Kevin Grier and Norman Maynard on the Economic Consequences of Hugo Chavez

“We use the synthetic control method to perform a case study of the impact of Hugo Chavez on the Venezuelan economy. We compare outcomes under Chavez’s leadership and polices against a counterfactual of “business as usual” in similar countries. We find that, relative to our control, per capita income fell dramatically. While poverty, health, and inequality outcomes all improved during the Chavez administration, these outcomes also improved in each of the corresponding control cases and thus we cannot attribute the improvements to Chavismo. We conclude that the overall economic consequences of the Chavez administration were bleak.”

– Kevin Grier and Norman Maynard, abstract for “The economic consequences of Hugo Chavez: A synthetic control analysis"

How Negative Interest Rates Prevail in Market Equilibrium

Many people have the intuition that even if paper currency were out of the picture, other things that pay a zero interest rate would still create a zero lower bound, so that an attempt to take the target rate into deep negative territory would fail. Among them is one of the greatest economics bloggers of them all: John Cochrane. In his Grumpy Economist post “Cancel Currency?” he writes:

Suppose we have substantially negative interest rates – -5% or -10%, say, and lasting a while. But there is no currency. How else can you ensure yourself a zero riskless nominal return?

Here are the ones I can think of:

- Prepay taxes. The IRS allows you to pay as much as you want now, against future taxes.

- Gift cards. At a negative 10% rate, I can invest in about $10,000 of Peets’ coffee cards alone. There is now apparently a hot secondary market in gift cards, so large values and resale could take off.

- Likewise, stored value cards, subway cards, stamps. Subway cards are anonymous so you could resell them.

- Prepay bills. Send $10,000 to the gas company, electric company, phone company.

- Prepay rent or mortgage payments.

- Businesses: prepay suppliers and leases. Prepay wages, or at least pre-fund benefits that workers must stay employed to earn.

My brother Chris and I answer this argument in “However Low Interest Rates Might Go, the IRS Will Never Act Like a Bank.” The set of things that can create a zero lower bound can be narrowed down considerably by the two key principles we explain there:

- Giving a zero interest rate when market interest rates are in deep negative territory (say -5%) is a money-losing proposition. Private firms are unlikely to continue very long in providing such an above-market interest rate to individuals wanting to store money with them.

- Anything that can vary in price cannot create a zero lower bound: negative interest rates will either cause its price to go up enough that expected depreciation gives it a negative expected return, or potential price variation will make its return risky enough it is clear there is no risk-free arbitrage to be had. This rules out things such as gold or foreign assets from creating a zero lower bound, unless a credibly fixed exchange rate or an established price of gold is in play.

What is left? The only other category I can see are opportunities to lend to a government within the central bank’s currency zone at a fixed interest rate. But even there, there is another logical proviso on what can create a zero lower bound. I explain in “How to Keep a Zero Interest Rate on Reserves from Creating a Zero Lower Bound”:

[3.]… a zero interest rate that only applies to a limited quantity of funds does not create a zero lower bound. The reason that our current paper currency policy creates a zero lower bound is that under current policy banks can withdraw an unlimited quantity of paper currencyand redeposit it later on at par. By contrast, within-year prepayment of taxes is possible but practically limited to the amount of the tax liability. (Between tax years a typically nonzero interest rate based on the market yield of short-term U.S. obligations applies.)

Thus, other than paper currency:

- An unlimited option for banks to put funds in reserve accounts at a zero interest rate creates a zero lower bound. But if there is a ceiling of 101% of required reserves as I discuss in “How to Keep a Zero Interest Rate on Reserves from Creating a Zero Lower Bound,” an interest rate on reserves of zero does not create a zero lower bound.

- An unlimited option for depositors to save in a government-run bank (such as Japan’s postal savings) at a zero interest rate creates a zero lower bound. But an option to get a zero interest rate on a monthly balance of only up to 1000 euros per person (or an asset value of something like 4% of annual GDP for the eurozone as a whole), as I recommend in “How to Handle Worries about the Effect of Negative Interest Rates on Bank Profits with Two-Tiered Interest-on-Reserves Policies” does not create a zero lower bound.

- An unlimited option to prepay taxes in a way unlimited by any relationship to one’s actual tax liabilities, earn a zero interest rate and then get a huge tax refund creates a zero lower bound. But an option to prepay within the tax year capped at a reasonable estimate of one’s actual tax liabilities (all the current US tax law offers) does not create a zero lower bound.

IRS interest rates between tax years are set by the Secretary of the Treasury in line with market short-term rates, such as the Treasury bill rate. They are no stickier than the Secretary of the Treasury wants them to be. It is true that a sufficiently determined Secretary of the Treasury could probably thwart a Fed move to negative interest rates by offering convenient saving at a zero interest rate through the tax system. But I don’t think the Fed would be likely to go to deep negative rates in any case without some degree of tacit backing from the Executive Branch. (I do think that with the Executive Branch’s tacit backing, the Fed might go to deep negative rates despite complaints in Congress if it thought that was necessary for the economy.)

Finally, suppose I am wrong about the willingness of private firms to lose money by continuing to offer a zero interest rate when many market rates have gone substantially negative. In “Banking at the IRS,” John Cochrane argues that private interest rates are sticky at zero. There is still a limit to how much a firm can allow individuals to store at an above-market zero interest rate without going bankrupt, and in practice, the quantity limit of how much value a firm will allow people to store at a zero interest rate is much tighter than that.

Let’s get more concrete about the sheer magnitude of the task of finding zero interest ways of storing one’s money when the central bank is bidding up the price–and therefore down the interest rate–of Treasury bills as far as it can before investors sell over the whole stock of Treasury bills. To make the calculations easier, let me imagine that before going to negative rates, that a central bank has done enough quantitative easing that most of the national debt in private hands is in the form of short-term Treasury bills that have a negative rate. In that case, the net debt-to-GDP ratio (based on government debt in private hands) puts a floor on how much in funds private individuals will be trying to shift into zero interest rate opportunities. Actually, to this should be added the paper currency to GDP ratio too, since under my proposal, paper currency carries a negative rate of return because of its gradual depreciation against electronic money. (It is only because paper currency would have a negative rate of return under my proposed policy that the discussion in this post even arises.) Here are a few interesting net debt/GDP ratios rounded to the nearest full percent as of the latest update of the Wikipedia article “List of countries by public debt” in 2012. I doubt many of these numbers have gone down since then:

- Australia: 17%

- Austria: 51%

- Belgium: 106%

- Canada: 37%

- Denmark: 8%

- Finland: -51%

- France: 84%

- Germany: 57%

- Greece: 155%

- Ireland: 102%

- Israel: 70%

- Italy: 103%

- Japan: 134%

- Netherland: 32%

- Norway: -166%

- Portugal: 112%

- Spain: 72%

- Sweden: -18%

- Switzerland: 28%

- United Kingdom: 83%

- United States: 88%

Certainly, in the eurozone, Japan, the United Kingdom, the US and Canada, the task of finding zero interest rate opportunities for all the funds that start out in government debt is daunting. Countries like Norway that have a substantial sovereign wealth fund show that the amount of money the public holds in government bills and bonds–surely a positive number–can be larger than the government debt with assets netted out–in Norway’s case, a negative number. So the net debt to GDP ratios above are only the start of how much people might face a negative interest rate in that they are trying to escape.

The biggest single opportunity for getting a zero interest rate when rates in general are negative is typically tax system. I suspect that most countries have much less wiggle room for playing with the timing of tax payments than the US. For example, the rules for the timing of paying VAT taxes probably don’t have the same kind of wiggle room. And even in the US, the wiggle room on the timing of payments is probably much greater for households than for firms. In the US, tax revenue as a percentage of GDP is something like 27%. But shifting tax payments from being paid each month as the income comes in to being paid on January 1, say, only shifts that 27% forward by 6.5 months on average, since some of the payments are already early in the year. Or for those who pay quarterly, things might be shifted forward by 7.5 months. (7.5/12) * 27% is less than 17%. (This is composed of up to 27% of GDP at a zero interest rate at the beginning of the year, and much less at a zero interest rate toward the end of the year.)

