Is It a Problem for Negative Interest Rate Policy If People Hang On to Their Paper Currency?

I teach how to break through the zero lower bound in my “Monetary and Financial Theory” class. I got an interesting question from one of my students, Matthew Hoffman (who chose fame over anonymity when I told him I wanted to write this Q&A post. Here are his questions and my answers.

Matthew: I understand that electronic money would be the unit of account, and that the deposit fee, in a time of negative interest rates, would eliminate the ZLB as the paper currency is charged roughly the value of the negative rate upon deposit. So my question is what stops people from just taking all of their money out and holding it as cash? You give three ways to act against paper currency storage, but since you advocate the third method (the fee on deposits) why can’t people still withdraw all of their money in cash and then not re-deposit until the deposit fee is “allowed to shrink when the interest rate is positive?”

Is the answer to my question explained in part “B. The Paper Currency Interest Rate,” in that since the electronic money is the unit of account, then the deposit fee still affects the value of paper currency regardless of whether it’s in the bank or under the mattress? For example, if I take a $100 bill out of the bank when the deposit fee is 2%, then is the value of my bill only $98 if I go to the mall? Or is it still worth $100, but when I go to re-deposit it, at that point it will be worth only $98 and I essentially lost $2 by putting it in the bank?

Miles: Excellent questions!

- Note that over the horizon where paper currency earns a zero interest rate, money in the bank also does. So that creates no incentive to take out paper currency–though it also provides no disincentive.

- At retail, paper currency will be at par for a while. If I take out cash and spend it, that stimulates the economy. So that is OK. It doesn’t stop the policy from working.

- The interest rate for small checking and saving accounts may stay zero if interest rates are not too low, and to somewhat lower interest rates if the central bank subsidizes zero interest rates in small checking and saving accounts. If so, then those folks wouldn’t have any temptation to withdraw paper currency in any case.

Notice that in no case is there an arbitrage that stops interest rates from being deeply negative.

Matthew: One follow up question…so would cash that was already under the mattress when the Fed increases the deposit fee still be worth its face value? It would only be worth less if it were deposited? This is like your second point in your previous email I believe…the value will stay at par for awhile and that cash can stimulate the economy if spent.

Miles: If used for purchases reasonably promptly, paper currency households already had could probably be spent at par. And most business try to deposit their paper currency in the bank quickly, while the exchange rate changes very slowly. So paper currency on hand at the beginning of the electronic money system should not be a big deal for them.

Brian Blackstone: Deflation Holds No Terrors for Those Who Know How to Use Negative Interest Rates

I have criticized Wall Street Journal reporter Brian Blackstone in the past for not appreciating the power of negative interest rate policy:

- The Wall Street Journal’s Big Page One Monetary Policy Mistake

- Brian Blackstone Doubles Down on a Big Mistake in Reporting on Monetary Policy

But Brian Blackstone is beginning to show a greater appreciation for negative interest rates in his October 18, 2015 Wall Street Journal article

- “Switzerland Offers Counterpoint on Deflation’s Ills: Country shows falling consumer prices can go hand in hand with steady growth, low unemployment.”

Here are some of the key passages:

1. Consumer prices in Switzerland have fallen on an annual basis for most of the past four years. … Even after food and energy prices are stripped out, core prices fell 0.7%.

“It’s hard not to call that deflation,” said Jennifer McKeown of Capital Economics …

And yet evidence of deflation’s pernicious side effects—recession, weak employment, rising debt burdens—is pretty much nonexistent in Switzerland. Its economy is expected to expand this year and next, albeit slowly, in the 1% to 1.5% range. Unemployment was just 3.4% in September. Government debt is low.

2. Some of that success is due to the shattering of another long-held maxim: that central-bank policy rates can’t go negative to offset the effects of falling prices.

3. Major central banks prefer annual inflation of about 2% to provide a cushion against deflation.

4. To keep the franc in check, the central bank may be forced to cut the deposit rate even further, analysts say, particularly if the ECB eases policy more.

Brian asks the following question,

So why aren’t central banks embracing the Swiss example?

The answer he gives is this:

Analysts note that it’s difficult to distinguish between good and bad deflation until it’s too late.

But to me the answer is simpler. Deflation is not a good thing, but deflation holds no terrors if a central bank understands how to use negative interest rates. To me, this is the message of Brian’s article, though he doesn’t say it himself.

Although it hasn’t done so yet, because the Swiss National Bank knows how to make the rate of return on paper currency negative if people ever started storing large amounts of paper Swiss francs, it can dare push interest rates lower than other central banks that do not fully understand how to break through the zero lower bound.

You might be interested in the other things I have said about the Swiss National Bank and negative interest rate policy:

- The Swiss National Bank Means Business with Its Negative Rates

- Swiss Pioneers! The Swiss as the Vanguard for Negative Interest Rates

- Q&A on the Swiss National Bank’s Move to Negative Interest Rates

- Negative Interest Rates and Financial Stability: Alexander Trentin Interviews Miles Kimball

- Alexander Trentin and Sandro Rosa Interview Miles Kimball: Clinging to Paper Money is Like Clinging to Gold

- Alexander Trentin: Negative Interest Rates and the Swan Song of Cash

- 18 Misconceptions about Eliminating the Zero Lower Bound

Quartz #66—>Japan Should Be Trying Out a Next Generation Monetary Policy

Here is the full text of my 66th Quartz column, “Japan Should Be Trying Out a Next Generation Monetary Policy,” now brought home to supplysideliberal.com. It was first published on September 11, 2015. Links to all my other columns can be found here.

