“Real difficulties can be overcome; it is only the imaginary ones that are unconquerable.”

– Theodore Vail. Hat tip to Joseph Kimball for this quotation.

A Partisan Nonpartisan Blog: Cutting Through Confusion Since 2012

“Real difficulties can be overcome; it is only the imaginary ones that are unconquerable.”

– Theodore Vail. Hat tip to Joseph Kimball for this quotation.

John Stuart Mill’s discussion of the regulation of bars and the like in paragraph 10 of On Liberty “Chapter V: Applications” touches on many key issues that arise for contested laws:

He writes:

The question of making the sale of these commodities a more or less exclusive privilege, must be answered differently, according to the purposes to which the restriction is intended to be subservient. All places of public resort require the restraint of a police, and places of this kind peculiarly, because offences against society are especially apt to originate there. It is, therefore, fit to confine the power of selling these commodities (at least for consumption on the spot) to persons of known or vouched-for respectability of conduct; to make such regulations respecting hours of opening and closing as may be requisite for public surveillance, and to withdraw the license if breaches of the peace repeatedly take place through the connivance or incapacity of the keeper of the house, or if it becomes a rendezvous for concocting and preparing offences against the law. Any further restriction I do not conceive to be, in principle, justifiable. The limitation in number, for instance, of beer and spirit houses, for the express purpose of rendering them more difficult of access, and diminishing the occasions of temptation, not only exposes all to an inconvenience because there are some by whom the facility would be abused, but is suited only to a state of society in which the labouring classes are avowedly treated as children or savages, and placed under an education of restraint, to fit them for future admission to the privileges of freedom. This is not the principle on which the labouring classes are professedly governed in any free country; and no person who sets due value on freedom will give his adhesion to their being so governed, unless after all efforts have been exhausted to educate them for freedom and govern them as freemen, and it has been definitively proved that they can only be governed as children. The bare statement of the alternative shows the absurdity of supposing that such efforts have been made in any case which needs be considered here. It is only because the institutions of this country are a mass of inconsistencies, that things find admittance into our practice which belong to the system of despotic, or what is called paternal, government, while the general freedom of our institutions precludes the exercise of the amount of control necessary to render the restraint of any real efficacy as a moral education.

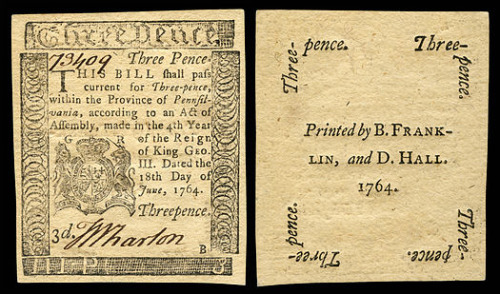

Following up on “Owen Nie: Playing Card Currency in French Canada,” Owen Nie offers here another guest post on monetary history. This one is drawn from Richard Lester’s “Currency Issues to Overcome Depressions in Pennsylvania, 1723 and 1729.” Monetary Experiments: Early American and Recent Scandinavian. New York: Augustus M. Kelley, 1970. 56-111.

This chapter provides a detailed account of the two attempts, in 1723 and in 1729, to combat depression by monetary expansion in Pennsylvania prior to the Revolutionary War. Before this monetary experiment, the scarcity of metallic money, a result of the lack of mints in North America and the prohibition by the British government of exporting gold and silver to the colonies, was widely considered a cause for business depression in Pennsylvania as well as in other North American colonies in various historical accounts. In answer to the scarcity of a medium of exchange, the Pennsylvania Assembly passed an act in 1723 to issue 15,000 pounds of paper money as a remedy. This soon brought about a remarkable recovery in business conditions and trade activities (mostly British imports into Pennsylvania) without engendering inflation and runaway speculation. By 1729 the necessity for additional monetary expansion was becoming apparent and hence a bill to issue an additional 30,000 pounds was passed and a new round of revival of business soon ensued. The two monetary expansions enabled Pennsylvania to enjoy more favorable price levels and exchange rates in the following years. Pennsylvania’s success and prosperity was such that the colonists protested vehemently when the British Board of Trade prohibited the American colony from issuing paper money in 1764. There seem to be general agreement that these currency expansions, with combating depression as their sole objective, had been a remarkable success.