That limit of 17% of annual GDP (averaged over the year) that can get a zero interest rate is far short of the 88% that individuals and firms in the US and abroad will want to find in zero US interest rates. Along the lines of “How to Handle Worries about the Effect of Negative Interest Rates on Bank Profits with Two-Tiered Interest-on-Reserves Policies,” throw in bank account assets amounting to 4% of annual GDP in individual bank accounts exempted from a negative interest rate supported by subsidies through the interest on reserves formula. (The effective subsidy needed is not 4% of GDP, but the absolute value of the interest rate times 4% of a year’s GDP, say |-4%| per year times 4% of yearly GDP, or .16% of GDP on a flow basis.) Beyond the bank accounts subsidized to have a zero interest rate, then throw in a generous several percent of annual GDP worth of prepayment opportunities that the private sector will allow, and still those now holding government debt will fall far short of finding enough zero interest opportunities to shift their liquid assets into. When I say that is generous, remember that the flow that can be prepaid needs to be multiplied by the length of time it can be prepaid to get the stock of wealth that can be shielded from zero interest rates. Other than prepayment of mortgages–which is already a big issue even at positive interest rates–most opportunities to prepay are limited to about 90 days, which is much lass than in the tax system.

Even with substantial opportunities to get a zero interest rate, if individuals and firms have liquid assets left over that can’t get a zero interest rate, then the key market rates can go into deep negative territory as the central bank bids up the price of Treasury bills so that, say it costs $10,100 to buy a promise from the Treasury of $10,000 three months from now: a -4% annual yield.

So far, central banks that have gone to negative interest rates have done so tentatively. Still, interesting adjustments are beginning to happen. Here is a passage from Tommy Stubbington’s December 8, 2015 Wall Street Journal article “Less Than Zero: Living With Negative Interest Rates”:

Danish companies pay taxes early to rid themselves of cash. At one small Swiss bank, customer deposits will shrink by an eighth of a percent a year.

But it isn’t all bad. Some Danes with floating-rate mortgages are discovering that their banks are paying them every month to borrow, instead of charging interest on their home loans. …

… other peculiar consequences are sprouting. In Denmark, thousands of homeowners have ended up with negative-interest mortgages. Instead of paying the bank principal plus interest each month, they pay principal minus interest.

“Hopefully, it’s a temporary phenomenon,” said Soren Holm, chief financial officer at Nykredit, Denmark’s biggest mortgage lender by volume. Mr. Holm said the administration of negative rates has gone smoothly, but he isn’t trumpeting the fact that some borrowers get paid. “We wouldn’t use it as a marketing tool,” he said.

Negative rates have cost Danish banks more than 1 billion kroner ($145 million) this year, according to a lobbying group for Denmark’s banking sector.

“It’s the banks that are paying for this,” said Erik Gadeberg, managing director for capital markets at Jyske Bank. If it worsens, Jyske might charge smaller corporate depositors, he said, then maybe ordinary customers. “One way or another, we would have to pass it on to the market,” Mr. Gadeberg said.

In Switzerland, one bank already has. In October, Alternative Bank Schweiz, a tiny lender, sent letters to customers with some bad news: They were going to be charged for keeping money in their accounts.

The Swiss central bank has a deposit rate of minus 0.75%, and Martin Rohner, chief executive of ABS, decided enough was enough. The costs were eating up the firm’s entire profit, he said. He set a rate of minus 0.125% on all accounts.

August Klatt: Is the NFL Trying to Hide Something by Injecting Bias into Head Injury Science?

Link to August Klatt’s Linked In homepage

I am pleased to host another student guest post, this time by August Klatt. This is the 2d student guest post this semester. You can see all the student guest posts from my “Monetary and Financial Theory” class at this link.

Behind the $100 million donated for brain research by the National Football League lies many question marks. Does NFL Commissioner, Roger Goodell honestly want to reveal the long-term effects of head injuries or is this all a publicity stunt?

There is no doubt that football is one of the largest causes of concussions.Head trauma has been observed to cause serious long-term brain damage and diseases such as Chronic Traumatic Encephalopathy (CTE). CTE was discovered by Neuropathologist, Dr. Bennet Omalu, who was recently played by Will Smith in the new movie Concussion. A movie that clearly explained the dangers of head trauma, was highly critical of the NFL, and showed that there is still a lot of research that still needs to be done.

Former NFL players, such as Junior Seau have unfortunately been the victims of CTE. Seau shot himself in 2012 and when his brain was examined it was determined that he had this disease.CTE can cause depression and aggressive behavior. It was probably concussions while playing football that caused Seau’s awful disease and eventually led to his death. The death of Seau and the movie Concussionhave brought brain research into the spotlight recently and have raised questions about the NFL.

As these concussion issues started to lead to critiques of the NFL, the league stepped up as the largest contributor of donations for brain research. This looks like the NFL is trying to help uncover the risks of concussions, but it might be a little more than that. The NFL has typically funded research projects with “league-friendly scientists.” Roger Goodell and the National Football League know that the public will continue to push for more research, so if it’s going to happen, it might as well be on their terms.

In an article on ESPN by Steve Fainaru and Mark Fainaru-Wada, the NFL agreed to co-sponsor a significant study in 2012 with the National Institute of Health. This study was designed to research the connection between football and long-term brain damage. Once the NIH awarded the study to Dr. Robert Stern, the NFL funding disappeared. Dr. Robert Stern is famously known for critiquing the National Football League and accusing them of covering up links between brain damage and football, which eventually led to a court settlement.

ESPN’s Outside the Lines did a report on how the NFL has used its power to influence concussion research. In an article also written by Steve Fainaru and Mark Fainaru-Wada, they discuss the results of this report by saying:

In at least six instances over the past year years, NFL-affiliated grants totaling several million dollars have gone to scientists of institutions directly connected to the league, the data shows. The NFL and its partners awarded nearly $4 million for projects tied to the co-chairman of its powerful Head, Neck and Spine Committee Dr. Richard Ellenbogen, including a $2.5 million concussions clinic affiliated with Ellenbogen and another top NFL advisor.

While the NFL has made a step in the right direction by pouring money into this research, their hands are too close to it all. I agree with the Wall Street Journal opinion article by Roger Pielke Jr. that the “NFL needs distance from its brain-injury funding.” If the NFL wants to ensure that their $100 million is going towards credible and useful research then they need to let the National Institute of Health allocate the money without any stipulations. This is the only way that we can maximize the social benefit of the brain research contributions.

With the NFL awarding concussion research to league-friendly scientists, any results that suggest football not having a negative effect on the brain are automatically discredited by many. The public has such a vested interest in brain injuries now that the true research is bound to get out. If the NFL has nothing to hide, then putting the funding in the hands of the NIH shouldn’t bother them. If they are trying to hide something and influence the research then they better stop now before they drown themselves in billions of dollars worth of lawsuits.

Ezra Klein Interviews Ben Bernanke about Miles Kimball’s Proposal to Eliminate the Zero Lower Bound

Photo of Miles telling Yang Liu and Ben Bernanke how good the hors d’oeuvres are and how to eliminate the zero lower bound when Ben Bernanke came to give a talk at the University of Michigan on January 14, 2013

In a December 15, 2015 episode of “The Weeds,” Ezra Klein asked Ben Bernanke about my proposal to eliminate the zero lower bound. See “Ezra interviews Ben Bernanke.” About the 34:50 mark the dialogue is as follows:

Ezra Klein: There is an idea out there, which is obviously politically unlikely. But I’ve always found it interesting as a thought experiment at the very least—and it is has been pushed by, among others, economist Miles Kimball. Which is, if you could have instead of the paper dollar being the store of value, sort of an electronic dollar, we could really move on somewhere to electronic money, then it would essentially be easy as a matter of technical, operational work to have negative interest rates as well as positive ones. Are you familiar with these proposals, and I’m curious what you think of them.

