Meet the Fed's New Intellectual Powerhouse

Here is a link to my 47th column on Quartz: “Meet the Fed’s new intellectual powerhouse.”

I have two related columns not directly linked in this piece: “Monetary Policy and Financial Stability” and my discussion of Janet Yellen’s views: “Janet Yellen is Hardly a Dove: She Knows the US Economy Needs Some Unemployment.”

What I say in the column about how a low elasticity of intertemporal substitution affects how the Fed should respond to risk premia is informed by the discussion I gave of a paper of Mike Woodford and Vasco Curdia at a Bank of Japan conference (which I mentioned and linked to here.) Claudia Sahm, Matthew Shapiro and I are working on literature review of empirical work on the elasticity of intertemporal substitution for our paper on that topic. I will have more to say on that in the future.

Update: I wrote this column (which is about much more than Jeremy Stein himself) just in time. On April 3, 2014, Jeremy Stein announced he was resigning from the Fed. But we might see him again in the future in high government office.

Nobubble Nobel. By Marcia

As usual, econlolcats indicate good things coming. After a long hiatus, I will have a new Quartz column, “Meet the Fed’s New Intellectual Powerhouse.” (All but the word “meet” was my own original working title.)

Also, don’t miss my column about Bob Shiller:

Get Real: Robert Shiller’s Nobel Should Help the World Improve Imperfect Financial Markets

Thomas Jefferson and Religious Freedom

In his book Revolutionaries: A New History of the Invention of America(p. 307), Jack Rakove writes:

As he later explained in Notes on the State of Virginia, Jefferson had further reasons for making historical literacy the foundation of a common education. Rather than “putting the Bible and Testament into the hands of the children, at an age when their judgments are not sufficiently matured for religious enquiries, their memories may here be stored with the most useful facts from Grecian, Roman, European and American history.” … the kinds of historical facts that Jefferson deemed useful and his ideas of education carry over into the subject of bill 82, the bill for religious freedom. Though its formal purpose was to disestablish the Anglican Church, its deeper animus was to free individuals from any obligation to adopt religious views they found unpersuasive. In Jefferson’s view, all religious belief was finally a matter of individual opinion. The history of religious establishments was an unrelenting story of corrupting alliances between churchmen and rulers, abusing their power to impose their opinions and modes of thinking on others. This too was a form of tyranny, as inimical to liberty as anything else the Stuarts and other execrable autocrats had attempted. For Jefferson as for Locke, religion was not a matter of children inheriting the faith of parents. It was instead a subject of inquiry, and no one could simply adopt another’s convictions. The point of reading history first, scripture later, was to empower individuals to judge the claims of all religions by teaching them that much of what passed for orthodoxy in other times and places depended on the impure alliance of church and state.

See also “The Importance of the Next Generation: Thomas Jefferson Grokked It.”

Haozhao Zhang: The US Should Counter Russia's Natural Gas Weapon With Its Own

Image from the New York Daily News article “Vladimir Putin approves draft bill for annexation of Crimea as Russia, slams U.S. opposition.”

Haozhao Zhang is a student in my “Monetary and Financial Theory” class at the University of Michigan. I very much liked this post he did for the internal class blog. I asked him if I could make it a guest post here:

The current conflict in Ukraine is attracting a lot attention. Weeks ago, in order to against the counter force from EU countries, Mr. Putin played his trump card: raise the natural gas price in Ukraine. As a big country rich in natural resources–especially energy–Russia can use its control over the natural gas piped into Europe from Russia as a strategic weapon in this game.

The West has threatened to sanction Russia for moving to annex Crimea. But more than 30% of gas in EU is provided by Russia, so the credibility of those threats is in doubt. Leading countries in the EU such as the UK and Germany are faced with such a concern: the graph below from NYT can shows that major buyers of the Gazprom – Russia’s largest state-owned natural gas company.

Note the positions of Germany and Britain on the list. Actually according to this article in WSJ, Six countries in Europe import 100% of their gas from Russia, and an additional seven rely on it for at least half. It is beyond doubt that Russia has its considerable influence on the attitudes of the EU countries on this affair. U.K. Foreign Secretary William Hague said European nations may need to “recast their approach” to Russian energy purchases if the crisis isn’t resolved.

