Creative AIs—Derek Thompson →

As a tenured professor only 10 years away from retirement, I am not worried about my own job. What I liked about this article was being pointed to DALL-E-2 and Consensus. I tried them out. They seem useful.

Miles's Tweetstorm on Interpersonal Comparison of Utility

https://twitter.com/mileskimball/status/1597969384982515712

Building an Affordable House

In “Why Housing is So Expensive” I write:

There are two big reasons why housing is so expensive. The first is the obstacles put in the way of building new housing in many of the most desirable cities to live in. …

… [second] there has been no real improvement in productivity in construction in the last 50 years.

The book Building an Affordable House, by Fernando Pages Ruiz, and its review by Brian Potter in his blog Construction Physics, gives a sense of what the possibility frontier is for low construction and how far typical construction is from that possibility frontier.

A Rundown of the New Weight-Loss Drugs →

Note: semaglutide will go off-patent in 2032, so these drugs won’t always be super-expensive.

Nominal Illusion: Are People Understanding Real Versus Nominal Interest Rates?

Before the last couple of years, inflation had been low (and reasonably steady) for long enough, it wouldn’t be surprising if even important economic actors now didn’t fully understand that for economic decisions, they should be paying attention to real interest rates, rather than nominal interest rates.

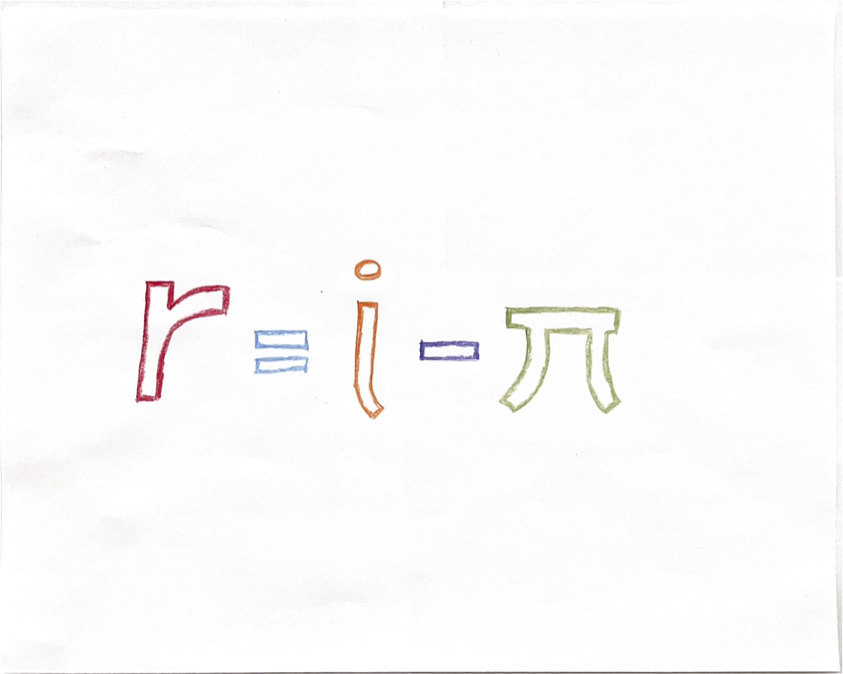

Take the tech sector, for example. There are many possible reasons for the end of the Second Tech Boom that Noah Smith talks about here. But higher interest rates are not a good reason, unless someone, somewhere, despite having a high IQ, fails to understand real versus nominal interest rates. Whatever the business model for monetization that a tech company pursues, the revenues—and ultimately profits—from that monetization should go up an extra amount from any general rise in prices. So for a venture capitalist, what should matter is what the interest is compared to inflation. The interest rate compared to inflation can be calculated as the usual concept of the interest rate—what economists call the “nominal” interest rate—minus the inflation rate. The usual nominal interest rate minus inflation is called the real interest rate. You can see the equation above. “r” stands for the real interest rate, “i” stands for the nominal interest rate and the symbol for pi stands for the inflation rate. (In economics, the symbol pi doesn’t always stand for 3.14159… It is more often the traditional symbol for the inflation rate, and only occasionally stands for 3.14159.)

There is no indication that the real interest rate is going to be all that high in the future. I have been tweeting that the Fed might well have to raise rates to 7% by sometime in 2023, which would be a considerably higher rate than the market seems to expect. But with core inflation running at 6.3%, that would be a real interest rate of only 0.7%. (“Core inflation” is the rate of changes in prices other than food and energy prices. The reason to take out food and energy prices is that they bounce around so much that what they do in any given month can mislead you about what it means for prices in the next few months.) I wouldn’t be surprised if a higher level of national debt (as measured in years’ worth of Gross Domestic Product) raised the long-run real interest rate somewhat compared to its very low rate so far in the 21st century, but that increase should be less than 1%. A long-run real interest rate of, say, 2% is a real possibility, but I’d be surprised to see any higher than that in the US during the next two decades.

The logic above applies to other real assets as well. For example, machine tools are used to produce goods whose price should go up along with other prices. So it is the interest rate compared to inflation—the real interest rate that should matter. That real interest is low, so it is a good time to buy a machine tool unless the price of machine tools is temporarily elevated compared to other prices.