Ben Bernanke: Yeah, I think that something like that would work in the sense that it could help get interest rates negative, so it would give the Fed more ability to cut rates even when rates were started out at a very, very low level. But I–first of all it’s kind of Rube Goldberg in the sense that the simpler solution would just be to have reasonable fiscal policy, that—that acts at the appropriate time. And secondly, as you point out, I think that it’s not something that the American public would be too enthralled with. I think politically, it would be very, very difficult to get—get approval for that. So its not, you know—it’s not something that I see as high on the priority list, putting aside whatever it’s—whatever the theoretical costs and benefits might be, it doesn’t seem like something that politically is feasible anytime soon.

Miles: In response to Ezra’s description, let me clarify that what is important is for electronic money to provide the unit of account. There are many stores of value, but one main unit of account.

I have many reactions to what Ben Bernanke said:

- Ben Bernanke agrees with Peter Sands and Larry Summers that, from a technical point of view, what I propose could do the job.He says: “I think that something like that would work in the sense that it could help get interest rates negative, so it would give the Fed more ability to cut rates even when rates were started out at a very, very low level.”

- The details of the implementation I propose make it much more politically feasible than other modes of implementation. When I give a seminar to central bankers, they come in thinking it might be a nice idea in theory, but would never happen, and then go out of the seminar seeing that it can really be done. For example, my proposal is fully compatible with using the current paper notes. My more recent presentations–ever since I started presenting “18 Misconceptions about Eliminating the Zero Lower Bound”–have been even better at making this point.

- The political path I foresee is an international one, as discussed in “Breaking Through the Zero Lower Bound” (pdf) and “Negative Interest Rate Policy as Conventional Monetary Policy” (pdf). I do not think the US is likely to be the first nation to use deep negative interest rates, but there is hope that some other country will have pioneered the needed monetary policy tools by the time the US needs them.

- Many central banks can do what needs to be done to eliminate the zero lower bound without any new legislation. I am currently working with Peter Conti-Brown on an article for a law review discussing the legal situation in the US. We need to dig into the law a lot more, but so far, it looks as if the Fed might be able to do what needs to be done without any new legislation. In any case, one should not assume too quickly that new legislation is needed. The law gives the Fed a lot of discretion in monetary policy.

- I disagree with Ben about the aptness of discretionary fiscal policy for stabilizing the economy. In my view, the difficulty in using discretionary fiscal policy to handle deep recessions is not a random stroke of bad luck during this past recession, but something likely to obtain quite generally for basic political economy reasons: short-run fiscal policy simply has too much resonance with long-run fiscal policy, which in turn goes to the heart of the ways in which major parties differ in many advanced countries. Therefore, developing monetary policy tools powerful enough for central banks to stabilize economies even if fiscal authorities are not very helpful seems the height of wisdom.

On Ben Bernanke’s general claim that there are other tools available besides negative rates, here is an abridged version of the section in How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide about other possible tools for stimulating the economy:

Comparison of Negative Interest Rates to Other Tools for Stimulating the Economy

- Why Austerity Budgets Won’t Save Your Economy

- Monetary vs. Fiscal Policy: Expansionary Monetary Policy Does Not Raise the Budget Deficit

- Ben Bernanke: The Fed Does Less Monetary Stimulus Than It Thinks is Warranted Because It Is Afraid of the Side Effects of Unconventional Tools

- How and Why to Avoid Mixing Monetary Policy and Fiscal Policy

- Is the Bank of Japan Succeeding in Its Goal of Raising Inflation?

- Japan Should Be Trying Out a Next Generation Monetary Policy

- QE May or May Not Work for Japan; Deep Negative Interest Rates Are the Surefire Way for Japan to Escape Secular Stagnation

- Narayana Kocherlakota Advocates Negative Rates and Criticizes the Conduct of US Fiscal Policy

- If a Central Bank Cuts All of Its Interest Rates, Including the Paper Currency Interest Rate, Negative Interest Rates are a Much Fiercer Animal

- Helicopter Drops of Money are Not the Answer

- Higher Inflation Is Not the Answer

“Reporting on Japan’s Move to Negative Interest Rates” in German: “Mangelhafte Berichterstattung über Negativzinsen” oder “Negativzinsen Richtig Verstehen”

Link to the full magazine of which one page is shown above

I love to have posts translated into other languages. Werner Onken and Beate Bockting arranged a German translation of “Reporting on Japan’s Move to Negative Interest Rates” in Fairconomy, that you can see at this link. As a separately linked article, it goes by the title “Mangelhafte Berichterstattung über Negativzinsen.”

A Wonderful Ad for Nonsupernaturalism

via Joseph Kimball

(from an earlier Superbowl, not the latest one)

Laura Tyson on the Investment Accelerator →

Business investment depends on expected future demand and output growth, not on current returns or retained earnings. This “accelerator” theory of investment explains most – but not all – of the weakness of business investment in the developed economies since the 2008 financial crisis.

Capuchin Monkeys Reject Unequal Pay

via James Wells

With a Regulatory Regime That Freely Accomodates Housing Construction, Lower Interest Rates Drive Down Rents Instead of Driving Up the Price of Homes

In my travels to the central banks of many countries, when I dig into concerns about financial stability, I often find that the biggest financial stability worry associated with low or temporarily negative interest rates is about the effect of low interest rates on the price of houses in the capital city or other major cities. Let me analyze this issue.

The simplest case is when the anticipated real interest rate r is constant from now on and there are no tax complications. Suppose also that the home will last forever if appropriately maintained, with anticipated Rent and Maintenance constant from now on. Then the price P based on these anticipated values should be

P = (Rent - Maintenance) / r

If no additional construction is allowed, and the economy is fairly static even after the interest rate changes (say because of a changed desire for saving), Rent and Maintenance should stay close to the same, so Price should go up when r goes down.

But if construction is freely allowed within certain parameters–say along the lines I propose in “Density is Destiny,” which makes land costs small relative to the physical cost of building, than in the long run, the price of a home must equal the cost of constructing, say, the floor of the building corresponding to that home. With P a constant, it is useful to rearrange the equation above to

Rent = Maintenance +r P

Thus, for example,

If, in the long run, the real interest rate is a small positive number in relation to the standard construction price of a home, than rent should be a little above maintenance.

In the limit, as the real interest rates goes down toward zero, rent should just equal maintenance.

If, in the long run, the real interest rate is negative, then the equation seems to say that rent should be below maintenance. But the equation doesn’t really work when the long-run real interest rate is negative, since if rent were below maintenance, the home would be a burden rather than a benefit, and no one would pay anything for it. In other words, the price is equal to the cost of building a home as long as it is worth someone’s while to build one. But if rent were below maintenance in the long run, no one would build one. On the other side, note that the interest rate on an infinite-term bond–a consol–can never be negative in equilibrium. If I give you money and can never demand anything back other than interest, having a negative coupon payment where I pay you would mean I have only give you money and you never give me anything back. I won’t do it. So at a minimum, negative interest rates must either be temporary or include either some return of the principal within finite time, or an option to demand the principal back at some finite time.

If the interest rate is expected to move around, the same essential principles apply. For fixed rent and maintenance–corresponding in my simple example to a prohibition against new construction–any path of lower interest rates raises the present value of a home, so the price of a home goes up. For a fixed price of a home–corresponding in my simple example to a policy very favorable to new construction–almost any path of lower interest rates will lead to more construction and lower rents.