This column was written in conjunction with two other closely related posts that you might want check out as well:

- Is the Bank of Japan Succeeding in Its Goal of Raising Inflation?”

- An Underappreciated Power of a Central Bank: Determining the Relative Prices between the Various Forms of Money Under Its Jurisdiction

If you want to mirror the content of this post on another site, that is possible for a limited time if you read the legal notice at this link and include both a link to the original Quartz column and the following copyright notice:

© September 11, 2015: Miles Kimball, as first published on Quartz. Used by permission according to a temporary nonexclusive license expiring June 30, 2020. All rights reserved.

After twenty years of slow economic growth, Japan’s Sept. 26, 2012 election centered on Shinzo Abe’s promise to shake up monetary policy. Once in office, Abe appointed Haruhiko Kuroda to head the Bank of Japan. In short order, the Bank of Japan went from defending its monetary policy during those two lost decades of slow growth and bragging about the number of different types of assets it was buying to a serious program of quantitative easing on steroids, with a commitment to buying bonds and other securities equal in value to over half of GDP every year.

One of the announced objectives for this massive asset purchase program is to bring inflation quickly up to 2% per year. The idea is that the zero interest rate the Bank of Japan has maintained for a long time would be a more powerful stimulative for the economy if businesses and consumers were comparing it to a higher inflation rate. The logic is similar to the logic driving economists such as Olivier Blanchard, Larry Ball, and Paul Krugman to recommend raising inflation target to 4% in other countries in order to supercharge the stimulative effect of zero interest rates.

The key concept is that of a “real interest rate,” or an interest rate stated in terms of a basket of goods instead of the usual interest rate stated in terms of money.

Japan is wasting its time trying to raise inflation

Japan may succeed at bringing annual inflation up to 2%; indeed, it has made some real progress toward that goal. But suppose Japan succeeds in getting inflation up to 2%; would that be enough? The US economy has struggled mightily despite the fact that it went into the Great Recession with a 2% annual rate of core inflation. Japan could try to target an even higher rate of inflation, as Blanchard, Ball and Krugman recommend, or Japan could leave behind quantitative easing and higher inflation targets to make the leap to next-generation monetary policy.

The key to next-generation monetary policy is to cut interest rates directly instead of trying to supercharge a zero interest rate by raising inflation. Of course, cutting interest rates below zero pushes them into negative territory. But Switzerland, Denmark, Sweden and the euro zone have already shown that can be done. There is a widespread myth that cutting interest rates much deeper than -0.75% would inevitably cause people and firms to do an end run around those negative interest rates by taking their money out of the banking system as paper currency. Not so!

It is easy to neuter cash taken out of the bank as a way to defeat negative interest rates simply by removing the guarantee that the Bank of Japan will take that cash back at face value. You can find the details of how such a cash-neutralizing policy works here, here and here. This is an idea I have taken on the road that has withstood close examination and grilling by central bankers and economists all over the world. A common reaction is surprise at how easy the practical details are relative to the many much more difficult things central banks already do.

If the guarantee that the Bank of Japan (or other central bank) will always take cash back at face value is removed, it leaves no way to avoid negative interest rates without stimulating the economy. If people take cash out of the bank, store it, and then spend it, that stimulates the economy. If a firm takes a pile of money facing a negative interest rate out of the bank to build a new factory, that stimulates the economy. And even if, say, Japanese households take money that would otherwise earn a negative interest rate out of the bank to buy foreign stocks and bonds, it stimulates the Japanese economy, when excess yen in the hands of the foreigners who sold those stocks and bonds ultimately make their way back to Japan to buy Japanese products, boosting net exports.

Japan is wasting time by trying to raise inflation because it doesn’t need to raise inflation. Raising inflation is an indirect way to get the same effect that can be achieved directly by cutting interest rates. Switzerland, Denmark, Sweden and the euro zone have gingerly dipped their toes in the water of negative interest rates. Japan should go all in.

The alternatives to negative interest rates all have serious downsides. For example, increasing government spending is a bad idea: Japan already has more debt in comparison to its GDP than any other major economy—more than two years worth of GDP. (And saying that the Bank of Japan can just keep buying all that debt ad infinitum should be a last resort.) Worse, Japan has already been down the path of high government spending and has already exhausted most attractive government investment opportunities.

What about ramping up quantitative easing even more? Quantitative easing works in the right direction, but to get the needed effects requires dosages so large that no one knows what side effects it might have. By contrast, economic theory is reasonably clear about how interest rates affect the economy, even when they are negative.

Addressing Japan’s supply-side

Even if Japan makes the leap to next-generation monetary policy, it will still have serious economic problems. Many economists and politicians argue that monetary stimulus is a distraction from necessary supply-side reforms (often called “structural reforms”).

