are past the 30-day exclusive I give Quartz by contract.)

Even before I started blogging, Noah Smith told me I should write a post about NGDP targeting. This is that post. And it is also the post on “Optimal Monetary Policy” that I have been promising for some time. It was first published on February 22, 2013. Links to all my other columns can be found here.

If you want to mirror the content of this post on another site, that is possible for a limited time if you read the legal notice at this link and include both a link to the original Quartz column and the following copyright notice:

© February 22, 2013: Miles Kimball, as first published on Quartz. Used by permission according to a temporary nonexclusive license expiring June 30, 2014. All rights reserved.

The most important equation in economics

Much of the history of economics can be traced by the contents of its best-selling textbooks. In 1848, John Stuart Mill published the blockbuster economics textbook of the 19th century: Principles of Political Economy. A century later, in 1948, Paul Samuelson—the very first American Nobel laureate in economics, who more than anyone else made economics the mathematical subject it is today—popularized Keynesian economics in the best-selling economics textbook of all time, Economics: An Introductory Analysis. This past year, in my classroom, I taught from one of the two best and most popular introductory economics textbooks, Brief Principles of Macroeconomics authored by Greg Mankiw—chair of the economics department at Harvard, former chair of the president’s Council of Economic Advisors, and my graduate school advisor.

One constant in all of these textbooks is an equation as famous for economics as E=MC2 is for physics—an equation suitable for an economist’s vanity license plate: MV=PY.

As E=MC2 is the key to understanding nuclear weapons and nuclear power, the “equation of exchange” MV=PY is the key to understanding monetary policy. And for the first major school of economic thought born in the blogosphere, I know of no way to explain their views without invoking this equation. Nerdily charismatic, they call themselves “market monetarists,” but it is easier to identify them by their attribution of almost mystical powers to maintaining a steady growth rate of both sides of this equation. Let me try to explain why the equation MV=PY is so important.

One way to read MV=PY is: Velocity adjusted money equals nominal GDP.

M is the money supply.

V is the “velocity” of money or how hard money works.

So M times V is velocity-adjusted money.

P is the price level: think of the consumer price index, though P would include the prices of other things as well, such as equipment bought by businesses.

Y is real GDP, the amount of goods and services produced by the economy that really matter for our material well-being.

But P times Y is GDP at current prices before adjusting for inflation. GDP before adjusting for inflation is called nominal GDP. PY, that is nominal GDP, can go up either because real GDP goes up (an increase in Y) or because prices go up (an increase in P).

So what the equation of exchange says is: if there is a lot of money in the economy and that money is working hard, then either the economy will have high real GDP (=Y) or high prices (P). On the other hand, if there is not enough money or money is not working very hard, then either real GDP will be low or prices will be low.

Milton Friedman, one of the dominant economists of the 20th century, didn’t write a best-selling economics textbook, but had an enormous influence on policy as a public intellectual. (To celebrate what would have been his 100th birthday last year, I annotated links to many of his best YouTube videos here on my blog. They are still well worth watching.) Friedman played a key role in the US’s switch from a draft to a volunteer military and was the intellectual mastermind behind the school choice movement. As an adviser to president Ronald Reagan, he was the gray eminence of Reaganomics. In monetary policy, Friedman proposed having the money supply (M) grow at a constant rate. Since he thought velocity (V) wouldn’t change much, Friedman was, in effect, advocating a constant growth rate of the velocity-adjusted money supply—and therefore a constant growth rate of nominal GDP. The trouble with this idea is that velocity turned out in later years not to be constant—both because it is affected by interest rates and because it is affected by innovations such as ATM’s. So keeping the money supply (M) growing at a constant rate would cause erratic swings in the velocity-adjusted money supply (MV), and therefore in nominal GDP.

Enter: the market monetarists

So the spirit of Milton Friedman’s proposal is the idea of keeping velocity-adjusted money, and therefore nominal GDP, growing at a constant rate. In a movement that should make Milton Friedman proud (if he can get internet access in heaven), that is exactly what the “market monetarists” advocate. The importance market monetarists put on the idea of keeping nominal GDP growing at a constant rate is readily apparent from the frequency of the abbreviation NGDP for nominal GDP in some of the posts and tweets by Scott Sumner, David Beckworth, and Lars Christensen. One of the best ways to see the value of paying attention to nominal GDP is to look at a graph of nominal GDP over time in the US, using data from the Federal Reserve Bank of St. Louis.