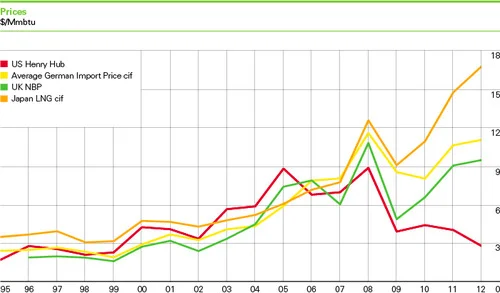

Also reported in WSJ, Obama’s government is taking measures to curb the Russia’s stranglehold over EU’s natural gas supply. US is currently one of the biggest natural gas production nations in the world due to one of its most advancing tech in this field: fracking. The strategy is to increase natural gas exports to the EU from the US, reducing the EU’s dependence on Russian gas. Compared to Russia, US has a big initial cost advantage that can help balance out transportation costs. As the graph from BP’s official site showed below, the natural gas price has kept falling over recent years in North America. The price in US is far lower than that of Asia and Europe.

In this strategy for the US, big oil and gas production firms like ExxonMobil benefit a lot from it, while environmentalists and small manufacturing companies strongly oppose such a claim. From a geopolitical point of view, this strategy seems unstoppable.

There are several reasons why US has restricted oil and natural gas exports in the past:

- Exporting more natural gas will increase the price of it in the US. Currently the natural gas price in US is only about 1/5 of that in Japan, which gives an advantage to US manufacturing industries that rely heavily on gas as raw material. More exports would mean less gas available in US, and the price would likely rise.

- Environmentalists are concerned about fracking.

- Fear of running out: in the past, with less advanced technology the available gas reserves seemed limited. People were afraid of a natural gas shortage later on if it was exported now.

However, the current situation is dramatically different. Here is why it is now a good time for the US to export natural gas:

- There is a boom in natural gas reserves, thanks to the new technology of “fracking.“

- Increasing the domestic gas price now looks like a good thing. Because of the increase in gas reserves, natural gas producing firms are complaining. Exports would now raise the price and benefit those firms without making the prices seem too high to consumers, compared to what they were used to in the past.

- Exporting US natural gas would curb Russia’s power over the EU. The political pressure in the Ukraine will be the main push behind increasing natural gas exports from the US.

Overall, the US strategy is good news, because it can help establish a global natural gas market, and encourage the use of relatively clean, low-carbon natural gas.

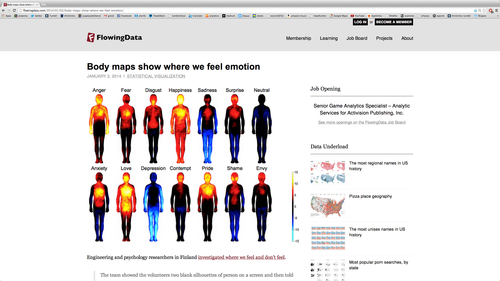

flowingdata.com

My top-notch chiropractor Mark Sakalauskas strongly recommended the website flowingdata.com. I think it will be of interest to many of you. Of recent posts on flowingdata.com I particularly liked the post linked above about where we feel emotion bodily.

On Happiness

This is the audio for a discussion about happiness by three of the best researchers and thinkers on happiness in the world: Justin Wolfers, Matthew Adler and my coauthor Ori Heffetz. (It was for a radio broadcast that never aired. Simon Tulett is the interviewer.) It makes a wonderful addition to my sub-blog on “Happiness.” Thanks to the participants for making this public–especially to Ori, who arranged to post it on his personal website.

“Folks, we’re talking about real policies that can make or break millions of lives. If you let your ego dictate your position on, say, monetary policy, rather than do your best to get it right, you’re doing something truly vile.”