But it is a lot easier to move workers and capital from low productivity activities to higher productivity activities in a boom, than in a stagnant economy in which people worry about getting the next job or finding the next business opportunity.

Having an economy made worse by monetary policy is not a very reliable aid to jumping over political hurdles to supply-side reform. Instead, a substandard economy due to substandard monetary policy is often a temptation to more government spending and more debt. Japan should fix its monetary policy first, by eliminating any floor on interest rates. Then it can and should face its supply-side problems squarely.

John Stuart Mill: Certification, Not Licensing

Miles’s Certificate for the highest level of training for the Bowen Technique

As I do, John Stuart Mill felt a close connection between education policy and certification and licensing policy. I am leery of the overgrowth of licensing requirements for relatively safe occupations, but if we are unable to eliminate them, at least we should make the requirements simple enough that it possible for students to graduate from high school with several licenses–something I proposed in “Magic Ingredient 1: More K-12 School.”

If we can improve evaluation methods, it is much better to certify skills than it is to certify that someone has taken a certain number of classes with passing grades, as I argue in “The Coming Transformation of Education: Degrees Won’t Matter Anymore, Skills Will.”

As for licensing itself, although they are often spoken of in the same breath, there is a world of difference between certification and licensing. Certification requirements say that you have to inform customers of your level of qualifications or lack of qualifications in unmistakable ways, according to a well-defined terminology established by the government. They are based on the principle of telling the truth and not deceiving, but do entail some details to make sure no one misunderstands.

By contrast, licensing requirements say you can be thrown in jail for getting paid for something that someone with an absolutely crystal clear idea of your lack of qualifications is perfectly happy to pay you to do. For example, I would run afoul of the law in Michigan if I cut someone else’s hair for pay–a law ultimately backed up by the threat of throwing me in jail, even if the initial penalty is only a fine. The real reason for that stipulation is that barbers want that barrier to entry in place (I think at least a year and a half of training), not any danger that I will seriously harm someone with a basic haircut. I express some of how wrong I think the overgrowth of licensing requirements is in my post “When the Government Says “You May Not Have a Job.”

Up at the top you see my certificate for the highest level of training in a form of bodywork called the Bowen Technique, which I wrote about in my post “Tom Bowen’s Gift to Humanity: A Powerful Australian Technology.” It is not as if I have time in any case, but a few years ago, I could have hung up a shingle as a bodyworker (the category of someone who has not jumped through any state-defined hoops) and treated people without violating the law. Michigan seems to be going in the direction of many states and requiring a license for any body work, which in some places would require a large amount of training in other modes of body work such as massage therapy (about a year’s worth of additional training).

John Stuart Mill, in paragraph 14 of “On Liberty “Chapter V: Applications” (which I preface with the last sentence of paragraph 13 for context) explains how to get the benefits of certification without having the government force conformity in education or saying one cannot do a job without jumping through hoops that often have little to do with what one’s skill would be at doing a job. Here are the ground rules John suggests:

But in general, if the country contains a sufficient number of persons qualified to provide education under government auspices, the same persons would be able and willing to give an equally good education on the voluntary principle, under the assurance of remuneration afforded by a law rendering education compulsory, combined with State aid to those unable to defray the expense.

The instrument for enforcing the law could be no other than public examinations, extending to all children, and beginning at an early age. An age might be fixed at which every child must be examined, to ascertain if he (or she) is able to read. If a child proves unable, the father, unless he has some sufficient ground of excuse, might be subjected to a moderate fine, to be worked out, if necessary, by his labour, and the child might be put to school at his expense. Once in every year the examination should be renewed, with a gradually extending range of subjects, so as to make the universal acquisition, and what is more, retention, of a certain minimum of general knowledge, virtually compulsory. Beyond that minimum, there should be voluntary examinations on all subjects, at which all who come up to a certain standard of proficiency might claim a certificate. To prevent the State from exercising, through these arrangements, an improper influence over opinion, the knowledge required for passing an examination (beyond the merely instrumental parts of knowledge, such as languages and their use) should, even in the higher classes of examinations, be confined to facts and positive science exclusively. The examinations on religion, politics, or other disputed topics, should not turn on the truth or falsehood of opinions, but on the matter of fact that such and such an opinion is held, on such grounds, by such authors, or schools, or churches. Under this system, the rising generation would be no worse off in regard to all disputed truths, than they are at present; they would be brought up either churchmen or dissenters as they now are, the State merely taking care that they should be instructed churchmen, or instructed dissenters. There would be nothing to hinder them from being taught religion, if their parents chose, at the same schools where they were taught other things. All attempts by the State to bias the conclusions of its citizens on disputed subjects, are evil; but it may very properly offer to ascertain and certify that a person possesses the knowledge, requisite to make his conclusions, on any given subject, worth attending to. A student of philosophy would be the better for being able to stand an examination both in Locke and in Kant, whichever of the two he takes up with, or even if with neither: and there is no reasonable objection to examining an atheist in the evidences of Christianity, provided he is not required to profess a belief in them. The examinations, however, in the higher branches of knowledge should, I conceive, be entirely voluntary. It would be giving too dangerous a power to governments, were they allowed to exclude any one from professions, even from the profession of teacher, for alleged deficiency of qualifications: and I think, with Wilhelm von Humboldt, that degrees, or other public certificates of scientific or professional acquirements, should be given to all who present themselves for examination, and stand the test; but that such certificates should confer no advantage over competitors, other than the weight which may be attached to their testimony by public opinion.