In all the years since 1955, the most striking feature of the graph is the jog down in nominal GDP since the financial crisis in late 2008. Market monetarists take this jog down in GDP since the financial crisis as an indication that monetary policy has not been anywhere near stimulative enough in the aftermath of the financial crisis. In this, they are absolutely right. The reason the graph of nominal GDP shows the stance of monetary policy so well is that too-tight monetary policy drags down both prices (=P) and real GDP (=Y), which both contribute to nominal GDP (=PY) that is low relative to its trend. Conversely, too-loose monetary policy pushes up both prices and real GDP, which both contribute to nominal GDP that is high relative to its trend.

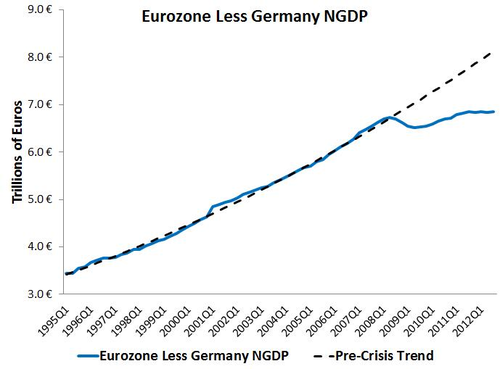

Here is a corresponding graph for the euro zone minus Germany from wunderkind and Wonkbook blogger Evan Soltas:

This graph for Europe focuses on recent years (the trend is shown by the dashed line) and indicates that, while it might have been more nearly okay for Germany, the European Central Bank’s monetary policy has been too tight for the rest of the euro zone.

The graphs show one of the big attractions of market monetarism: with graphs like these it is easy to get a handle on whether monetary policy has been too loose or too tight. Market monetarists go further to say that if the US Federal Reserve and other central banks committed to do whatever it takes to keep nominal GDP on track, then the financial markets listening to that commitment would react in a way that would help to make it happen. In Fed-speak, the market monetarists emphasize communication policy in the form of forward guidance on the track of nominal GDP the Fed or other central bank is aiming for. To know whether the financial markets are getting the message, market monetarists advocate the creation of assets that would provide a market prediction for nominal GDP much as TIPS (Treasury Inflation Protected Securities) provide a market prediction for inflation.

So far, I have emphasized the positive aspects of market monetarism, because I think market monetarism has, in fact, been an important force for good in our current economic troubles. When a crisis scares people into holding back on spending, the best remedy is monetary stimulus, and graphs of nominal GDP, interpreted as a market monetarist would, speak loudly for exactly the needed monetary stimulus.

Evaluating market monetarism

But now I want to step back and question whether market monetarism is the final answer for monetary policy. There are three things that matter for monetary policy: the temptation, the objective if a central bank can resist the temptation, and the toolkit.

The Temptation. The temptation for monetary policy is that, absent a concern about inflation, GDP is chronically too low for at least three reasons: imperfect competition, taxes, and labor market frictions. The trouble is that raising GDP beyond a certain point—a point called the natural level of GDP—does raise inflation. And not only does raising GDP beyond a certain point raise inflation, pushing GDP above the natural level for even a year or two raises the level of inflation permanently. The one way to get rid of that extra inflation is to push GDP below the natural rate for a while. To put things starkly, after the above-natural GDP of the 1960s, we would still have the double-digit inflation of the 1970s if Americans hadn’t suffered through a big recession that put GDP below its natural level during Reagan’s first term in the early 1980’s. We have low inflation today in large measure thanks to the suffering of Americans in the early 1980s.

The objective. “Sinning” by having GDP above the natural level is no fun if it has to be coupled with “repenting” by having GDP below the natural level to avoid having inflation forever higher. There are two reasons the combination of above-natural GDP one year and below-natural GDP another year is a bad deal. First, the pleasure from higher output and employment to workers, to the taxman, and to firms, is not as big as the pain from lower employment. Second, higher output makes inflation go up more readily than lower output brings inflation back down. Put all this together, and the objective is clear: stay at the natural level of output to avoid the bad deals from any other combination of output in different years that keeps inflation from being higher in the end.