Here is the full text of my 65th Quartz column, “An economist explains why a key to the free world lies with China,” now brought home to supplysideliberal.com. It was first published on July 3, 2015. Links to all my other columns can be found here.

Ori Heffetz pointed out the error of my counting 239 years (“almost a quarter of a millenium”) of freedom in the United States since 1776, since the key date for freedom in the United States can’t be counted any earlier than the adoption of the 13th Amendment to the Constitution on December 18, 1865 abolishing legal slavery in the US. We are coming up on the 150th anniversary of that event later on this year. This actually reinforces my statement in the first sentence of the column that freedom is a rarity in human history. I am leaving this error in the column itself, because it is an instructive error, once pointed out.

In addition to comments here, don’t miss the comments and debate in reaction to my first link to the Quartz column.

If you want to mirror the content of this post on another site, that is possible for a limited time if you read the legal notice at this link and include both a link to the original Quartz column and the following copyright notice:

© July 3, 2015: Miles Kimball, as first published on Quartz. Used by permission according to a temporary nonexclusive license expiring June 30, 2020. All rights reserved.

Freedom is a rarity in human history, and still too much of a rarity in the world today. This should be no surprise. Would-be tyrants abound, and it is not easy to establish a system that keeps them all in check. The wonder is that we can celebrate the better part of a quarter of a millennium of freedom in the United States, and comparable freedom in some other lucky countries.

When Dan Benjamin, Ori Heffetz, Nichole Szembrot and I surveyed more than four and a half thousand Americans about what they viewed as the most important objectives for public policy, the top two (of 131 choices) were “freedom from injustice, corruption, and abuse of power in your nation,” and “people having many options and possibilities in their lives and the freedom to choose among them.”

This pairing of responses shows an awareness of the danger to freedom from those who would organize the institutions of a nation to serve the interests of an in-group at the expense of an out-group. At the beginning of the struggle toward freedom, the in-group is very small and the out-group large. At later stages of the struggle toward universal freedom, the in-group will be large and the out-group small. But adding up across the world, it is not at all clear that a majority of the people in the world today can be called truly free.

In international struggles for freedom, the advantage free nations have had in per capita income has helped to keep them from being overwhelmed by a coalition of dictatorships and oligarchies. As Daron Acemoglu and James Robinson argue in Why Nations Fail, the level of economic freedom necessary to enjoy the full benefits of innovation presents a constant danger of undermining the power of those currently in charge. As long as a country is getting up to speed on existing technologies and settled best practices, such dangers can be kept within bounds. But, a small in-group with a toehold on power is loathe to allow a creative adventure into the unknown that could transform the political arena as well as the economy.

The key to the future of freedom in our world is China. Its one-and-a-quarter billion people and high rate of economic growth are the reasons its course is so important to the future:

Thus, over a horizon of two or three decades, China is dangerously unpredictable. The last three possibilities—Chinese civil war, a Chinese Putin, or continued dominance by an oligarchy that attacks freedom as a faulty Western conceit—all represent serious dangers to the progress of freedom in the world, as well as to peace. The imperative of raising the likelihood of full freedom in China means that trying to stand in the way of Chinese economic growth is not the answer. And one should remember Berkeley economist Brad DeLong’s question: “Does it really improve the national security of the United States for schoolchildren in China to be taught that the United States sought to keep them as poor as possible for as long as possible?”

If one rejects the fool’s errand of trying to stunt the economic growth of a dangerously unpredictable China, the best course to protect freedom and relative peace in the world is to make the free world stronger: numerically, economically, militarily, and in the quality of life freedom can be shown to provide. On all of these fronts, I worry about what I see as a lack of seriousness by the leaders and citizens of the free world about meeting the challenge of China.