The US Treasury has a report out on Occupational Licensing Reform that I hope to talk about in some detail in a later post. But you might want to read it before then. Here is the link.

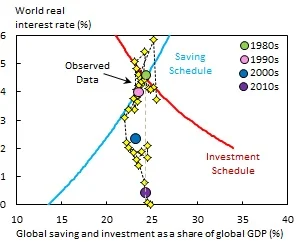

Lukasz Rachel and Thomas Smith: Drivers of Long-Term Global Interest Rates--Can Changes in Desired Savings and Investment Explain the Fall?

On the Bank of England’s new blog, Lukasz Rachel and Thomas Smith have posted an excellent analysis of forces that could plausibly be causing the long-run decline of global interest rates. I highly recommend it. The graph above is a teaser.

Hannah Katz: The Pros and Cons of Tipping Culture

Link to Hannah Katz’s LinkedIn Homepage

I am delighted to host another student guest post by Hannah Katz. This is the 7th student guest post of this semester. You can see all the student guest posts from my “Monetary and Financial Theory” class at this link.

Evidence shows that although the tipping culture is actually an economic advantage for those who can take full advantage of the system, not every waiter is able to do so due to discriminatory factors.

Tipping expectations around the world are vastly different, depending on who you ask. Any U.S. waiter would answer 20% of the total bill, while a Japanese citizen might be confused on what tipping even means. In the United States there exists a federal minimum wage for most careers, but waiting tables is not technically one of them. Although employers are technically supposed to pay the difference if a waiter does not clear minimum wage with his/her tips, in most cases the cost of waiters’ wages is passed on to the consumer in the form of a tip. The tipping culture is actually an economic advantage for those who can take full advantage of the system, but not every waiter is able to do so due to discriminatory factors.

In the Southern Economic Journal article“The Effect of the Tipped Minimum Wage…”, authors William Even and David Macpherson study the effect of a raised tipped minimum wage on full-service restaurant employees. Even and Macpherson studied national data and concluded that if the minimum wage for servers was increased and the expectation for tips was decreased, then full-service employees would suffer reduced employment by restaurants. This indicates that if the cost of servers’ wages were forced onto restaurant owners, effectively raising the minimum wage that most restaurants have to pay their servers, the same result would occur. Clearly, reducing the burden on restaurants by maintaining the practice of tipping is advantageous to waiters.

Another huge advantage of tipping to waiters is that cash tips often go unreported. Anecdotally, I know many waiters that do not fully report their tips to the IRS. Somehow, this is considered normal practice although it is certainly tax fraud. The IRS estimated a $290 billion gap in self and true reported income last year, according to BakerTilly’s article “IRS Targets Tip Income..”, and the gap may be even higher.

Although tipping culture may be beneficial to servers, the practice isn’t exactly fair. As Freakonomics radio host Stephen Dubner points out in “Should Tipping be Banned?”, tips that servers receive correlate to their race, attractiveness, and other discriminatory factors. Basically, the customer of a restaurant has the power to determine the wages of a server and discriminatory practice is unregulated. There is no Human Resources department in restaurants that a waiter can appeal to if he/she feels undercompensated because of discrimination. This data is supported in Tipping Research’s paper Predictorsof Male and Female’s Average Tip Earnings, which found that servers received more tips if they were rated as more attractive, as opposed to years of experience and friendliness, which were uncorrelated with tips.

The tipping culture in the United States and other Western countries is not going away any time soon. Restaurants and waiters both benefit from the system, and customers are so used to it that no widespread action will be taken anytime soon. But perhaps it is time to question this system that causes such a huge gap in true and reported income, and can be discriminatory in nature.

Mehul Gaur: Bernie Sanders’s Financial Transactions Tax is a Bad Idea

Link to Mehul Gaur’s LinkedIn Homepage

I am delighted to host another student guest post by Mehul Gaur. This is the 6th student guest post of this semester. You can see all the student guest posts from my “Monetary and Financial Theory” class at this link.

Bernie Sanders’ proposed 0.5% tax on stock transactions is not only going to dry up liquidity in the markets, but may actually serve to lower tax revenue overall.

Bernie Sanders has been making quite a name for himself recently. After announcing his candidacy for presidency, Bernie has positioned himself to the left of the standard Democratic Party stance and proposed an estimated $15 trillion healthcare reform. One of the ways he has proposed to pay for this massive expenditure is to levy a 0.5% tax on each trade of stocks, bonds, and derivatives. Opponents of the tax argue that it would make it impossible for high-frequency trading firms to operate, put off speculators, and reduce volatility by making very low-margin computerized trades unprofitable.