Update, May 11, 2021: The experience in Japan helps prove my point. In the May 7, 2021 Wall Street Journal article “The Global House Price Boom Could Haunt the Recovery From Covid-19,” Mike Bird writes:

There have been a small number of successes in controlling and preventing house price booms to note. They bear much closer examination for policy makers in the rest of the world.

Japan’s case is the most obvious. The country’s lack of zoning restrictions and rent controls are regularly credited with the country’s flat home prices, particularly in Tokyo where the total population is still increasing.

Do Negative Interest Rates Lead To Too Much Debt?

One common objection to low interest rates–and even more to negative interest rates–is that it will lead to too much debt. It occurred to me that this is looking at things only from the standpoint of the borrower’s desires. But the amount of debt is determined in a market equilibrium in which the lender’s desires are also part of the picture. A similar one-sided logic would be to claim that low interest rates encourage too little lending. But with little lending, there would also be little debt. So which is it? Do low interest rates lead to more debt (because borrowers want more debt) or less debt (because lenders want to give them less and so borrowers can’t borrow and end up less in debt)?

If the central bank does its job well (better than existing central banks have managed so far), the economy would be near the natural level of output most of the time. Think of that as approximately the same state as if the economy had perfectly flexible prices and monetary policy had no effect on anything real. At the natural level of output, the level of national debt has to do with taxing and spending policy, while the level of private debt has a lot to do with heterogeneity–how different people are from one another in the sense of a wealth-weighted variance of preferences.

Starting from that benchmark, a positive output gap might mean there are more good-looking projects for which there would be both demand and supply of loans. So low central bank interest rates might lead to more debt simply because the economy then boomed, while high central bank interest rates might lead to less debt because the economy contracted and their were few projects for which there was both supply and demand for lending.

In this discussion, I haven’t yet adequately distinguished between debt in the sense of fixed-income securities and equity finance. This distinction matters. To the extent debt causes problems for financial stability, it is almost always fixed-income securities that are the problem. The easiest way to reduce debt is to have tight leverage limits–or equivalently, high equity requirements–for banks and other financial firms, for individual mortgages (with mortgage reform such as Andy Caplin’s share appreciation mortgages) and for any other type of firm that has shown a high propensity toward threatened bankruptcy. Even student loans can easily be put on a more equity-like and less debt-like basis by having some of the payment stated as a percentage of income instead of as a fixed amount.

If policy is trying to push arrangements toward more equity and less debt, negative interest rates can be quite helpful, because they make safety look like a loss, which makes potential lenders more willing to put their funds into securities that look like equity.

A related concern is the concern that negative interest rates might encourage people to take on too much risk. But if the risk is funded by equity instead of debt, risk can be taken on without seriously raising the probability of bankruptcy. And as long as bankruptcy probabilities are low because the fraction of equity-funding is high, risk-taking seems to me like a good thing, not a bad thing.

Now I may be missing something here. If so, I would be interested to here what. One question I have is whether junk bonds are enough like equity that what I said about equity can be applied to them, or whether junk-bonds sometimes occur in industries where the deadweight loss from bankruptcy is so high that there is a lot of inefficiency to having junk-bond financing instead of equity financing. One would hope that junk bonds would mainly be an attractive funding vehicle in equilibrium in industries where the deadweight loss from bankruptcy was especially low.

Suparit Suwanik: Putting Paper Currency In Its Proper Place

Link to Suparit Suwanik’s Linked In homepage

I am delighted to be able to start another season of student guest posts with this guest post by Suparit Suwanik. The students in my “Monetary and Financial Theory” class are required to do 3 blog posts each weak during the semester. From among the best of these I choose some to be guest posts here. (You can see the class assignment and resource blog here, and links to student guest posts from previous semesters here.) I am impressed by Suparit’s level of understanding of what I have been proposing. Suparit’s post below is the 1st student guest post this semester:

Amid the growing popularity of the world’s newest monetary policy tool - negative interest rates, many newspapers, including the Wall Street Journal, are paying attention to the possibility of related changes in paper currency policy. The interesting editorial, “The Political War on Cash”, touches on how politicians and central bankers around the world are massively rallying to limit the use of cash, especially large-denomination bills. From Mario Draghi to Larry Summers, they are planning to get rid of the large notes, for example, €500 notes and $100 bills, which would mean it’s time to say goodbye to Benjamin Franklin. The author cites that “The real reason the war on cash is gearing up now is political: Politicians and central bankers fear that holders of currency could undermine their brave new monetary world of negative interest rates…” which suggests an unwarranted prejudice against negative interest rates. Also, he points out many reasons why paper currency shouldn’t be entirely eliminated (Yes, he’s going that far!). It’s such a pity he’s never taken a class with Prof. Miles Kimball of University of Michigan, a strong supporter of negative interest rate policy.

I take the liberty of crystallizing Kimball’ several posts, such as:

- How Subordinating Paper Currency to Electronic Money Can End Recessions and End Inflation,

- An Underappreciated Power of a Central Bank: Determining the Relative Prices between the Various Forms of Money Under Its Jurisdiction and

- The Costs and Benefits of Repealing the Zero Lower Bound… and Then Lowering the Long-Run Inflation Target

blended with my thoughts to counter argue the author’s reasons, point by point.

First, the Wall Street Journal editorial board argues that cash allows legitimate transactions to be executed quickly, without either party paying fees to a bank or credit-card processor. I somewhat agree that we need to pay fees to use credit cards, or electronic money, while we can use cash free of charge (cash earns zero interest rate). Yet, in the world of negative interest rates where the time-varying fee on cash deposits is additionally imposed, as Kimball suggested, cash, or paper currency has its value even less than electronic money. If you go buying something at a retail store, the shopkeeper will sell you at the higher price if you pay by the greenback than what it costs in electronic currency. That is, paying by cash even costs you more than (or equal to) paying by electronic currency, which includes fees to a bank or credit-card processor. This, in other words, means that the electronic currency is taking a role of “unit of account”, instead of the paper currency.

Second, the Wall Street Journal editorial board states that cash lets millions of low-income people participate in the economy without maintaining a bank account. This may be going too far since, according to Kimball, we will not entirely eliminate paper currency, at least, just yet. Subordinating paper money to electronic money as an economic yardstick is a big enough step for now; the question of whether to further demote paper currency can wait. We still keep the paper currency to function as “the medium of exchange” as it has always been doing, especially for low-income people that frequently use cash to buy relatively inexpensive necessity goods. Only one function of money, unit of account, will be given exclusively to the electronic currency.

Third, while there’s a chance of theft for cash, digital transactions are subject to hacking and computer theft. Again, this is going too far since, by the time when cash is going to be largely eliminated (but small bills are kept for those reasons mentioned above), the electronic system will have had large upgrades and enhanced security. Also, the security risk has long been presented, either you hold paper or electronic currency. So why are you so afraid as if it never existed?

Finally, cash is the currency of gray markets because high taxes and regulatory costs drive otherwise honest businesses off the books. The author warns that governments may need to reconsider since it might destroy businesses and leave millions of people unemployed. To my thought, this is a fallacy: why do we need to keep those businesses avoiding tax underground? Is it a duty of government to ignore those unlawful businesses just for the reason that they stimulate economy?

I agree that the government may reduce the role of paper currency that greatly compromises the privacy of transactions, but try weighing between pros and cons of going “electronic” as the new economic yardstick, in order to have effective policy in preventing the economy from the recession. I see no reason to deny it.