Bringing more people into the free world is easier than it sounds. The key is to focus on people, not patches of ground. Although it is hard to bring a patch of ground currently subject to an oppressive regime under free institutions, the economic importance of land—apart from what is on top of the land—continues to decline relative to the importance of people, education and training, ideas and capital. Once one focuses on people, the answer is clear: bring people to where freedom already rules. That is so easy it is hard to do the opposite. Many people in benighted countries seek freedom and the prosperity that full freedom enables. Standing in the way of those hopes, many otherwise free countries make strenuous efforts to keep those people seeking prosperity and freedom out.

The rhetoric is all about those hoping to join the free world taking away the jobs of those already there. Forgotten is the fact that those hoping to join the free world will also serve in the armed forces and pay taxes to support those armed forces, as well as raise children who will invent the technologies that can help us meet the challenge of China economically as well as militarily. (For the record, the only persuasive evidence for immigrants materially hurting the job prospects of those already here is for them hurting the job prospects of other recent immigrants.)

Despite the relative difficulty of bringing nations closer to full freedom, there is important work to be done in that arena—particularly in solidifying and deepening freedom in nations that are well along the road toward freedom, but need to go further. The people in Turkey recently voted decisively against creeping dictatorship. I agree with The Economist in calling for the European Union to move forward with admitting Turkey in order to solidify those gains. And because of the number of people involved, helping India reach its full potential is of crucial importance for the free world.

It is much better to have the democratic tug of war between different groups each looking to get their share of the pie than it is to have one favored group that alone gets its way. But when it comes to strength in a dangerous world, it is the size of the pie that matters most. Economists actually have excellent tools for understanding what it takes to foster economic growth. Monetary policy tools for stabilizing the economy are advancing faster than most people realize.

And although issues of taxation and certain labor market rules continue to be contentious, there is broad agreement among economists about many key measures to foster long-run economic growth: improving education, pouring resources into research and development, and preserving economic freedom: the ability to do new things in new ways without your competitor being able to get the government to stop you. In the area of economic policy, one of the biggest problems is simply the amount of political airtime taken up by a small set of issues that leaves little time to discuss everything else.

Militarily, one of the free world’s successes is now also a weakness. After World War II, great efforts were made to encourage pacifism in Japan and Germany. Those efforts bore remarkable fruit. Anyone who spends any time in Japan or Germany soon learns how deep pacifism runs in those countries now. Japan’s pacifism only affects its own military efforts, but Germany’s pacifism has contributed to pacifism in the rest of Europe. For the rest of the free world, I would riff on St. Augustine by saying “Make me pacifist, but not yet.” Peace is important, but so is freedom. Let freedom triumph; then we can hope to be able to afford pacifism. In the meanwhile, the pacifism of Japan and Germany means that the rest of the free world needs to shoulder a bigger military burden.

Given numerical and economic strength–fostered by more immigration, education, research and economic freedom–there is no lack of ideas for how to turn technological sophistication and military spending into military strength (with all the frightfulness inherent in military strength). A fascinating article in The Economist details some of these ideas:

For the free world, the objective of military strength is not war, but deterrence. What all scenarios for China’s future hold in common is that China is likely to behave better if it faces a relatively strong American military than if it faces weakness.

When the free world does well, it is much harder for the unfree world to keep out the winds of freedom. But autocracies use every failure of the free world to argue that autocracy isn’t so bad in comparison. In making the case for freedom, good economic policy in the free world goes a long way. But making sure that the benefits of freedom extend to everyone is also crucial.

Some argue that the way to make sure that the benefits of freedom extend to everyone is to expand government social programs. But the use of government power when it is not necessary is itself an affront to freedom, since people are in effect being told to “get with the program” or be thrown in jail. I don’t think we currently know how to get done what needs to be done with a doctrinaire libertarian approach, but we can edge in that direction. People want to help others who are less fortunate. The only thing that stops them from doing what needs to be done voluntarily is concern about the time and resources that might take away from their own families.