If Bernie is using this as a piece of political propaganda, its genius. To someone not familiar with the financial markets (the majority of voters), it seems like a tax that provides wide social benefits at a very low cost to “those rich traders” on Wall Street. However, if Bernie is serious about implementing this, he could be doing something that would derail the financial markets and possibly cause another stock market crash.

Let’s start with what supporters of the policy are right about: It will drive high-frequency traders (HFTs) out of business. Their profit margins per trade are well below 0.5% and it will essentially eliminate the industry.

There’s just 1 tiny problem with that: It is estimated that HFTs make up somewhere between 50%-75% of all trading volume in the United States. So, by implementing this tax, one would essentially be directly eliminating at least half of the liquidity in the equity markets. But we got rid of the evil HFTs right? HFTs are widely believed to actually help the markets by both adding liquidity and reducing trading costs. Additionally, by cutting the trading volume in half one would also be reducing the potential revenue from the tax. It may also have a net negative effect on tax revenue because of reductions in capital gains taxes. Bernie did not provide any numbers on this, but as I discuss later, both of these statements have an empirical basis.

Next, the tax would affect all sorts of institutional investors (investment banks, mutual funds, hedge funds, etc.). Currently, these funds average transaction fees of 7 basis points. Adding a tax of 50 basis points would radically affect their returns and cause them to cease activity. Additionally, most 401(k)s are invested in these types of funds, so the tax would essentially be reducing the value of investors retirement accounts. Another important point to note is that by taxing bond transactions, the government is inhibiting the ability to raise capital for not only corporations, but itself.

Obviously, this is all conjecture, but it is not entirely baseless. Sweden, in 1984, introduced a 50 basis point tax on all equity transactions. In 1986, the tax was doubled to 100 basis points. After this second announcement, 60% of the traded volume of the 11 most actively traded Swedish share classes, accounting for 50% of all Swedish equity trading volume, relocated to London. By 1990, more than half of all Swedish securities trading had moved offshore. The government reacted to this by introducing a tax on fixed income securities. Within a week of the introduction of the tax, the volume of bond trading fell by over 85%, futures trading fell by 98% and the options market ceased to exist. Also, the incremental revenue generated by the equity tax was almost entirely offset by the loss in capital gains tax. (More information about this tax can be found here)

This post was inspired by my reaction to How to Avoid Another Market Crash, by Douglas Cliggott (Lecturer of Economics at University of Massachusetts Amherst). Contrary to his favorable view, I think introducing Bernie Sanders’s tax on the capital markets is a bad idea. It is one that will overall generate much greater costs than benefits. It will severely inhibit firms ability to raise capital and by reducing liquidity, may actually serve to magnify volatility in the markets. It is by no means, as Douglas Cliggott would have you think, a perfect tax.

Farqani Mohd Noor: Malaysia Should Maintain a Flexible Exchange Rate for Monetary Independence

Link to Farqani Mohd Noor’s LinkedIn Homepage

I am delighted to host another student guest post by Farqani Mohd Noor. This is the 5th student guest post of this semester. You can see all the student guest posts from my “Monetary and Financial Theory” class at this link.

The other day, my brother, a dentist, was furious on Whatsapp, complaining about the depreciating Ringgit. He said, “80% of my dental materials are imported, and they’re 25% more expensive now. But the government is not increasing allocation of funds for them. How am I supposed to give my services to the people?!”

Commodity-exporting countries are facing depreciating currencies due to the current economic landscape; US interest rates are uncertain, China is combating a housing bubble and a stock market crash, and commodity prices are fluctuating. These factors are affecting the supply and demand for currencies. Malaysia, one of the affected countries, is now selling $ 4.4 Malaysian Ringgit (MYR) for $1 USD.

My brother continued, “At this rate we will reach $5 MYR for 1 USD. Why not peg the currency?”

I fell silent, trying to formulate a witty economic response. I recall reading Milton Friedman. He said, “A country that pegs the exchange rate is essentially committing itself to adopt the economic policies of the country whose currency it is pegged to.”

The idea of pegging MYR to the USD is familiar to Malaysians as Dr. Mahathir, the former Malaysian Prime Minister, banned offshore market trading of the ringgit and pegged it to $3.8 USD during the 1997 Asian Financial Crisis. Consequently, the country recovered from the crisis faster than our Southeast Asian peers (Indonesia and Thailand). This unorthodox method was successful with the help of the central bank.

The central bank has control over MYR through foreign reserves. The $95 billion USD of foreign currency reserves in Malaysia will not sufficient to peg the currency in the long run; they will eventually run out of ammunition. The central bank will have to borrow foreign currency in efforts to meet the demand for foreign currency. Shrinking of the foreign reserves and the cost of accumulating them means more RISK in the economy. Therefore, I conclude that foreign reserves serve as an instrument for the central bank to smooth the currency but not to fix them at a certain rate.

In order to face these risks during the 1997 Asian Financial Crisis, Dr. Mahathir implemented selective capital controls in order to circulate MYR within the country. For example, investments above $10000 MYR to non-residents will require permission from the central bank. Dr. Mahathir also implemented in an expansionary fiscal policy worth $2 billion MYR for consecutive years until 2002. This was coupled with low interests rates from 11% in mid 1998 to 3% in the December 1999. These were efforts to stimulate spending during the times of recession and prevent MYR from leaving the country.