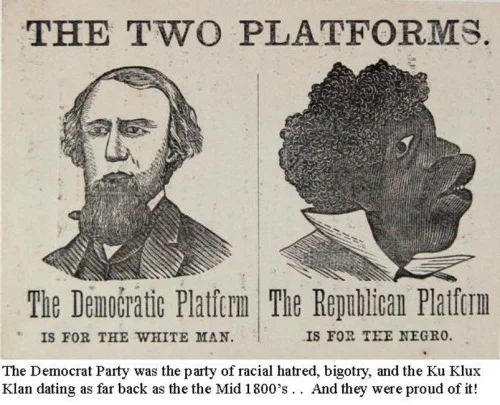

Democratic Injustice

We are at a moment when nationalism has a very visible advocate in US politics–a nationalism that not only privileges the interests of US citizens over the interests of non-citizens, but also often slips into thinking of many US citizens as if they weren’t US citizens, it is worth remembering the tendency of democracies toward the injustice of imposing the will of the majority on the minority.

For many of us, “democratic” has a very positive connotation–so much so, indeed, that those members of the Republican party who are frequently interviewed on TV have trained themselves to call the opposing party the “Democrat Party” instead of the “Democratic Party” to avoid having listeners be influence by the positive connotations of the word “democratic.” But “democratic” is a far cry from the beautiful word “just.” Justice requires, among other things, that no one is ever bossed around more than is truly needed to meet other genuine demands of justice and prudence. To realize that goal, explicit limits on the power of a democratic majority are necessary.

John Stuart Mill speaks eloquently of the experience we have gained about the dangers of unfettered democratic majorities in the 4th paragraph of the “Introductory” to On Liberty:

… in political and philosophical theories, as well as in persons, success discloses faults and infirmities which failure might have concealed from observation. The notion, that the people have no need to limit their power over themselves, might seem axiomatic, when popular government was a thing only dreamed about, or read of as having existed at some distant period of the past. Neither was that notion necessarily disturbed by such temporary aberrations as those of the French Revolution, the worst of which were the work of an usurping few, and which, in any case, belonged, not to the permanent working of popular institutions, but to a sudden and convulsive outbreak against monarchical and aristocratic despotism. In time, however, a democratic republic came to occupy a large portion of the earth’s surface, and made itself felt as one of the most powerful members of the community of nations; and elective and responsible government became subject to the observations and criticisms which wait upon a great existing fact. It was now perceived that such phrases as “self-government,” and “the power of the people over themselves,” do not express the true state of the case. The “people” who exercise the power are not always the same people with those over whom it is exercised; and the “self-government” spoken of is not the government of each by himself, but of each by all the rest. The will of the people, moreover, practically means the will of the most numerous or the most active part of the people; the majority, or those who succeed in making themselves accepted as the majority; the people, consequently, may desire to oppress a part of their number; and precautions are as much needed against this as against any other abuse of power. The limitation, therefore, of the power of government over individuals loses none of its importance when the holders of power are regularly accountable to the community, that is, to the strongest party therein. This view of things, recommending itself equally to the intelligence of thinkers and to the inclination of those important classes in European society to whose real or supposed interests democracy is adverse, has had no difficulty in establishing itself; and in political speculations “the tyranny of the majority” is now generally included among the evils against which society requires to be on its guard.

Let us not be too complacent in assuming that “democratic” outcomes are inherently just. It takes a lot more for a society to be just than simply having fair elections.

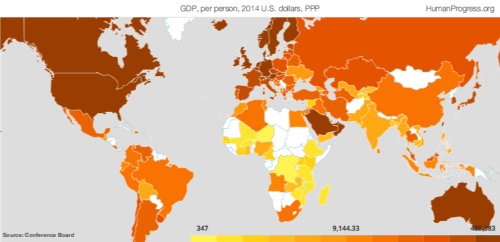

HumanProgress.org: GDP Per Person Over Time by Country

Interactive maps like this one are very revealing. HumanProgress.org has many others like it as well.

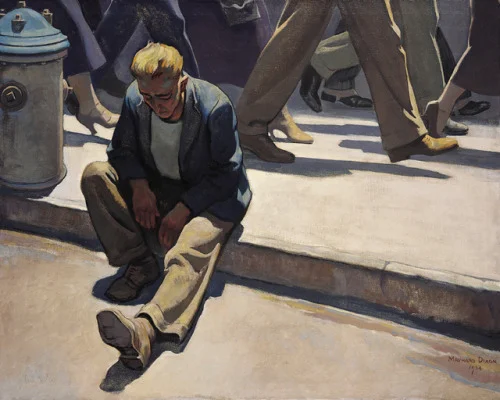

The Storm and the Battle Ahead

Decades of stagnating wages didn’t help, and the swift cultural changes brought on by technical change and globalization have occasioned many tough adjustments, but the timing and intensity of the political storm we see all around us owes a great deal to the Great Recession. The Great Recession in turn owes its depth and duration to not just a failure of financial stability policy, but to a monumental failure of monetary policy.

Many of the central bankers at the helm during the Great Recession acted heroically to make things better than they might have been–notably Ben Bernanke at the Fed, Mervyn King at the Bank of England and Mark Carney at the Bank of Canada–but even those heroic efforts fell far short of what common women and men had a right to expect from central bankers. The fault lies with the economics profession as a whole, which first did too little to insist on the high equity requirements that could have easily blunted or avoided the financial crisis that sparked the Great Recession, and second had not laid the intellectual groundwork to break through the zero lower bound in 2009 to stop the Great Recession in its tracks once it had begun.

Many artists documented the suffering in the Great Depression of the 1930′s. Seeing several of Maynard Dixon’s painting at the BYU art museum, including the one you see above, made me think of how that suffering was caused by that era’s monumental failure of monetary policy. What you and I are doing now to add to the tools available to central banks to fight recessions and escape the need for inflation is the least that people should expect of us in doing our duty. The hundreds of millions of people who depend on us should not suffer during the next recession because of any lack of diligence or courage on our part.

The people of the world, by and large, do not know exactly what went wrong to make the Great Recession as bad as it was. They do not know, by and large, what it will take to avoid a rerun of the Great Recession or the secular stagnation that Japan has suffered for the last 20+ years. Many of the people of the world may curse us for tools they don’t understand are the key to avoiding such dire outcomes. But they will curse economists in general–and central bankers in particular–much more if we fail to do our job of keeping the world economy on an even keel. Let us not shrink from the task before us, but press forward.

Many of you are already participants, in large and small ways, in the battle against the zero lower bound. This post is written in the first instance to honor you, to encourage you and to thank you for your efforts. For those readers newer to the idea that monetary policy can be reinvigorated by modifying traditional paper currency policy, take a look at “How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide.”

“There is a vitality, a life force, an energy, a quickening that is translated through you into action, and because there is only one of you in all of time, this expression is unique. And if you block it, it will never exist through any other medium and it will be lost. The world will not have it. It is not your business to determine how good it is nor how valuable nor how it compares with other expressions. It is your business to keep it yours clearly and directly, to keep the channel open. You do not even have to believe in yourself or your work.”

– Martha Graham, speaking to Agnes De Mille, as quoted in Martha: The Life and Work of Martha Graham. via Maria Popova, writing on Brain Pickings

Even Central Bankers Need Lessons on the Transmission Mechanism for Negative Interest Rates

Link to the Wikipedia article on Mark Carney

I have called Ben Bernanke a hero many times for his actions to stem the hemorrhaging of the US economy during the 2008 Financial Crisis and the ensuing Great Recession (in “Four More Years! The US Economy Needs a Third Term of Ben Bernanke,” in “Ben Bernanke on Trial” and in my presentations to central banks around the world). But for his actions as Governor of the Bank of Canada that insulated Canada from the worst of the Great Recession, and his work as Chairman of the G20′s financial stability board, Mark Carney is every bit as great a hero. Although for the sake of financial stability, it is worth desiring even higher equity requirements for banks, those equity requirements are probably significantly higher and the international financial system significantly more stable than it would be without Mark Carney’s leadership.