So, as I advocated here in “Yes, There is an Alternative to Austerity vs. Spending: Reinvigorate America’s Nonprofits,” it is enough to use the arm of the government to require more substantial charitable contributions, while giving people wide latitude to decide which particular causes they want to support. This can both assist in things the government is now doing, such as taking care of senior citizens and supporting medical research, and begin to take care of things that should be done, but aren’t. With millions of people each required to do something, but allowed to think and decide for themselves what most needs to be done, the odds that the benefits of freedom and prosperity extend into all the nooks and crannies of society improve dramatically.

Finally, though efforts to measure national well-being in ways that respect the full range of things human beings care about are still in their infancy, there is hope that developing such measures as counterpoints to GDP can guide public policy toward ways of improving the quality of life in nations that use them in unexpected ways. Such measures of national well-being might also be used by autocrats to keep those they rule over just happy enough to forestall rebellion, but those rulers would be faced with this truth: people love freedom, and will never be content for long without it.

“These different defenses of literature are connected with different conceptions of democracy. The world-citizen view insists on the need for all citizens to understand differences with which they need to live; it sees citizens as striving to deliberate and to understand across these division. It is connected with a conception of democratic debate as deliberation about the common good. The identity-politics view, by contrast, depicts the citizen body as a marketplace of identity-based interest groups jockeying for power, and views difference as something to be affirmed rather than understood. Indeed, it seems a bit hard to blame literature professionals for the current prevalance of identity politics in the academy, when these scholars simply reflect a cultural view that has other, more powerful sources. Dominant economic views of rationality with the political culture have long powerfully promoted the idea that democracy is merely a marketplace of competing interest groups, without any common goals and ends that can be rationally deliberated. Economics has a far more pervasive and formative influence on our life than does French literary theory, and it is striking that conservative critics who attack the Modern Language Association are slow to criticize the far more powerful sources of such anticosmopolitan ideas when they are presented by market economists. It was no postmodernist, but Milton Friedman, who said that about matters of value, ‘men can ultimately only fight.’ This statement is false and pernicious. World citizens should vigorously criticize these ideas wherever they occur, insisting that they lead to an impoverished view of democracy.”

– Martha Nussbaum, Cultivating Humanity: A Classical Defense of Reform in Liberal Education, pages 110-111 (in chapter 3).

At the University of Michigan we have a student-selected “Golden Apple” award for excellent teachers. The winners traditional give an “Ideal Last Lecture.” I liked the 12 life lessons Golden Apple Winner Stephen Strobbe gave. (You can see the full article in the University of Michigan’s University Record here.) Here they are:

Unlike Bank of England Chief Economist Andrew Haldane’s position described in Jennifer Ryan’s Bloomberg Business article linked above, I am doubtful that the UK needs lower interest rates right now. But if it did, Andrew Sentance, a former member of the Bank of England’s monetary policy committee is wrong in saying “There’s not much lower you can go, and a cut to 0.25 percent isn’t going to have a significant impact on the economy” (as quoted in the article). The Bank of England has actually been quite interested in eliminating the zero lower bound, as indicated by making Ken Rogoff and me keynote speakers at their conference on the future of money in May 2015.

Here is the full text of my 64th Quartz column, “Radical Banking: The world needs new tools in the fight against the next recession,” now brought home to supplysideliberal.com. It was first published on June 25, 2015. Links to all my other columns can be found here.

If you want to mirror the content of this post on another site, that is possible for a limited time if you read the legal notice at this link and include both a link to the original Quartz column and the following copyright notice:

© June 25, 2015: Miles Kimball, as first published on Quartz. Used by permission according to a temporary nonexclusive license expiring June 30, 2020. All rights reserved.

The cover of the June 13th Economist magazine trumpets “Watch out: The world is not ready for the next recession.” Within, the cover story explains:

When central banks face their next recession, in other words, they risk having almost no room to boost their economies by cutting interest rates. That would make the next downturn even harder to escape.

The Economist is wrong.