John Stuart Mill: Different Strokes for Different Folks

Preference heterogeneity–different people wanting different things–has been a major theme in my research. In On Liberty, Chapter III: “Of Individuality, as One of the Elements of Well-Being,” paragraph 14, John Stuart Mill emphasizes the benefits for people’s welfare of letting them pursue their own desires, even if some of those desires are hard for us to understand:

I have said that it is important to give the freest scope possible to uncustomary things, in order that it may in time appear which of these are fit to be converted into customs. But independence of action, and disregard of custom, are not solely deserving of encouragement for the chance they afford that better modes of action, and customs more worthy of general adoption, may be struck out; nor is it only persons of decided mental superiority who have a just claim to carry on their lives in their own way. There is no reason that all human existence should be constructed on some one or some small number of patterns. If a person possesses any tolerable amount of common sense and experience, his own mode of laying out his existence is the best, not because it is the best in itself, but because it is his own mode. Human beings are not like sheep; and even sheep are not undistinguishably alike. A man cannot get a coat or a pair of boots to fit him, unless they are either made to his measure, or he has a whole warehouseful to choose from: and is it easier to fit him with a life than with a coat, or are human beings more like one another in their whole physical and spiritual conformation than in the shape of their feet? If it were only that people have diversities of taste, that is reason enough for not attempting to shape them all after one model. But different persons also require different conditions for their spiritual development; and can no more exist healthily in the same moral, than all the variety of plants can in the same physical, atmosphere and climate. The same things which are helps to one person towards the cultivation of his higher nature, are hindrances to another. The same mode of life is a healthy excitement to one, keeping all his faculties of action and enjoyment in their best order, while to another it is a distracting burthen, which suspends or crushes all internal life. Such are the differences among human beings in their sources of pleasure, their susceptibilities of pain, and the operation on them of different physical and moral agencies, that unless there is a corresponding diversity in their modes of life, they neither obtain their fair share of happiness, nor grow up to the mental, moral, and aesthetic stature of which their nature is capable. Why then should tolerance, as far as the public sentiment is concerned, extend only to tastes and modes of life which extort acquiescence by the multitude of their adherents? Nowhere (except in some monastic institutions) is diversity of taste entirely unrecognised; a person may, without blame, either like or dislike rowing, or smoking, or music, or athletic exercises, or chess, or cards, or study, because both those who like each of these things, and those who dislike them, are too numerous to be put down. But the man, and still more the woman, who can be accused either of doing “what nobody does,” or of not doing “what everybody does,” is the subject of as much depreciatory remark as if he or she had committed some grave moral delinquency. Persons require to possess a title, or some other badge of rank, or of the consideration of people of rank, to be able to indulge somewhat in the luxury of doing as they like without detriment to their estimation. To indulge somewhat, I repeat: for whoever allow themselves much of that indulgence, incur the risk of something worse than disparaging speeches—they are in peril of a commission de lunatico, and of having their property taken from them and given to their relations.

Jessica Hammer: Venezuela's Deadly Struggle

Jessica Hammer is a student in my "Monetary and Financial Theory” class at the University of Michigan. Students in the class write three blog posts a week for an internal class blog. Of the ones they select as their own best work, I have been choosing a few to publish as guest posts on supplysideliberal.com. This is Jessica’s second appearance here. Her previous guest post is “Jessica Hammer: The World Poverty Situation is Better Than You Think.” This post about Venezuela is a grim but powerful complement to Ezequiel Tortorelli’s guest post, “The Trouble with Argentina.” Here is what Jessica has to say about Venezuela:

When someone hears about Venezuela, I suspect the first thing most people think of is oil. Of course, this is due to the fact that this country is an OPEC member and exports around 25 million barrels of oil to the United States each month. Venezuela has one of the most abundant oil sources in the world but, unfortunately, it is being wasted. Perhaps you remember ex-President Hugo Chavez, and his passing in recent years. Many hoped the tyrannical government would disappear along with him, but the power of “chavismo” (the support for Chavez’s socialist reforms) prevailed. But the current president (the used-to-be bus driver who received no college education and is bluntly incompetent) , Nicolas Maduro, is slowly losing control of the country – or so they hope. The world knows little about the horrid situation in Venezuela, and how this potentially-wealthy nation is destroying itself.