Now, let’s translate the objective of staying at the natural level of output into nominal GDP terms. (It is important in the discussion above that I am thinking of inflation primarily in terms of otherwise slow-to-adjust prices going up faster, rather than in terms of slow-to-adjust wages going up faster. My argument for doing that can be found here.) As long as the natural level of output is growing at a steady rate, keeping real GDP on that steady track will also keep inflation and so the rate of increase of prices steady. If both real GDP and prices are growing at a steady rate, then nominal GDP will be growing at a steady rate. So a steady growth rate of nominal GDP is exactly the right target as long as the natural level of output is growing steadily.

But what if new technology makes the natural level of output go up faster, as the digital revolution did from at least 1995 to 2003? Then real GDP should be going up faster to keep inflation steady. And that means that nominal GDP should also be going up faster. Historically, the Fed has not handled its response to unexpected technology improvements very well, as I discuss in another column, but that doesn’t change the fact that the Fed should have had nominal GDP go up faster after unexpectedly large improvements in technology. (Because the Fed actually let nominal GDP go below trend after technology improvements—instead of above trend as it should have—many people ended up not being able to get jobs after technology improvements.)

By the same token, if technology improves more slowly than it normally does, then both real and nominal GDP should be on a lower track to keep inflation steady and avoid the bad deals from pushing inflation up and then having to bring it back down. Some people have claimed that our current economic slump is a reflection of technology growing more slowly, but careful measures of the behavior of technology and a growing body of research by economists show that is at most a small part of what has been going on since the financial crisis that hit in late 2008. Indeed, if all of the below-trend output we have seen in the last few years were due to more slowly improving technology, we would not have seen inflation fall the way it did after the financial crisis.

The toolkit. Even if I can bring my market monetarist friends around to adjusting the nominal GDP target for what is happening with technological progress, I differ from them in thinking that the tools currently at the Fed’s disposal plus clearly communicating a nominal GDP target are not enough to get the desired result. The argument goes as follows. Interest rates are the price of getting stuff—goods and services—now instead of later. If people are out of work, we want customers to buy stuff now by having low interest rates. Thinking about short-term interest rates like the usual federal funds rate target that the Fed uses, the timing of the low interest rates matters. If everyone knows we are going to have low short-term interest rates in 2016, then it encourages buying in the whole period between now and 2016 in preference to buying after 2016. But to get the economy out of the dumps, we really want people to buy right now, not spread out their purchases over 2013, 2014, and 2015. The lower we can push short-term interest rates, the more we can focus the extra spending on 2013, so that we can have full recovery by 2014, without overshooting and having too much spending in 2015. This is an issue that economist and New York Times columnist Paul Krugman alludes to recently in a column about Japanese monetary policy.

There is only one problem with pushing the short-term interest rate down far enough to focus extra spending right now when we need it most: the way we handle paper currency. The Fed doesn’t dare try to lower the interest rate it targets below zero for fear of causing people to store massive amounts of currency (which effectively earns a zero interest rate). Indeed, most economists, like the Fed, are so convinced that massive currency storage would block the interest rate from going more than a hair below zero that they talk regularly about a zero lower bound on interest rates. The solution is to treat paper currency as a different creature than electronic money in bank accounts, as I discuss in many other columns. (“What Paul Krugman got wrong about Italy’s economy” gives links to other columns on electronic money as well.) If instead of being on a par with electronic money in bank accounts, paper currency is allowed to depreciate in value when necessary, the Fed can lower the short-term interest as far as needed, even if that means it has to push the short-term interest rate below zero.

Keeping the economy on target

In the current economic doldrums, breaking through the zero lower bound with electronic money is the first step in ensuring that monetary policy can quickly get output back to its natural level. A better paper currency policy puts the ability to lower the Fed’s target interest rate back in the toolkit. That makes it possible for the Fed to get the timing of extra spending by firms and households right to meet a nominal GDP target—hopefully one that has been appropriately adjusted for the rate of technological progress.

Despite the differences I have with the market monetarists, I am impressed with what they have gotten right in clarifying the confusing and disheartening economic situation we have faced ever since the financial crisis triggered by the collapse of Lehman Brothers on September 15, 2008. If market monetarists had been at the helm of central banks around the world at that time, we might have avoided the worst of the worldwide Great Recession. If the Fed and other central banks learn from them, but take what the market monetarists say with a grain of salt, the Fed can not only pull us out of the lingering after-effects of the Great Recession more quickly, but also better avoid or better tame future recessions as well.