The proof that the Economist is wrong could be heard in a remarkable May 18 conference in London, not far from the Economist’s offices. The conference had an impressive list of co-sponsors–the Brevan Howard Centre for Financial Analysis, the Centre for Economic Policy Research (CEPR), Imperial College Business School, and the Swiss National Bank—who chose the audacious title “Removing the Zero Lower Bound on Interest Rates.” In other words, the conference organizers were announcing at the top of the program to the assembled central bankers, academics, and financial industry participants their belief that any limits on how much interest rates can be cut can be swept away. That conference was followed by another conference the next day at the Bank of England, with the same theme.

If interest rates can be cut as much as necessary, central banks alone have plenty of firepower to end the next recession, even without any help from fiscal policy. Given the limits to fiscal policy coming from political squabbles and concerns about adding to national debt, monetary policy unhampered by limitations on central banks’ interest rate targets would be good news indeed. For example, if the Fed could have cut interest rates to -4% throughout 2009, the US could have had a robust recovery by the end of 2009 instead of bad economic times dragging on as long as they did.

I spoke at both conferences. The Centre for Economic Policy Research arranged for interviews of several participants at the lunch break of the “Removing the Zero Lower Bound” conference, and did a brilliant job of editing those interviews into videos with high production values. You can see links for all of the interviews here. All of these interviews take negative interest rates very seriously. Collectively, the full set of interviews gives a sense of how much attitudes are shifting.

The three most radical interviews—arguing that there may ultimately be no limits to how low interest rates can go when necessary to bring economic recovery–are with Citigroup’s Chief Economist Willem Buiter

with Martin Andersson, from Sweden’s Ministry of Finance

and with me

The key to unlimited firepower in monetary policy is to deal with the problem of people storing cash. As I describe in my interview, my own approach to avoiding the problem of people storing paper currency to get an interest rate close to zero rather than the intended negative interest rate during a serious downturn is to charge private banks a deposit fee when they turn in cash at the cash window of the central bank for credit in their reserve accounts with the central bank.

Such a charge at the cash window of the central bank closes the loophole that would otherwise allow financial firms to earn a zero interest rate (minus storage costs) by using cash. In this system, regular people who are saving for long periods of time could still in all likelihood earn positive interest rates on bank accounts and a zero rate on cash over longer periods of time, but the ability to earn a zero interest rate from cash would be temporarily suspended during the worst of an economic downturn. As a result, other interest rates could be pushed down as low as necessary to heal the economy.

After these two conferences, I visited the Bank of Finland as well as the central banks of Sweden, Norway and Canada to explain at length my views on how to enable central banks to cut interest rates as much as they think they should, without being stopped short by the problem of paper currency storage. As compared to my visits to central banks before the conference I find the change in attitudes toward the possibility of deep negative interest rates as a result of these conferences has been dramatic.

The Sveriges Riksbank in Sweden already has negative interest rates, and could easily go further.

The Bank of Canada is less likely to need negative interest rates in the immediate future, but already has an “Effective Lower Bound” working group focused on exploring the possibilities for negative interest rate policy in the next recession. After the London conferences, and my extended discussions with them, these central banks are all thinking more seriously about the possibility that the danger of massive paper currency storage in a negative interest rate environment can be averted by appropriate action at the cash window of a central bank.

Introducing new tools for monetary policy is inherently controversial, but recent years have seen important additions to what is seen in most central banks as the acceptable toolkit: the use of quantitative easing (QE) and more recently the use of mild negative interest rates. Modifications to the way paper currency is handled at the cash window of the central bank to make deep negative rates possible could plausibly be the next major addition to the monetary policy toolkit. If so, the world could be better prepared to deal with the next recession than many people expect.

Michael Reddell has had a distinguished career in monetary policy making in New Zealand (as well as in Papua New Guinea and as an IMF appointee in Zambia). He recently retired from his job at the Reserve Bank of New Zealand and began a blog “Croaking Cassandra” about economic policy. (He also blogs about religion on his blog “Among Traditions.”)