Caracas, the capital, is currently (and has been for a while) the world’s deadliest city. Not Baghdad or Mogadishu. Mexico is known for its drug-related violence, but its murder rate is well below Venezuela’s rate of 73 per 100,000 citizens. Caracas, however, experienced a soaring rate of more than 200 per 100,000 in 2012 (and 2013 was even higher). To put this into perspective, Venezuela’s murder rate is higher than the death rates of the US and the 27 countries of the EU combined. Violence is so predominant, that people live in constant fear of going outside. Most wealthy people have to travel with bodyguards in order to avoid kidnappers. I personally know a lot of Venezuelans, and they all know of someone who has been murdered – either friends, family, or friends of friends. Most cases like these are a result of robberies. But gun fights are common to establish property rights, personal disputes, or drug-related problems. And the problem isn’t only the fact that violence is so widespread; nearly 90% of murders go unpunished. The police are so corrupt that they are often the ones involved in murders.

As if this weren’t enough to put up with, Venezuelans face daily shortages of basic goods. The most common ones include toilet paper, flour, sugar, cooking oil, and chicken. Not only are there rations on available goods, but these goods are not readily available. Producers point to the price controls and the limitations on foreign currency, which limit the availability of resources needed for production. Also, there are viable claims that 30 billion dollars were robbed from Cadivi (the government body which administered currency exchange) by the government elite. This is seen as the cause for the country’s current shortage problems.

Additionally, inflation is among the highest in the world at 56%. Maduro eliminated the Cadivi program last year, which Venezuelans used to transfer dollars overseas. Today, a dollar goes for 84.2 bolivares in the black market – 13 times more than the official rate. Toyota is halting production, while Ford is significantly reducing its production in Venezuela. Venezuela’s economy is in shambles.

And its government is worse. Without getting into too much detail, Venezuela’s government is best described as a raging civil war where the Chavistas in power have bought the support of enough people to think they can deceive the country into thinking that they are representing them. In the last elections, the result was announced before all the votes were counted. People took to social media to report the fraud. Pictures and videos of military men burning boxes of ballots quickly spread over Facebook and Twitter. But the government had enough power over the military to stay “enchufados” (plugged in), as the opposition says. However, beginning February 12th, Venezuelans have taken to the streets by the millions. They are peacefully protesting against the government that is driving their country into ruins. Sadly, many people have been killed as they continue to take to the streets in protest, and the government persistently uses military force to subdue them. Now, they are outraged that the government is so blunt in oppressing them – not even trying to hide it anymore.

It is tragic to see a country so rich in natural resources, with so much talent and potential, deprived of its capability to provide its people with a decent life-style. Corrupt governments have a far-reaching effect on the economic well-being of a country. Most people in the US, and many other democratic countries, don’t realize the deep extent of corruption that exists in places like Venezuela. My intent is to raise awareness about this. The Venezuelan government is not the only corrupt, undemocratic government in the world, but at the moment, it stands out as one that is close to being brought down in favor of a more open, honest government. More pressure from foreign governments is essential–along with the noble efforts of the Venezuelan people–to put Venezuela back on the path of freedom and democracy.

Will Econ Blogging Hurt Your Career?

I ran across this very interesting youtube video by Noah Smith on “Will Econ Blogging Hurt Your Career?” I wanted to address that question as well. On balance, going forward, I think blogging is likely to be more of a help to your career than a hindrance–at least if you enjoy blogging.

One way in which my experience has been different from Noah’s is that I spend much more than an hour and a half per week blogging, if I include writing for Quartz. I have undertaken blogging as a serious career move, and so don’t mind spending some serious time at it. But that is something more appropriate for my career stage than it would be for a graduate student or untenured professor. And having grown children who are already off making their way in the world makes it easier.

As far as my own career goes, I feel the blogging has only been a plus. My colleagues in the Economics Department at the University of Michigan have been very supportive. Part of the reason is that I am not the only blogger here at Michigan. Noah has a list of other bloggers connected with the University of Michigan here. (Folks at the University of Michigan are blog readers, too. Interesing statistic: Ann Arbor edges out New York City as the city generating the most visits to my blog.)

As always, there are tradeoffs. Blogging might take time away from writing economics journal articles. But in my case I have found that blogging is fun enough and rewarding enough that I willingly do it at the expense of many leisure activities. And blogging builds human capital–contacts, writing skill and ideas (generated in important measure at the expense of non-blogging leisure)–that are valuable for research activities. So even the sign of the effect on traditional research productivity is, at this point, unclear. (Also, blogging should have some positive effect on citation accounts just by the inevitable publicizing of one’s own research, and is very helpful for one’s teaching.) Blogging creates additional temptations when one is avoiding hard but necessary tasks. But most of us face plenty of temptations in that regard anyway, and have had to develop techniques of self-discipline sufficient to get our work done.