In addition to my assessment of Mark Carney as a hero, I have to confess myself a fan. Along with Haruhiko Kuroda, he tops my list of central bankers I would like to meet in person, but haven’t yet. And I wrote “Could the UK Be the First Country to Adopt Electronic Money?” thinking of Mark Carney’s remarkable career move from the Bank of Canada to head the Bank of England.

But I take issue with Mark Carney’s inadequate analysis of the transmission mechanism for negative interest rates in his recent speech “Redeeming an unforgiving world.” It is the sort of thing people are saying these days, but it is incomplete and misleading. One could easily come away with the idea that unless regular households face negative interest rates in their deposit accounts that negative interest rates only work through the exchange rate channel, which is zero-sum from a global point of view. What Mark Carney meant might be much more sensible: except for small household accounts, if Mark Carney’s point is simply that more pass-through of negative interest rates is better than less, I wholeheartedly agree. (Fortunately, experience with negative interest rates in Europe suggests that–with the exception of household accounts, large and small–there is a great deal of pass-through.) But in any case it is important to deal with what Mark Carney said and how it might be misconstrued. To show that I am not off-base to worry about such a construal, consider this from George Magnus in Prospect:

To their credit, policymakers did note that monetary policy alone was no longer enough to deal with the problems in the world economy. Mark Carney, Governor of the Bank of England, had earlier criticised countries pursuing Negative Interest Rate Policies, or NIRP, by arguing that where retail customers were protected from the effects, countries were essentially pursuing a covert form of currency depreciation.

Of course monetary policy is not enough to deal with all the problems of the world economy: I said as much in “Governments Can and Should Beat Bitcoin at Its Own Game”:

But make no mistake: Giving electronic money the role that undeserving paper money now holds will only tame the business cycle and end inflation. Fostering long-run economic growth, dealing with inequality, and establishing peace on a war-torn planet will remain just as challenging as they are now. But every time one set of problems is solved, it allows us to focus our attention more clearly on the remaining problems. It is time to step up to that next level.

Monetary policy cannot solve all of our problems. But monetary policy–and full-scale negative interest rate policy in particular–is the primary answer to the problem of insufficient aggregate demand. It is a bad thing when world leaders say or seem to say the opposite. As the title of Martin Sandbu’s excellent column on ft.com proclaims: “Central banks cannot pass the buck.”

Mark Carney’s Description of the Transmission Mechanism for Negative Interest Rates

Here is the key passage from Mark Carney’s speech:

Central bank innovation has now extended to negative rates, with around a quarter of global output produced in economies where policy rates are literally through the floor.

Conceptually the more that effective policy rates can be reduced below equilibrium rates, the better the prospects for demand to grow faster than potential supply, promoting global reflation.

However, it is critical that stimulus measures are structured to boost domestic demand, particularly from sectors of the economy with healthy balance sheets. There are limits to the extent to which negative rates can achieve this.

For example, banks might not pass negative policy rates fully through to their retail customers, shutting off the cash flow and credit channels and thereby limiting the boost to domestic demand.7 That is associated with a commonly expressed concern that negative rates reduce banks’ profitability.

To be clear, monetary policy is conducted to achieve price stability not for the benefit of bank shareholders.

Nonetheless, when negative rates are implemented in ways that insulate retail customers, shutting off the cash flow and other channels that mainly affect domestic demand, while allowing wholesale rates to adjust, their main effect is through the exchange rate channel.

From an individual country’s perspective this might be an attractive route to boost activity. But for the world as a whole, this export of excess saving and transfer of demand weakness elsewhere is ultimately a zero sum game. Moreover, to the extent it pushes greater savings onto the global markets, global short-term equilibrium rates would fall further, pulling the global economy closer to a liquidity trap. At the global zero bound, there is no free lunch.8

For monetary easing to work at a global level it cannot rely on simply moving scarce demand from one country to another. Instead policy needs to increase primarily domestic demand, with the exchange-rate channel more a side effect that accompanies any monetary policy action.

In any given country, a monetary expansion aimed at boosting domestic demand will tend to reduce effective interest rates relative to their equilibrium level, generating an excess of domestic investment over domestic saving that must be met with a capital inflow from abroad.

But viewed from overseas, the corresponding capital outflow will tend to raise the short-term equilibrium rate (Chart 12), giving conventional monetary policy overseas more traction.

In this way, the rising tide of global demand would raise all boats.

Why It is OK for Regular Households to Be Insulated from Negative Deposit Rates

In “How to Handle Worries about the Effect of Negative Interest Rates on Bank Profits with Two-Tiered Interest-on-Reserves Policies” I argue that it is not only OK for small deposits (say the first 1000 euros in average monthly balances per person) to be exempted by private banks from negative rates to the extent those banks choose to do so, but that this should be encouraged by an effective subsidy built into the central bank’s formula for interest on reserves. One reason this is OK is that most of the assets and liabilities in the economy are held by firms and a small share of the people, so there is plenty of transmission mechanism left if only large accounts and commercial accounts are subject to the negative interest rates. I do agree with Mark Carney that it is very helpful to encourage banks to pass along negative interest rates to large accounts and commercial accounts.

The kind of central bank subsidies I suggest in “How to Handle Worries about the Effect of Negative Interest Rates on Bank Profits with Two-Tiered Interest-on-Reserves Policies,” combined with the encouragement to pass along negative interest rates to the large accounts and commercial accounts can go a long way toward maintaining bank profitability.

Negative Interest Rates Can Do Their Work Even Outside of the Foreign Exchange Markets

Let me set aside the foreign exchange markets for a moment by imagining that interest rates are being cut by 1 percentage point by all the central banks in the world. In some countries this would be a cut to a lower positive interest rate. In other countries, it would be a cut to a negative interest rate or to a deeper negative interest rate, which for countries already at significant negative interest rates might call for lowering the paper currency interest rate as well. (See “If a Central Bank Cuts All of Its Interest Rates, Including the Paper Currency Interest Rate, Negative Interest Rates are a Much Fiercer Animal.”) Since all countries would be cutting their rates by 1 percentage point in tandem, there should be only modest effects on international capital flows and hence only modest effects on exchange rates and trade balances.

The effects of this interest rate cut would be quite similar for countries that were cutting their rates in the positive region and countries that cut to a negative rate. As I wrote in “Negative Interest Rate Policy as Conventional Monetary Policy”:

As far as I know, very few economists have objected to permanently raising the inflation rate as a way to deal with the zero lower bound on the basis that this would not, in fact, allow any extra monetary stimulus. The reason is the fact I started with: standard models say it is the real interest rate that matters. But if it is the real interest rate that matters, lowering the nominal interest rate without raising inflation will stimulate the economy through totally standard mechanisms. It is not necessary to have full agreement on exactly how a lower real interest rate stimulates the economy. For all of those who agree that interest rate policy matters, a cut in the nominal interest rate will have much the same effect as an increase in inflation with the nominal interest rate held fixed. So if an increase in inflation operates through conventional means, so does a cut into negative territory of the full set of nominal government interest rates – target rate, interest on reserves, lending rate, between- tax-year rate, postal savings rate and paper currency interest rate. In that sense, a negative interest rate policy is a conventional monetary policy if having a target inflation rate of 2 per cent or 4 per cent instead of a target inflation rate of zero is a conventional monetary policy.

With a global cut in interest rates by 1 percentage point, different countries are getting to a low real interest rate in different ways–some in part by having had higher inflation to begin with, some by negative nominal interest rates–but the effects are similar.

But negative interest rates seem new enough, that it is worthwhile to review the wide range of transmission mechanisms by which lower interest rates increase aggregate demand. Here is the basic story: In any nook or cranny of the economy where interest rates fall, whether in the positive or negative region, those lower interest rates create more aggregate demand by a substitution effect on both the borrower and lender, while other than any expansion of the economy overall, wealth effects that can be large for individual economic actors largely cancel out in the aggregate.