I was delighted to get an email from him yesterday morning saying he had seen my talk at the New Zealand Treasury Friday, July 24 on the Economics of Happiness and would love to get together to talk about eliminating the zero lower bound. (I had spoken on Wednesday, July 22 at the Reserve Bank of New Zealand about eliminating the zero lower bound.) As it happened, I went to lunch a few hours later with both Michael Reddell and Carsten Schousboe (who is a Senior Health Economist at the Pharmaceutical Management Agency here in Wellington, the capital of New Zealand).

In his email introducing himself, Michael pointed me to this blog post, which he kindly agreed to let me mirror here. Here is what Michael had to say:

One of my persistent messages on my blog “Croaking Cassandra” has been that central banks and finance ministries need to be much more pro-active in dealing with the technological and regulatory issues that make the near-zero lower bound a binding constraint on how low policy interest rates can go, and hence on how much support monetary policy can provide in periods of excess capacity (and insufficient demand).

I’ve found it surprising that the central banks and governments of other advanced economies have not done more in this area. In most of these countries, policy interest rates have been at or near what they had treated as lower bounds since 2008/09. A few have been plumbing new depths in the last year or so, but half-heartedly (the negative rates have not applied to all balances at the central bank), and no one is confident that policy interest rates could be taken much below -50bps (or perhaps -75bps) without policy starting to become much less effective. The ability to convert to physical currency without limit is the constraint. There are holding costs to doing so, but for all except day-to-day transactions, the holding costs would be less than the cost of continuing to hold deposits once interest rates get materially negative. For asset managers and pension funds, for example, that shift would look attractive. I would certainly recommend that the Reserve Bank pension fund (of which I’m an elected trustee) transferred much of its short-term fixed income holdings into cash if the New Zealand OCR (Official Cash Rate) looked likely to be negative for any length of time.

I’ve been surprised by the lack of much urgency in grappling with this issue in other countries. I suspect there must have been a sentiment along the lines of “well, getting to zero was a surprise, and inconvenient, but we got through that recession, it is too late to do anything now, and before too long policy rates will be heading back up to more normal levels”. But they haven’t, despite false starts from several central banks. And each of these countries is exposed to the risk of a new recession, with little or no macroeconomic policy ammunition left in the arsenal. Interest rates can’t be cut, and the political limits to further fiscal stimulus are severe in most advanced countries.

If the rather sluggish reaction of other advanced country central banks (and finance ministries) is a surprise, the lack of any initiative by the New Zealand and Australian authorities is harder to excuse. Neither country hit the zero bound in 2008/09, or in the more recent slowdown (Australian policy rates are now at their lows, and commentators increasingly expect that New Zealand’s soon will be). The period since 2008/09 should have shown authorities that the zero lower bound is much more of a threat that most of us previously realised (not just, for example, a Japanese oddity). It should have suggested some serious contingency planning – as, for example, the Reserve Bank of New Zealand had done as part of whole of government preparedness for the possibility of a flu pandemic. Both countries have had years to get ready for the possibility of the zero lower bound. It is not as if the experience of the countries who have hit zero is exactly encouraging – slow and weak recoveries and lingering high unemployment.

But neither New Zealand nor Australia appears to have done anything about it. Indeed, in the most recent Reserve Bank of New Zealand Statement of Intent these issues don’t even rate a mention. I’m not suggesting it is the single most urgent or important issue the central banks face. Contingency planning never is, but that does not make doing it any less important. I’m also not suggesting that New Zealand is as badly placed as some – if we were to get to a zero OCR, our yield advantage would disappear and the exchange rate would probably be revisiting the lows last seen in 2000. And we have some more room for fiscal stimulus than some other countries. But no central bank or finance ministry should contemplate with equanimity the exhaustion of monetary policy ammunition. Nasty shocks are often worse than we allow for.