I have a story to tell. Chris House’s office is right next to mine, with our doors one foot apart from each other. A couple of months ago, I walked into his office to talk as I often do, and he asked me how much time blogging took. I said “It depends on why you are asking; if you are asking so you can scold me for all the time I spend blogging …” Then it turned out he wanted to ask me if I thought it would be worth his while to start blogging. (I should say here that Chris is not the sort of person who would scold in any case; he would tease.)

Along the lines of what I said in my talk “On the Future of the Economics Blogosphere,” I said that I thought blogging was bound to grow in importance within economics–and that there is a first-mover advantage: for any given quality, those who start blogging earlier will gain more prominence and reap more rewards, as long as they remain continuously active.

Chris was persuaded; here is a link to Chris’s excellent blog. Among many other things he has accomplished with his blog, Chris caused Paul Krugman to write the sentences I think are most worthy of anything Paul Krugman has ever said of being included in a collection of famous quotations.

Mary O'Keeffe on Slow-Cooked Math

Mary O'Keeffe was my Ec 10 teacher back in 1977-1978. She has appeared previously on supplysideliberal.com in “My Ec 10 Teacher Mary O’Keeffe Reviews My Blog” and “Another Reminiscence from My Ec 10 Teacher, Mary O’Keeffe.” She gave me permission to share this Facebook post she made in response to the post “Cathy O'Neill on Slow-Cooked Math”:

I am also a slow-cook mathematician, for the most part. I find I have to get into a state of flow in order to really think math through. Often I find it takes me a while to really understand exactly what the problem is getting at—but after a while, it just sinks in and becomes blindingly crystal clear and beautiful. I am rather glad that I didn’t experience buzzer-style or any kind of timed math contests as a kid—they might have permanently discouraged me and induced me into giving up on doing anything mathematically related. I think one of the reasons my husband and I were such a good partnership (professionally) was that he was good at blazing fast insights and I was good at thinking things through more rigorously and deeply. (This is somewhat of a stereotype. We didn’t always fit neatly into these separate boxes, but it is a pretty good first approximation description.)

Jonathan Haidt—What the Tea Partiers Really Want: Karma

I am a fan of Jonathan Haidt’s work. I learned a lot from his book The Righteous Mind: Why Good People Are Divided by Politics and Religion, and used those ideas in my column “Judging the Nations: Wealth and Happiness Are Not Enough.” I also quoted one of my favorite passages from The Righteous Mind in "God and Devil in the Marketplace.“

Jonathan wrote a very interesting piece in the Wall Street, October 16, 2010: ”What the Tea Partiers Really Want.“ Here is a key passage:

But the passion of the tea-party movement is, in fact, a moral passion. It can be summarized in one word: not liberty, but karma.

The notion of karma comes with lots of new-age baggage, but it is an old and very conservative idea. It is the Sanskrit word for "deed” or “action,” and the law of karma says that for every action, there is an equal and morally commensurate reaction. Kindness, honesty and hard work will (eventually) bring good fortune; cruelty, deceit and laziness will (eventually) bring suffering. No divine intervention is required; it’s just a law of the universe, like gravity.

Karma is not an exclusively Hindu idea. It combines the universal human desire that moral accounts should be balanced with a belief that, somehow or other, they will be balanced. In 1932, the great developmental psychologist Jean Piaget found that by the age of 6, children begin to believe that bad things that happen to them are punishments for bad things they have done.

To understand the anger of the tea-party movement, just imagine how you would feel if you learned that government physicists were building a particle accelerator that might, as a side effect of its experiments, nullify the law of gravity. Everything around us would float away, and the Earth itself would break apart. Now, instead of that scenario, suppose you learned that politicians were devising policies that might, as a side effect of their enactment, nullify the law of karma. Bad deeds would no longer lead to bad outcomes, and the fragile moral order of our nation would break apart. For tea partiers, this scenario is not science fiction. It is the last 80 years of American history.