Except for one wrinkle, it is even a good time to buy a house, as long as the house’s price isn’t so high that its price is likely to fall compared to other prices. If a house’s price will go up along with prices in general, the the inflation part of the interest rate you are paying will get recouped as nominal capital gains when you sell.

The wrinkle is an institutional one: the speed at which you are expected to pay back a fixed-rate mortgage is faster when the nominal interest is higher, even if the nominal interest rate is higher only to make up for inflation. “Fixed-rate” could have been—and should have been—defined in terms of real rates, but it isn’t. Traditional adjustable-rate mortgages also ask people to pay back the loan faster if the nominal interest is higher because of inflation. In either case, the same real rate with higher inflation means that someone with a mortgage has higher mortgage payments and builds up home equity faster (as long as the house price goes up along with other prices in the economy). In a high-inflation environment, the typical fixed-rate mortgage has a large component of forced saving to it. Not everyone can swing that high a level of forced saving, so housing demand gets crushed in times of high nominal interest rates, even if the real rate is low. Economists call the cash crunch when a high level of forced saving causes real hard ship a “liquidity constraint.” Liquidity constraints interact with the traditional form of mortgages to make it hard for many people to buy a house. This is unlikely to change any time soon because it scares people to see the nominal value of their mortgage go up, which is typically needed to keep mortgage payments low when inflation is high.

Let me challenge you to notice when you read the news or listen to what people are saying to look for places where people are forgetting the value of looking at real rather than nominal interest rates—or equivalently, where they are forgetting the ways in which a general rise in prices might make an investment in something real more attractive.

Brad DeLong Confirms that Not Having Negative Interest Rate Policy in the Monetary Policy Toolkit Makes People Afraid of Vigorous Rate Hikes to Control Inflation

In my September 5, 2022 post, “How a Toolkit Lacking a Full Strength Negative Interest Rate Option Led to the Current Inflationary Surge,” I write:

Thinking falsely that it couldn't fall back on negative rates, the Fed was too slow and timid in raising rates for fear that it didn't have the firepower to quickly reverse a recession if it went too far in raising rates.

In his Project Syndicate op-ed “When the Fed Stops Trying,” Brad DeLong confirms that this concern is on his mind, and indicates he thinks it has been on the mind of policy-makers in the Fed. Here are some key quotations from that piece, separated by added bullets:

Biden’s team knew that if the reopening inflation shock was too large, it could easily trigger an overreaction from the US Federal Reserve. That, eventually, would put America back in a semi-depressed or depressed state of secular stagnation, with little policy traction to respond to the next crisis or to promote a recovery.

The situation was thus analogous to Odysseus sailing between Scylla (a multi-headed monster) and Charybdis (a massive whirlpool). The Biden administration could either not try to navigate the strait at all (the first mistake), or it could try its luck with Scylla (secular stagnation) and Charybdis (stagflation).

Not without reason, financial markets seem to be betting that the Fed is about to make mistake number two: pursuing policies that will likely drag the US back toward secular stagnation. If past is prologue, we eventually will return to a scenario in which monetary policy is stuck at the zero lower bound. The economy may suffer another lost half-decade of growth, and socially and politically destabilizing inequalities will become even more pronounced.

In the last passage, Brad makes it clear the “secular stagnation” means being stuck at the zero lower bound. But of course, there is no zero lower bound. The idea that interest rates cannot be cut below zero, or cannot be cut very far below zero, is inside-the-box thinking—and the box is made of only flimsy material. The more I have worked on the details of how to best implement deep negative rates, the clearer it becomes that it is an available policy option. You can see the details in the resources laid out in my bibliographic post, “How and Why to Eliminate the Zero Lower Bound: A Reader’s Guide.” (You can always get there by clicking on the “NEG.RATES” button at the top of this blog.)

Also, despite West Virginia v. EPA, the authority of the Fed (a) to buy and sell Treasuries and (b) over its own reserve accounts needed to implement negative interest rate policy are so clearly authorized by statute, I believe the Fed, under current law, has the authority to implement deep negative rates along the lines of “How the Fed Could Use Capped Reserves and a Negative Reverse Repo Rate Instead of Negative Interest on Reserves.” (I am currently writing an article with a law professor, intended for a law review, making this case.)

Note that, as things stand, the likely timeline for needing negative rates allows plenty of time to lay out a monetary policy strategy including negative interest rates as part of the toolkit before we will need to actually implement negative rates.

Right now, one of the main objections people might make to negative interest rate policy is “You have to be kidding! How could you be talking about negative interest rates when inflation is so high. We need big interest rate hikes, not negative rates.” That is true as far as it goes, but I am arguing that the Fed’s slowness to raise rates is partly due to its fear that it doesn’t have the tools to deal with a serious recession. That raises the cost of raising rates too much—by a lot. The Fed will be scared to with inflation vigorously and promptly unless it also has the tools to deal with deflation. Imagine driving on a mountain road with a sheer drop to your right. Wouldn’t that increase the danger that you would hew to close to the middle of the road and collide with oncoming traffic? Or to take Brad’s analogy, if we know we can disarm and defang Scylla with negative interest rate policy, then we can steer far away from Charybdis.