The Principle of Countervailing Wealth Effects: It is easy to forget about some of the wealth effects. Applying the general principle that all the wealth effects cancel–other than overall expansion of the economy and differences in the marginal propensity to consume across economic actors can help in making sure one hasn’t missed a wealth effect, much as double-entry accounting helps in making sure one doesn’t miss something. An example of a particularly large wealth effect that is easy to miss is that a fall in interest rates raises the present discounted value of household labor income. The other principle that helps to avoid missing a wealth effect is to remember that there is always another side to every borrowing-lending relationship. If the economic actor on one side of the borrowing-lending relationship gets a negative hit to effective wealth, the economic actor on the other side will get a positive boost to effective wealth–again with the exception of the overall expansion of the economy.

The Effect of Redistributions: Redistributions from economic actors with a high propensity to consume to economic actors with a low propensity to consume might reduce the aggregate demand effect, but as an analysis like the one that Adrien Auclert does in “Monetary Policy and the Redistribution Channel.” shows that (a) the effects from such redistributions are modest (though definitely big enough to be worthy of Adrien’s effort at studying them) and (b) in the aggregate they tend to go in the same direction as the substitution effect. For understandable reasons, the modest overall size of the redistribution effects is not highlighted in the abstract but the fact that these redistributions act in the same direction as the substitution effect is. Note the word “amplify”:

This paper evaluates the role of redistribution in the transmission mechanism of monetary policy to consumption. Three channels affect aggregate spending when winners and losers have different marginal propensities to consume: an earnings heterogeneity channel from unequal income gains, a Fisher channel from unexpected inflation, and an interest rate exposure channel from real interest rate changes. Using a sufficient statistics approach, I show that the latter is plausibly as large as the intertemporal substitution channel in Italian and in U.S. data. A calibrated model reveals that this channel is particularly potent when asset maturities are short, and that the other two redistributive channels can also amplify the effects of monetary policy.

My proposals would have only a limited effect on redistribution channels. I can think of only two:

- Effective subsidies through the interest-on-reserves formula to encourage banks to exempt small accounts from negative interest rates tend to make interest rate cuts more favorable for spending by avoiding taking funds from households likely to have a high marginal propensity to consume.

- People using paper currency for tax evasion may well have a high marginal propensity to consume, but the more serious criminals who hold most of the rest of paper currency probably have a low marginal propensity to consume; laundering money into legitimate-enough businesses that it is safe to spend the money takes time, so for the most financially successful criminals consumption must often be deferred. (Think of the trouble the protagonists in “Breaking Bad” had in spending their money in the present without calling too much attention to themselves.) Lowering the paper currency interest rate is mostly a transfer from criminals of these two types to the central bank, where it either adds to central bank independence or is sent on to the remainder of the government. And in most countries, the rest of the government probably has a fairly high propensity to consume funds transferred to it from the central bank. (Indeed, in the US, there is an increasing and dangerous trend, not toward demanding the Fed generate more seignorage revenue, but toward demanding that the Fed hand over seignorage revenues it makes in the normal course of its businesses more quickly precisely because it is a way to spend more money without running afoul of anti-deficit rules.)

Why Wealth Effects Would Be Zero With a Representative Household: It is worth clarifying why the wealth effects from interest rate changes would have to be zero if everyone were identical. In aggregate, the material balance condition ensures that flow of payments from human and physical capital have not only the same present value but the same time path and stochastic pattern as consumption. Thus–apart from any expansion of the production of the economy as a whole as a result of the change in monetary policy–any effect of interest rate changes on the present value of society’s assets overall is cancelled out by the effect of interest rate changes on the present value of the planned path and pattern of consumption. Of course, what is actually done will be affected by the change in interest rates, but the envelope theorem says that the wealth effects can be calculated based on flow of payments and consumption flows that were planned initially.

Examples of Channels of Transmission of the Effects of Interest Rate Cuts to Aggregate Demand

Interest rates show up in many parts of the economy. Generally, interest rates move up and down together. Those where there is more risk of default or where money is locked up for longer periods of time tend to have a higher average level, so a move to negative short-term safe rates is likely to mean lower, but still positive rates for most consumer loans and bank loans, for example. It is worth taking a look at how, in each borrower-lender relationship, lower interest rates tend to stimulate aggregate demand overall. It is also good to notice how a loan done in a regular bank office is only a small share of all borrower-lender relationships.

Mortgages: Houses are easier to buy and to build when interest rates are lower. The effective wealth of those who own mortgages tends to go down when interest rates fall, especially when people use a prepayment option to refinance at a lower interest rate, but those who need to pay the mortgage get a corresponding improvement in their financial situation that enables them to spend more. Those who need to pay the mortgage typically have a higher propensity to consume.

Car Loans: Cars are easier to buy when interest rates are lower. This stimulates aggregate demand, and is mostly a substitution effect. Car buyers and car dealers benefit from lower interest rates. Their increased effective wealth makes up for the reduction in effective wealth of those who own securities backed by car loans who hope to roll over their existing loans into more car loans. Apart from the effects of that loss in effective wealth, those looking to roll over car loans they hold into more car loans have an incentive to shift the spending of what resources they have left toward the present over the future. That substitution effect also contributes to aggregate demand.

Venture Capital: It is easier and cheaper to get money for a startup when interest rates are low. This has a substitution effect toward more burn to write new software or develop a new medical treatment. There are wealth effects favoring those who have ideas over those who have a pile of money to invest. Those who have ideas tend to have a higher propensity to spend on making their ideas a reality (not consumption spending, but spending nevertheless) than the propensity of those with the pile of money to invest to spend on their own.

Commercial Paper: Those whose bank accounts would exceed the limit for being shielded from negative interest rates need to put their money somewhere. For large amounts of money, paper currency is not that attractive to begin with, and can be kept from being too attractive by keeping the paper currency interest rate equal to the central bank’s target rate (say the federal funds rate or a repo rate). So those who want to hold liquid wealth are still likely to want to have some version of money market funds, even when they have a negative interest rate. Or it may be that a new type of fund would arise serving the same function. Lower interest rates make it less costly for businesses to borrow in the commercial paper market and so make it easier for those businesses to make it from one month to the next without running out of funds. These businesses may even feel they can take a somewhat bigger risk in the direction of expansions. Those with part of their pile of funds invested in the commercial paper market suffer a loss in effective wealth, but that is made up for by the increase in effective wealth of those borrowing in the commercial paper market. Leaving aside those wealth effects, those with their funds invested in the commercial paper market have a bit of a substitution effect in favor of consuming more.

Firms with Cash Hoards: Farthest from needing any bank loan are companies that already have large liquid asset hoards that under current interest rates, they see as earning a better risk adjusted returns sitting and earning interest than if invested in a new factory, new machinery, or a new business venture. When interest rates go down, these firms will begin to pay a heavy price for simply earning interest with a liquid asset hoard, and those within the company who want to champion a new business venture will meet with more success in internal corporate deliberations. This is particularly valuable for the economy if firms were applying too high a hurdle rate for proposed projects even at the old higher interest rate as Clay Christensen and Derek van Bever argue in their Harvard Business Review article “The Capitalist’s Dilemma.” In this context, negative interest rates might help greatly in getting not only the CFO but also the production and sales side of the firm to realize that interest rates are low, and what that should mean for business decisions.

Governments and Treasury Bill Holders: Those who like to roll over their wealth in the form of short-term Treasury Bills are likely to be especially unhappy about low interest rates. But their loss is the government’s gain. And since lower interest rates on Treasury Bills show up as a reduction in conventional measures of the government budget deficit, this money is especially likely to be spent by the government. So the redistribution in this case tends to lead toward more aggregate demand.

Many people have been frustrated that the substitution effect for government investment is so low. Most governments seem to pay too little attention to interest rates in deciding whether an investment project such as refurbishing roads and bridges is a good idea or not. But it is unlikely that the logic that low interest rates make government investment projects a better idea will forever fall on deaf ears in every nation in which interest rates fall.