However, pegging currencies in current economic landscapes exposes Malaysia to different risks than that of 1997. Since fiscal policies are expensive, the government has to think twice of increasing spending. The government debt is much higher now than it was in 1997; it stands at more than 50% of GDP. With the introduction of Goods & Services Tax (VAT equivalent) and rationalization of subsidies, Malaysia has been going through a transitional period and prices have only begun to stabilize. Introducing more fiscal spending now will be counterintuitive to the efforts done to reduce the debt. But how will the Malaysian economy run under capital control with limited stimulus packages?

External landscapes, on the other hand, like Europe and China are also different from that of 1997. Europe is going through a difficult period, with the Greece Debt Crisis occurring during these last couple of months. China’s maturing economy is facing a sharp slowdown in exports and growth. These external economic landscapes matter because Malaysia is an exporting country – exports of goods and services measured by the World Bank is at 80% of GDP in 2014. Currently, US currency rates are appreciating against all other major currencies (not only MYR). If Malaysia’s currency is pegged against the USD, this will also appreciate the MYR against other currencies in the world. The appreciated currency will reduce major exports and destroy manufacturing businesses (main export sector) like electrical & electronic products (35% of Malaysia’s total exports), as prices will be more expensive than competitors in Thailand, Indonesia and China

Finally, The US Fed also plans on tightening monetary policies and increasing fed interest rates. These are policies that will prevent Malaysia from stimulating the country’s economy, if it decides to peg the MYR to USD. In the end, Malaysia will find itself facing a technical recession just like how Chile, and Argentina did when they pegged their currencies against USD. Malaysia needs monetary independence in order to face its own economical challenges that are different from the US. Moreover, in 1997, currency speculation created the Asian Financial Crisis. However, currently, political scandals and economical challenges are depreciating the MYR. Thus, we need policies to solve our problems and not limit them.

Given what I’ve said, Malaysia’s economic fundamentals are much stronger than it was in 1997. Thus, while pegging the currency might not be an option, I hope Malaysia can adjust to the supply and demand of MYR in the market. It’s been almost two decades since 1997, during which Malaysia has survived, recovered, and grown through the 2008 financial crisis.

But I did not have time to formulate these thoughts in a text message due to the need to write this post for class! So I replied to my brother’s comments, “Economies are cyclical. There’s a boom and a bust. Be patient in face of economic slowdown because no currency can defy economic principles especially not the MYR.”

Angus Deaton Wins Nobel Prize—Official Press Release →

Congratulations to Angus Deaton on a richly deserved Nobel Prize!

I have intersected with Angus Deaton both early on in a common interest in precautionary saving and currently in a common interest in the economics of happiness and the construction of indices of National Well-Being. It has been a delight talking with Angus about many scientific issues in connection with a current grant proposal on measuring National Well-Being that both of us are a part of. Because of his considered judgment, I respect Angus’s opinions more than those of just about any other economist on the planet. If after clarification and a few minutes argument with him, I ever found I disagreed with him, my first thought would be that I was probably wrong.

Greg Robb: Fed Officials Seem Ready to Deploy Negative Interest Rates in Next Crisis

Link to the article on Market Watch

Greg Robb interviewed me on Friday evening, October 9, and by the next morning had this incisive article out. You should read the entire article, but here is the part based on our interview:

Although negative rates have a “Dr. Strangelove” feel, pushing rates into negative territory works in many ways just like a regular decline in interest rates that we’re all used to, said Miles Kimball, an economics professor at the University of Michigan and an advocate of negative rates.

But to get a big impact of negative rates, a country would have to cut rates on paper currency, he pointed out, and this would take some getting used to.

For instance, $100 in the bank would be worth only $98 after a certain period.

Because of this controversial feature, the Fed is not likely to be the first country that tries negative rates in a major way, Kimball said.

But the benefits are tantalizing, especially given the low productivity growth path facing the U.S.

With negative rates, “aggregate demand is no longer scarce,” Kimball said.

Here is a quotation I sent him over email he didn’t have space to use:

Monetary policy can’t take care of long-run growth or financial stability. But, even if we had to face again something as terrible as the Great Recession, interest rate policy alone–without any help from quantitative easing or fiscal stimulus–could provide as much aggregate demand as needed once a central bank gets cash out of the way. And it is easy to get cash out of the way by adjusting how the central bank handles paper currency. The key is to make dollars (or euro or yen) in the bank the center of the monetary system, not paper money.

For more on negative interest rates, see my bibliographic post How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide. There is a 5 minute video there you should watch first, then you can browse through many links.

A Core Mormon Doctrine in a Tweet

“Exaltation is our goal, discipleship is our journey”–not bad, when reinterpreted in a nonsupernatural way.

I comment on a few other tweets from the Mormon Church’s official Twitter feed in this Storify story.

Cyrus Anderson: Hot Property in China

Link to Cyrus Anderson’s Google Sites Homepage

I am delighted to host another student guest post by Cyrus Anderson. This is the 4th student guest post of this semester. You can see all the student guest posts from my “Monetary and Financial Theory” class at this link.