Zane Salem: How to Boost US Exports

I like my student Zane Salem’s post because it applies the principles I talk about in my post “International Finance: A Primer” and the related tools I talk about in my “Monetary and Financial Theory” class, particularly this “International Finance” Powerpoint file. The policy perspective is distinctively his. I am not signing on to all of it, but starting with sound theory makes what he says coherent in a way in a way most commentators who talk about trade are not.

Note that a Twitter thread disputes Zane’s claim of a positive correlation between net exports and GDP. I think when Zane said “GDP is directly correlated with the country’s net exports" he simply meant that net exports is a component of aggregate demand. But "directly correlated” has a different technical meaning. The overall correlation between net exports and GDP depends on many other causal forces in addition to the effect of net exports on GDP as a component of aggregate demand.

Here is what Zane has to say:

Last December’s export data revealed the United State’s trade deficit sunk deeper than expected. This was caused by both an increase in its imports and decrease in its exports. Since GDP is directly correlated with the country’s net exports, the recovering US economy will keep taking dents if this is not turned around.

Background for Improving Exports

The current administration has worked at improving exports numbers since the recession. This was done by attempting to remove trade barriers with other countries and by offering financial assistance with ease of information. While the data suggests there have been some successes, numbers are not where they could be. A subsidy or tax break in any way, shape, or form doesn’t provide a suitable solution for this problem the short run.

That being said, I see two possible ways to improve a country’s exports:

- Invest in assets abroad

- Protect intellectual property abroad

A most effective way to increase exports is by having a relatively weak currency. This makes a country’s goods/services look relatively cheaper and thus a worthwhile purchase to others. By applying the basic principles of international finance we covered in lecture, I’ve devised an algorithm to create a relatively weaker currency and thus more attractive prices for being imported. This could be applied to the United States or any other country.

Investment in Foreign Assets

- Invest in foreign funds – (ideally assets with HIGH rates of return)

- In exchange for their intentional IOUs, they receive unintentional IOUs (US dollars)

- The bouncing around unintentional IOUS (US dollars) overseas leads to an increase in the purchasing of our exports (from their perspective our goods look cheaper and they have dollars to exchange)

- In addition to the return on the investment, NX increases for the US

The reason this works is because of the currency exchange that takes place after the initial investment. The unintentional US dollars that foreign countries incur will be used to purchase goods and services from the US, effectively making the investment an exchange of assets for goods and services. The shortcoming here is that this algorithm requires a simplified model. And, in addition to large number of unconsidered factors, this method is susceptible to high taxes/fees that foreign funds could charge foreign investors. Its implementation could potentially be a controversial political gesture as well.

But we have seen small examples of this. For instance, the Czech republic, staying clear of the Euro-zone, can be seen as doing something similar to this strategy to boost its exports. By investing abroad, they have been able to increase their exports. We have also seen examples with larger impacts, specially from China. China invests huge sums in US and Japanese funds, and in return the US and Japan imports a large number of Chinese goods.

In fact, Japan has recently really been on the suffering end of this strategy, with their net exports have seeing a downturn due to this paradigm. China (along with the US), seeking higher returns on investments, invest in Japan. Logically, Japan increases its imports of Chinese goods and services. In fact, foreign direct investment (FDI) skyrocketed last month from China to Japan:

“The rise in outbound FDI in January was led by a 500 percent jump in investment in Japan, the ministry said without elaborating.”

Trading Economics (and Fed) shows data on Japan’s balance of trade over the past year (see below). Notice how after China’s 500% investment jump in January, leads to a heavy drop in Japan’s balance of trade that same month:

So things do look troubling in Japan. A good question you might be asking yourself: is the US being affected by this too? The short answer is yes. Even as the world’s richest country, we rank 2nd to China in exports as of 2012 (latest data). In fact, it makes plenty of sense that China is ranked 1st in exports.

Intellectual Property Protection

So this strategy seems like a trouble inducing arms race for lower interest rates across many countries. Is there anything else the US or other countries could do to improve its exports? Yes, especially for the US! The United States could protect its IP abroad. It certainly does have a lot of unique valuable exports that other countries demand. Some high demand products come from the entertainment (movies, music, etc) and technology industry (machinery, electronics, etc). But both of these products don’t get their fair share of purchases because of heavy media pirating and patented designs being exploited or stolen (ex: iPhone). Enforcing piracy and protection at home and especially abroad has been a difficult challenge that the country is still trying to resolve. This is an area that I think deserves more attention.