Governments and Holders of Long-Term Government Bonds: It may well be that negative interest rates in most countries are preceded by quantitative easing that shifts government financing decisively toward Treasury bills. But there are likely to be some long-term government bonds left. In this case, there is much less of a redistribution between the government and the bond-holders. The committed payments stay the same for some time. The market value of the long-term bonds will change, but the present discounted value of the tax revenues slated to be used to make the payments on those bonds will change in a similar way. For the taxpayers, that change in the present value of the tax payments is in turn cancelled out to an important extent by the change in the present value of the income out of which those tax payments will be made.

With less redistribution, it makes sense to focus on the substitution effect even more than in the other examples above. As mentioned above, the substitution effect for the government may be low (much lower than it should be), but the holders of the long-term bonds have reason to shift their consumption forward in time.

Central Bank Lending: Eric Lonergan is right to emphasize in his post “There is a lot more the ECB can do” the value of central banks lowering the central bank lending rate (such as the discount rate in the United States) as part of a negative interest rate policy. As Martin Sandbu points out in “Central bankers’ feigned impotence” on ft.com, this needs to be done along with the central bank lowering the other interest rates it controls–otherwise private banks can borrow from the central bank and then park the money at a higher interest rate in the repo market or their reserve accounts after enough reshuffling to provide a bit of a fig leaf to pretend to hide what they are doing. Note here that it is the rate on extra reserves that needs to be in line with the lending rate. As I discuss in “How to Handle Worries about the Effect of Negative Interest Rates on Bank Profits with Two-Tiered Interest-on-Reserves Policies,” an effective subsidy by having a higher rate on inframarginal reserves is actually helpful.

If the central bank lending rate is in line with the target rate and interest on reserves, any redistribution is between savers and those banks borrowing from the central bank, with the central bank only a conduit and not itself subject to much of a wealth effect. But the positive wealth effect for banks is particularly important, since it helps preserve the bank capital needed for financial stability (hopefully in conjunction with a high capital conservation buffer that avoids the dissipation of scarce bank capital into dividends). And as in any other borrowing and lending relationship a lower central bank lending rate will have some substitution effect in favor of more spending–in this case through a certain amount of extra lending by the private banks that borrow from the central bank.

Returning to the Effects of Interest Rate Cuts on International Capital Flows and Exchange Rates

I hope the examples above show that the aggregate demand effects from lower interest rates–including negative interest rates–do not depend solely on international capital flows. It should be mentioned that even if all the nations in the world cut interest rates, there would be some interesting international effects. For example, China is a large holder of Treasury bills. If interest rates were to fall, there would be an important redistribution away from China toward the US. But let me now leave that aside.

The international effects Mark Carney is focusing on come from one country cutting its interest rates more than another. This leads to flows of funds from the now lower rate country toward other countries that have not cut their rates, as those funds seek a good return. As I discuss in “International Finance: A Primer,” the fact that foreign assets are purchased directly or indirectly by domestic currency then makes the rest of the world awash in domestic currency–more than the rest of the world outside the domestic currency zone wants. Exchange rates adjust until the domestic currency makes it way back to the domestic currency zone–primarily to pay for an increase in net exports.

Given the fact that negative interest rates would work for the whole world and so are not zero-sum, the fact that the early adopters get an extra kick from higher net exports is a feature, not a bug. As I argued in “Could the UK Be the First Country to Adopt Electronic Money?” and in my presentation “18 Misconceptions about Eliminating the Zero Lower Bound,” these international effects are likely to hasten the spread of negative interest rates as part of the monetary policy toolkit.

International effects can indeed be central for a small open economy such as Switzerland, Sweden or Denmark, and substantial even for an economy as large as the eurozone economy. And if a central bank gets enough extra aggregate demand quickly from international effects, it is unlikely to continue cutting interest rates far enough to see much action from the other channels. But if other central banks cut interest rates too in accordance with what their own economies need, then the central banks that started the round are more likely to find they need to cut interest rates far enough for the other channels to kick in in a big way.

When people ask about how effective negative interest rates are at stimulating aggregate demand, I always emphasize that interest rate cuts–in either the positive or negative region–should be judged by how much they do per basis point. One should not expect a 10 basis point (.1%) cut to have a huge effect simply because it is in the negative region. For those countries that choose as a matter of policy to keep their effective lower bound on interest rates by keeping the paper currency interest rate at zero, there may not be enough basis points to cut to have a big effect on aggregate demand. But for any central bank willing to go off the paper standard, there is no limit to how low interest rates can go other than the danger of overheating the economy with too strong an economic recovery. If starting from current conditions, any country can maintain interest rates at -7% or lower for two years without overheating its economy, then I am wrong about the power of negative interest rates. But in fact, I think it will not take that much. -2% would do a great deal of good for the eurozone or Japan, and -4% for a year and a half would probably be enough to do the trick of providing more than enough aggregate demand.

International effects do matter; such a salutary rate cut by the eurozone and Japan would probably mean the US and the UK would need to go to milder negative interest rates in order to stay on track itself. But if the US and UK did so, such rate cuts in the eurozone, Japan and the United States and the United Kingdom would bring about a big expansion of aggregate demand for the whole world.

On the transmission mechanism for negative interest rates, also see “On the Need for Large Movements in Interest Rates to Stabilize the Economy with Monetary Policy”

For links to everything I have written about negative interest rates, see “How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide.”

Inequality Is About the Poor, Not About the Rich

{kind=link}

As an initiative of the “Wicked Problems Collaborative,” Chris Oesterreich put together the work of contributors for What Do We Do About Inequality? The book is now out. We would love to get some more reviews up on Amazon.

I agreed to contribute a chapter to this effort on the condition that I could post it here on my blog, too. Here it is, slightly re-edited:

One of the most basic ways to think about why inequality matters is to use the intuition that a dollar means more to a family that is desperately poor than to a family that is astoundingly rich. In the survey behind the University of Michigan’s Index of Consumer Sentiment, 90% of respondents agreed that “one thousand dollars is worth more to a poor family than to a rich family.” [1] Even more tellingly, 74% said that $1000 to a family at their own level of income would “make a bigger difference” than $4000 to a family at twice their level of income. That is, 74% of those surveyed agreed that doubling a family’s standard of living cuts the value of an extra dollar by a factor of at least 4.

The belief that the significance of a dollar declines with income even trumps favoritism toward people at one’s own income level: 66% of respondents agreed that $1000 to a family at half their level of income would “make a bigger difference” than $4000 to a family at their own level of income. That is, close to a 2/3 majority of everyone agrees that cutting income by a factor of two below their own level multiplies the value of an extra dollar by a factor of 4.

In this essay, I want to pursue the logical consequences of the idea that doubling income cuts the value of an extra dollar by at least a factor of four, while cutting income in half multiplies the value of an extra dollar by a least a factor of 4. If one accepts this idea, a little arithmetic then goes a long way toward clarifying issues of inequality. Extending this idea throughout the full range of income [2] yields something like the inverse square law for gravity, only a bit more dramatic: just as being ten times as far away from the Sun reduces the force of the Sun’s gravity by a factor of 100, being ten times richer reduces the value of an extra dollar by a factor of at least 100. And just as being ten times closer to the Sun increases the force of the Sun’s gravity by a factor of 100, being ten times poorer increases the value of an extra dollar by a factor of at least 100.

Thus, quantifying the idea that a dollar means more to a poor family than to a rich family shows that as far as financial well-being is concerned, inequality is about the poor, not about the rich. This is an important idea because a large share of the popular discussion about inequality focuses on the rich. Relative to being in the hands of a middle-income family, then, dollars in the hands of the ultra-rich are merely wasted, while dollars in the hands of the poor are supercharged in their potency for making lives better.