The People’s Republic of China should defuse the property bubble by addressing the underlying issues and taking a larger role in implementing affordable housing.

Yifan Xie writes of the woes of China’s property market in a recent Wall Street Journal article, describing the plight of RiseSun and in particular an apartment complex in Bengbu it owns. The complex is described as a ‘Toscana-style high-end community’, but there are no buyers in what is normally the season for property sales and RiseSun’s financial outlook appears risky. This downturn is not isolated to smaller cities; the cities in Fujian have not kept up the pace either. Properties sales there fell 16.3 percent in the first two months from a year earlier, according to an article in South China Morning Post.

This goes to show an excess in housing. But, this is only in higher-end housing. There are many people that would want to buy a home, but cannot afford to do so. It is not entirely the private sector’s fault. There are land shortages in many urban areas and redevelopment projects are difficult due to fragmented ownership, according to an article by Haotian Lin. But there are still problems with what property developers have done so far. Haotian Lin continues, “many of these housing projects are located at the urban fringe where infrastructure still needs to be improved and where there are not many job opportunities. This means high costs on commuting, which can make the housing ‘unaffordable’”. Quality of the residences has also been a problem. Local governments pushed developers to build the quantities stipulated by the central government, but have not ensured quality.

In order to effectively implement affordable housing, the central government will have to redesign the incentive structures and possibly take a larger role in carrying out the process. It can do more to build affordable housing in areas from which potential workplaces and other needs are accessible. To address the shortage of well located land, it could offer fairer channels for land conversion such as the successful land leasing in Shenzhen. Policymakers should also revamp the incentives the development of affordable housing, in order to help offset the high cost of land in accessible locations. This could include holding the developers and the local government officials in charge accountable for meeting some set quality standards. The other side to this is to also make it easier for consumers to buy the homes. Expanding access to housing finance is one idea, but it is not new. Some cities and provinces are taking steps in this direction. In Fujian the downpayment required for first-time buyers was lowered to 20 percent from 30 percent, just after Jinan and Guangzhou lowered theirs. Another step would be to extend financing to migrant workers, many of who may face barriers such as the hukou permit.

According to a McKinsey report, “China’s affordable housing gap (the difference between market-rate housing costs and 30 percent of income for households in lower-income groups) equates to about $180 billion per year, or about 2 percent of GDP”. Integrating these groups will take significant effort, but in the long run, will result in a higher quality of life and a stronger economy. In the meantime, the property market could stand to benefit from this endeavor.

Ben Bernanke on Trial

Previewing his upcoming book The Courage to Act: A Memoir of a Crisis and Its Aftermath slated to come out the next day, Ben Bernanke discussed recent monetary policy history and general principles of monetary policy in the October 4, 2015 Wall Street Journal op-ed “How the Fed Saved the Economy.” He said a number of important things very well. Here are my favorite passages. I added headings, but the words in the indented bits are Ben’s. After quoting Ben, I give my take on his record at the Fed.

The Limits of Monetary Policy

Fed critics sometimes argue that you can’t “print your way to prosperity,” and I agree, at least on one level. The Fed has little or no control over long-term economic fundamentals—the skills of the workforce, the energy and vision of entrepreneurs, and the pace at which new technologies are developed and adapted for commercial use.

What Monetary Policy Can Do

What the Fed can do is two things: First, by mitigating recessions, monetary policy can try to ensure that the economy makes full use of its resources, especially the workforce. High unemployment is a tragedy for the jobless, but it is also costly for taxpayers, investors and anyone interested in the health of the economy. Second, by keeping inflation low and stable, the Fed can help the market-based system function better and make it easier for people to plan for the future. Considering the economic risks posed by deflation, as well as the probability that interest rates will approach zero when inflation is very low, the Fed sets an inflation target of 2%, similar to that of most other central banks around the world.

The Record for the US, the UK and the Eurozone Indicates that the Great Recession Called for Monetary Stimulus

Europe’s failure to employ monetary and fiscal policy aggressively after the financial crisis is a big reason that eurozone output is today about 0.8% below its precrisis peak. In contrast, the output of the U.S. economy is 8.9% above the earlier peak—an enormous difference in performance. In November 2010, when the Fed undertook its second round of quantitative easing, German Finance Minister Wolfgang Schäuble reportedly called the action “clueless.” At the time, the unemployment rates in Europe and the U.S. were 10.2% and 9.4%, respectively. Today the U.S. jobless rate is close to 5%, while the European rate has risen to 10.9%. …

Meanwhile, the United Kingdom is enjoying a solid recovery, in large part because the Bank of England pursued monetary policies similar to the Fed’s in both timing and relative magnitude.

The Supply Side

With full employment in sight, further economic growth will have to come from the supply side, primarily from increases in productivity. … As a country, we need to do more to improve worker skills, foster capital investment and support research and development.

My Take on Ben’s Record

Ben has been criticized for many things. I think that higher equity requirements–including mortgage reform involving more equity provided by not just homeowners but other investors to get higher equity requirements for mortgages–and sovereign wealth funds are the right tools to deal with financial instability, not monetary policy, so I certainly don’t follow the chorus faulting the Fed for causing bubbles by keeping interest rates too low in 2003. (Ben was not Chair then, but he was an influential Governor.)