While all of this would help us recover from the economic downturn and have a healthy GDP, we would be doing a disservice to the “victim” countries by competing with their local businesses (shifting the supply curve upward) and enforcing protection of IP. If performing such actions cripples another nation’s economy, this has negative moral and political repercussions that shouldn’t be taken lightly. I think its important to realize what could be done to provide solutions, not necessarily to impulsively act upon them.

Quartz #46—>One of the Biggest Threats to America's Future Has the Easiest Fix

Here is the full text of my 46th Quartz column, coauthored with Noah Smith, “One of the biggest threats to America’s future has the easiest fix,” now brought home to supplysideliberal.com. (I expect Noah will post it on his blog Noahpinionas well.) It was first published on February 4, 2014. Links to all my other columns can be found here.

Writing this column inspired a presentation on capital budgeting I gave at the Congressional Budget Office. See my post “Capital Budgeting: The Powerpoint File.”

If you want to mirror the content of this post on another site, that is possible for a limited time if you read the legal notice at this link and include both a link to the original Quartz column and the following copyright notice:

© February 4, 2014: Miles Kimball, as first published on Quartz. Used by permission according to a temporary nonexclusive license expiring June 30, 2015. All rights reserved.

Noah has agreed to allow mirroring of our joint columns on the same terms as I do, after they are posted here.

I talked about some of the issues of capital budgeting addressed in this column a while back in my post “What to Do When the World Desperately Wants to Lend Us Money” and Noah has talked about the importance of infrastructure investment a great deal on his blog .

Other Threats to America’s Future: Our editor wanted to title the column “The biggest threat to America’s future has the easiest fix.” I objected that I didn’t think it was the very biggest threat to America’s future. I worry about nuclear proliferation. Short of that, I believe the biggest threat to America’s future is letting China surpass America in total GDP and ultimately military might by not opening our doors wider to immigration—a threat I discuss in my column “Benjamin Franklin’s Strategy to Make the US a Superpower Worked Once, Why Not Try It Again?”

In the 1990s, with its economy stagnating after a financial crisis, Japan lavished billions on infrastructure investment. The Japanese government lined rivers and beaches with concrete, turned parks into parking lots, and built bridges to nowhere. The splurge of spending may have allowed Japan to limp along without a full-blown depression, but added to the mountain of government debt that remains to this day.

Given Japan’s experience, it may seem odd for us to call for an increase in America’s infrastructure investment. In terms of infrastructure, the US now is not Japan in the 1990s. They didn’t need to build … but we do.

First, the United States is a lot larger than Japan, and larger than the densely populated countries of Europe. We have a lot more ground to cover with highways, bridges, power lines, and broadband infrastructure. We need to be spending a higher fraction of our GDP on these transportation and communication links—but instead, we spend about the same or less.

Second, where Japan’s infrastructure was in good condition when the spending binge started, America’s infrastructure is in hideous disrepair. The American Society of Civil Engineers gives America’s infrastructure a “D+”. Although infrastructure opponents typically dismiss the opinions of civil engineers (who, after all, stand to personally gain from increased infrastructure spending), McKinsey released a recent report saying much the same thing. McKinsey notes that Japan is spending about twice as much as it needs to on infrastructure. But the US is spending only about three-fourths of what we should be spending. The Associated Press piles on, saying that 65,000 American bridges are “structurally deficient.” A former secretary of energy says our power grid is at “Third World” levels. The list of infrastructure woes goes on, and on, and on.

This is not the picture of a country with a healthy infrastructure.

We need to rebuild our infrastructure, and now is the perfect time to do it. Interest rates are at historic lows, but they are unlikely to stay there forever. Our government has a unique opportunity to borrow cheaply to fund infrastructure projects that will generate a positive return for the country. (If the increased spending acts as a Keynesian “stimulus,” so much the better.)

But infrastructure budgets have been cut, not expanded. Why? One reason is that in the race to cut the deficit, infrastructure spending has been lumped in with other types of spending. That is a tragic mistake. Unlike government “transfers,” which simply take money from person A and give it to person B, infrastructure leaves us with something that helps the private sector do business, and thus boosts our GDP growth. Infrastructure is a small percentage of overall federal spending, but tends to be a politically easy target.