My prompt for this post is the visit to New Zealand this week of Miles Kimball, Professor of Economics at the University of Michigan (and an interesting blogger across a range of topics). Kimball has probably been the most active figure in exploring and promoting practical ways to deal with the regulatory constraints and administrative practices that make the ZLB a problem. They are all government choices. I’ve linked to some of his work previously. I noticed Kimball’s visit through a flyer for a guest lecture he is giving at Treasury on Friday, on a quite unrelated topic. I presume he will also be spending time at the Reserve Bank, addressing some of the monetary issues. This would seem like a good opportunity for some serious and enterprising journalist to get in touch with Kimball – whether directly, or via the Reserve Bank or Treasury – for an interview on some of his work in this area, and the reaction he is getting as he promotes his ideas, and practical solutions, around the world.

I’ve suggested previously that if our authorities are not willing to start on serious preparations to overcome the ZLB then the Minister should think much more seriously about raising the inflation target. I’d prefer to avoid a higher inflation target – indeed, in the long-run a target centred nearer zero would be good – but current inflation targets (here and abroad) were set before people really appreciated just how much of a constraint the zero lower bound could be. Better to act now so that in any future severe recession there is no question as to ability of the Reserve Bank to cut the OCR just as much as macroeconomic conditions warrant.

Here are some other previous posts where I have touched on ZLB issues:

“Aristotle saw people not as striving to maximize a state of satisfaction, and also not as striving to perform a list of duties. He saw them, instead, as striving to achieve a life that included all the activities to which, on reflection, they decided to attach intrinsic value.”

– Martha Nussbaum, Cultivating Humanity: A Classical Defense of Reform in Liberal Education, pages 119-120.

When Maryland tried to tax the Second Bank of the United States, Daniel Webster argued before the Supreme Court in McCulloch v. Maryland that “An unlimited power to tax involves, necessarily, a power to destroy.” The Supreme Court echoed his words, saying “That the power to tax involves the power to destroy … [is] not to be denied.” John Stuart Mill addressed the same issue in paragraph 9 of On Liberty “Chapter V: Applications,” but came to a different rule: taxation must be limited to no higher than the revenue-maximizing rate–otherwise, it is clear that the intent of the taxation is to destroy rather than to raise revenue. He wrote:

A further question is, whether the State, while it permits, should nevertheless indirectly discourage conduct which it deems contrary to the best interests of the agent; whether, for example, it should take measures to render the means of drunkenness more costly, or add to the difficulty of procuring them by limiting the number of the places of sale. On this as on most other practical questions, many distinctions require to be made. To tax stimulants for the sole purpose of making them more difficult to be obtained, is a measure differing only in degree from their entire prohibition; and would be justifiable only if that were justifiable. Every increase of cost is a prohibition, to those whose means do not come up to the augmented price; and to those who do, it is a penalty laid on them for gratifying a particular taste. Their choice of pleasures, and their mode of expending their income, after satisfying their legal and moral obligations to the State and to individuals, are their own concern, and must rest with their own judgment. These considerations may seem at first sight to condemn the selection of stimulants as special subjects of taxation for purposes of revenue. But it must be remembered that taxation for fiscal purposes is absolutely inevitable; that in most countries it is necessary that a considerable part of that taxation should be indirect; that the State, therefore, cannot help imposing penalties, which to some persons may be prohibitory, on the use of some articles of consumption. It is hence the duty of the State to consider, in the imposition of taxes, what commodities the consumers can best spare; and à fortiori, to select in preference those of which it deems the use, beyond a very moderate quantity, to be positively injurious. Taxation, therefore, of stimulants, up to the point which produces the largest amount of revenue (supposing that the State needs all the revenue which it yields) is not only admissible, but to be approved of.

Even apart from the need for revenue, it has always seemed to me that within reason taxes were a gentler way of discouraging something, more consistent with freedom than ironclad rules. The changes in defaults and framing that go by the name of libertarian paternalism or soft paternalism seem even gentler and yet more consistent with freedom.