Ben, however, like many of the rest of us (I definitely include myself) did not do enough to recognize building financial instability and push for higher equity requirements before things blew up in 2008. My now deceased University of Michigan colleague Ned Gramlich was one of the few within the Federal Reserve Board who recognized some of these building problems when he served as a Governor of the Federal Reserve Board. Like Alan Greenspan, Ben should have paid more attention to Ned, and Ned should have been more insistent on his point.

In later decisions, in hindsight, Ben should probably have pressed to save Lehman. But it is not at all clear that could have arrested the crisis, since some other bank might have then failed and pulled things down.

Nevertheless, once Lehman fell, Ben’s actions were heroic, both in helping to push through the unpopular but necessary bailouts and in bringing the Fed around to a serious program of quantitative easing that helped greatly, as Ben points out in one of the passages above.

Overall, Ben is a hero in my book. The mistakes he made are mistakes I think I would have made myself. (I know that, because I have a reasonably good memory of what I thought in real time along the way.) But what he did right was something that very few people could have done as well.

Going forward, for the future of monetary policy, my wish would be for Ben Bernanke to help in pushing for a further expansion of the monetary policy toolkit. Despite Ben’s heroic actions, the actual outcome of US monetary policy–7 years of sluggish growth and zero interest rates–was terrible in absolute terms. There is a simple reason why: the zero lower bound. As far as I know, Ben has yet to acknowledge publicly the fact that the zero lower bound is a policy choice, not a law of nature–and that ways to eliminate the zero lower bound are quite practical. See my bibliographic post “How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide.” In recognizing and discussing publicly how easy it is to break through the zero lower bound, Bank of England Chief Economist Andrew Haldane is ahead of Ben. As things stand, the Bank of England is poised to do a much better job in the next serious recession than the Fed. Ben could do a lot to fix that by speaking frankly about the welcome fragility of the zero lower bound.

Neil Irwin: How the Stanford Economics Department is Mounting a Challenge to Harvard and MIT →

The most interesting thing to me in this article is Neil’s discussion of the shift in emphasis within economic towards heavy-duty empirical work.

Anand Jetha: Slow Progress in Battery Technology Will Hold Back Electric Cars

Link to Anand Jetha’s LinkedIn Homepage

I am delighted to host another student guest post by Anand Jetha, the 3d of this semester.

The battery is the biggest obstacle in technological progress, and ultimately the barrier for the all-electric vehicle to become a major participant in the automotive market.

Every day it seems there is a new gadget that rolls out doing something amazing, something innovative. Phones get lighter, thinner, and more powerful. Laptops are built thinner than our hands. Google has cars driving themselves. Tesla provides cars that drive themselves from your garage to the curb at any time you choose, and have all your comfort settings including temperature and radio adjusted. But the thing powering that ready to go car at the curb and the cell phone in your hands has barley changed in eight years. Processing power doubles every two years according to Moore’s law, but today’s battery cannot even hold 30% more power than a battery from 2007. This means each year your electric car battery can only hold 3% more power. That’s nowhere near the 50% per year growth we see in the processing power of that self-driving electric car.

But how can that be? We have so many more electronics using battery power today including laptops, fitness trackers, smart watches, phones, Xbox/PS4 controllers, electric razors, and many more. The demand for batteries is growing significantly so why isn’t the innovation following? The problem has to do with the limits of mass when it comes to the lithium in the batteries. They just can’t be squeezed any closer together.

A recent article in the Wall Street Journal titled “Porsche Unveils Prototype Battery-Driven Sports Car” highlights the new desires for auto companies to build all electric vehicles and plug-in hybrids. The article talks about Porsche’s new “Mission E” car as well as Audi’s “e-torn Quattro” and BMW’s “i8” which all push for fully electric performance cars. They claim that the driving experience is all that still matters, not the fuel. All three are getting amazing press coverage as they keep improving the efficiency of all-electric vehicles. The problem is even with this new focus for EV, they make up less than 1% of all vehicles in the United States.

That low market share starts to make sense once the limiting factor of the battery is accounted. The most expensive part of the electric cars is the battery that powers them. They add a significant cost to making the car. Take for example the Ford Focus ST, which is their highest tier gas model that sells for $24,425. Now add a battery to it and make it a plug-in hybrid and the costs shoots up to $29,170. And that is just a hybrid, which has a smaller battery than an all-electric vehicle. After the cost comes the problem of charging the current batteries. I can pull up to a gas station and fill my car in about 10 minutes. If I want to charge my Tesla at my house after paying to have a special charger installed, would take about 5 hours for a full charge. Our current batteries are very difficult to charge quickly. Now comes the issue of the size of the battery. The tesla gets at best 270 miles of range before I need to stop and charge for another 5 hours. Other than my interest in limiting my carbon footprint, I have no desire in driving a battery powered car that will force me to change my lifestyle.

Sure, the all-electric car is getting all kinds of converge but remember that their current market share is less than 1% in the US. The only way automakers will be able to sell these cars as something other than status symbols is if they magically create improvements in the power source.