One idea to boost infrastructure spending, therefore, is to treat government investments differently from other kinds of government spending by having a separate capital budget. A separate capital budget has been suggested, but so far, the effort has foundered. There is a lot of confusion over which types of spending represent an “investment in the future.” Some politicians tend to argue that almost anything that helps people is an investment in the future, and so is a legitimate part of a capital budget. But of course everything in the government’s budget is something that someone thinks will help people! So what is needed is a clear criterion to determine what should be in the capital budget and what should be in the regular budget.

There should be a fairly stringent set of criteria for what belongs in a capital budget. Furthermore, these criteria should appeal to both parties. Here is what we suggest as criteria to keep the capital budget “pure”:

1. If experts agree that an expenditure will raise future tax revenue by increasing GDP, then it belongs in the capital budget. If it can pay for itself entirely out of extra tax revenue in the future then it should be 100% on the capital budget. If it can pay for half of its cost out of extra tax revenue in the future, than it should be 50% on the capital budget. The provision “experts agree” requires some sort of independent commission doing an economic analysis with appointees from both parties, and with, say, two-thirds of the commissioners needing to agree that the value of future tax revenue is likely to be above a given level.

2. Even if an expenditure will not raise future tax revenue, it can count as a capital expenditure if it is a one-time expenditure—that is, if it makes sense to have a surge in spending followed by a much lower maintenance level of spending in that area. This will only be true if it pushes the existing stock of infrastructure, other government capital, or knowledge to a higher level than before, not if it just keeps things even. Crucially, by this logic, anything that lets the stock of infrastructure or other government capital decline would count as anegative capital expenditure. This principle enables the capital budget accounting to sound a warning when the nation is letting its infrastructure crumble away, and also allows sensible decisions about shifting funds from older forms of infrastructure toward modern forms of infrastructure needed by a fast-moving economy.

As our mention of the stock of knowledge suggests, a capital budget can also be a good way to make sure that America doesn’t underinvest in basic scientific research. However great the importance of better roads and bridges, it makes sense to weigh the benefits of those roads and bridges against the benefits of research that might someday conquer Alzheimer’s disease, or research on how to make the way math is taught in our public schools so exciting that every high school graduate in America is able to do the math needed to, say, operate computerized machine tools.

With proposals like these on the table, we believe there is a chance that Republicans and Democrats could agree to set infrastructure and other legitimate capital spending aside as an issue that should not be a victim of titanic political battles over the deficit. Of course, someday, if we find ourselves in Japan’s position of spending so much on infrastructure that it starts adding significant amounts to the debt, then the capital budget should become an issue in deficit fights as well. But we are far from that point.

Both Republicans and Democrats want to govern a country that is as rich and prosperous as possible. America’s businesses need good infrastructure to move their goods from place to place—and there is no question that we need the solid new ideas that research can provide. Economists of all stripes will agree that if a nation is under-spending on infrastructure and other legitimate capital spending—as America is right now —then boosting that spending is a win-win. It’s time to look beyond our fights over how to divide America’s pie, and focus on making the pie bigger.

Technical Afterword

There is a very interesting feature to our proposed capital budgeting system that we should highlight. How can the capital budget ever be negative? The capital budget plus the non-capital budget must add up to the total budget. So for a given total budget, a negative capital budget makes the non-capital budget bigger. What is going on is this: regular maintenance is like a quasi-entitlement within the non-capital budget. In any given year, regular maintenance as a component of the non-capital budget is fixed in advance and can’t be altered by the legislature. The only way it changes is that it is gradually reduced if the quantity of capital to be maintained gets lower, or gradually increased if the amount of capital to be maintained gets bigger.

In this lack of discretion about regular maintenance as a component of the non-capital budget, there is no real tying of the hands of the legislature: they could always choose to have a very negative capital budget, which would increase the non-capital budget enough to cover that maintenance. So if the legislature as a whole acted like a fully rational actor, this principle is not a constraint at all. But as political economy, it makes a difference, and a good one. The legislature can increase the non-capital budget and reduce the capital budget. But what the legislature can’t do is get more funds for other things by letting capital decay without it showing up in the accounting as an increase in the regular budget and reduction in the capital budget.

On these technical issues, see also