In the arena of encouraging actions to help the environment, I personally often find social disapproval to be a more onerous, less freedom-respecting means of getting compliance than a modest tax with the same overall effectiveness (and with rebates to maintain neutrality vis a vis the income distribution) would be. It uses up a lot of air time in social interactions for people to be guilting others into green actions that could be encouraged subtly in the background of life with an appropriate Pigou tax. Maybe it is just me, but I often bridle at someone telling me directly what to do, but don’t have any psychological resistance to responding to price signals, within reason.

“Scientific progress makes moral progress a necessity; for if man’s power is increased, the checks that restrain him from abusing it must be strengthened.”

– Madame de Staël, The Influence of Literature upon Society. Thanks to my brother Joseph for reminding me of this quotation.

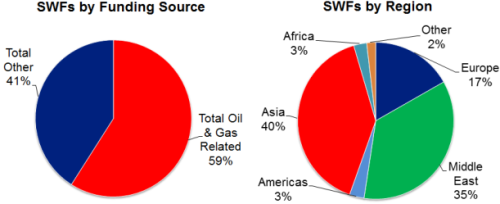

image source (2013)

In many blog posts and Quartz columns, I have argued that major economies such as the US should establish sovereign wealth funds even when issuing bonds is required to capitalize the funds. Sovereign wealth funds are already standard for countries that have positive net liquid assets. The new idea is to say that major countries that have negative net liquid assets should also have sovereign wealth funds as stabilization tools. A good post to turn to first for this is “Roger Farmer and Miles Kimball on the Value of Sovereign Wealth Funds for Economic Stabilization.”

In my tour of central banks to advocate eliminating the zero lower bound, I point out that even if monetary policy is someday done well enough to essentially keep the economy at the natural level of output all the time, there could still be a financial cycle. This possibility becomes clear if one writes down an entirely real general equilibrium noise trader model (as I have done in some very early stage research with Jing Zhang that might involve other coauthors before we are through). Even if the business cycle is entirely conquered in the sense of a zero output gap from sticky prices at all times, the financial cycle can cause welfare losses. Welfare losses can occur even when high enough equity requirements have taken away the implicit bailout subsidy for leverage. A contrarian sovereign wealth fund can help counteract the messed-up price signals caused by the noise traders.

In a July 19, 2015 post, “Skepticism About A U.S. Sovereign Wealth Fund,” Adam Ozimek worries about implementation difficulties for a sovereign wealth fund or other major economy. The first thing to say is that in general, institutions tend to be better in countries that–apart from natural resources–would be the richer ones, and so the right benchmark for the likely quality of a US sovereign wealth fund is Norway’s sovereign wealth fund rather than, say Saudi Arabia’s.

The second thing to say is that both Roger Farmer and I recommend a rule that the sovereign wealth fund is only allowed to invest in (low-fee) exchange traded funds. The importance of this is to keep the government from (a) micromanaging the investments and to keep the government from (b) voting the shares and micromanaging the behavior of the firms that way. In the US at least, if a sovereign wealth fund such as I recommend could ever be established, such aspects of the initial design of the fund can be maintained by the difficulty of getting changes opposed by one party through both Congress and a potential presidential veto. An initial bipartisan agreement on principles could not easily be broken.

The third thing to say is that I know in practice how to get the fund started off with a contrarian philosophy: I would recommend appointing John Campbell as the first head of the US Sovereign Wealth Fund.

On the objective of a sovereign wealth fund, the more I think about it, the more I realize that calculating the optimal policy for a large country’s sovereign wealth fund given a concern with overall social welfare in the usual way is a very interesting research problem. Basically, there is a technical answer to this question in the same sense that there is a technical answer for optimal monetary policy, after what I think is easier math than for optimal monetary policy.

The small country problem is, of course, even easier: a small country faces something much more akin to the standard portfolio problem, with the issue of what level of risk aversion to use when investing on behalf of a nation’s citizens. And of course, just as an individual household needs to integrate human capital into its portfolio decision, a small country sovereign wealth fund needs to integrate a wide variety of assets the country’s citizens and government already hold into its portfolio decision.